By Ashay Abbhi

The growth of renewable energy in India has opened up a plethora of opportunities for all stakeholders. The dynamic policy environment aligned with the government’s ambitious targets has improved investor confidence. Meanwhile, competitive bidding and the resulting low tariffs have enhanced the offtake of renewables-based power. The overall risk profile of renewable energy projects has also improved. Interestingly, the recent developments in the segment have led to a spike in private equity (PE) investment. Strong rounds of funding are a testament to the increasing investor interest and the growing stability of renewable energy companies. Robust PE activity accompanied by a wave of mergers and acquisitions (M&As) points towards a sustainable future for the sector. According to Renewable Watch Research, PE activity in the renewables sector in 2018-19 has been the highest in the past five years. Across the 13 PE deals tracked by Renewable Watch Research for the year 2018-19, $2,273 million has been invested in the sector. The value of deals was nearly double that of the previous spike, experienced in 2015-16, when $1,206 million was invested through eight deals. In comparison, in 2014-15, although the number of deals was high (10 deals), their value was quite low, averaging at $56.6 million per deal. In 2016-17, when the renewable energy industry opened up significantly on the back of strong policy changes, only five PE deals with a cumulative value of $586 million were reported. The year 2017-18 saw the lowest deal value in the past five years, with seven deals amounting to only $270.5 million.

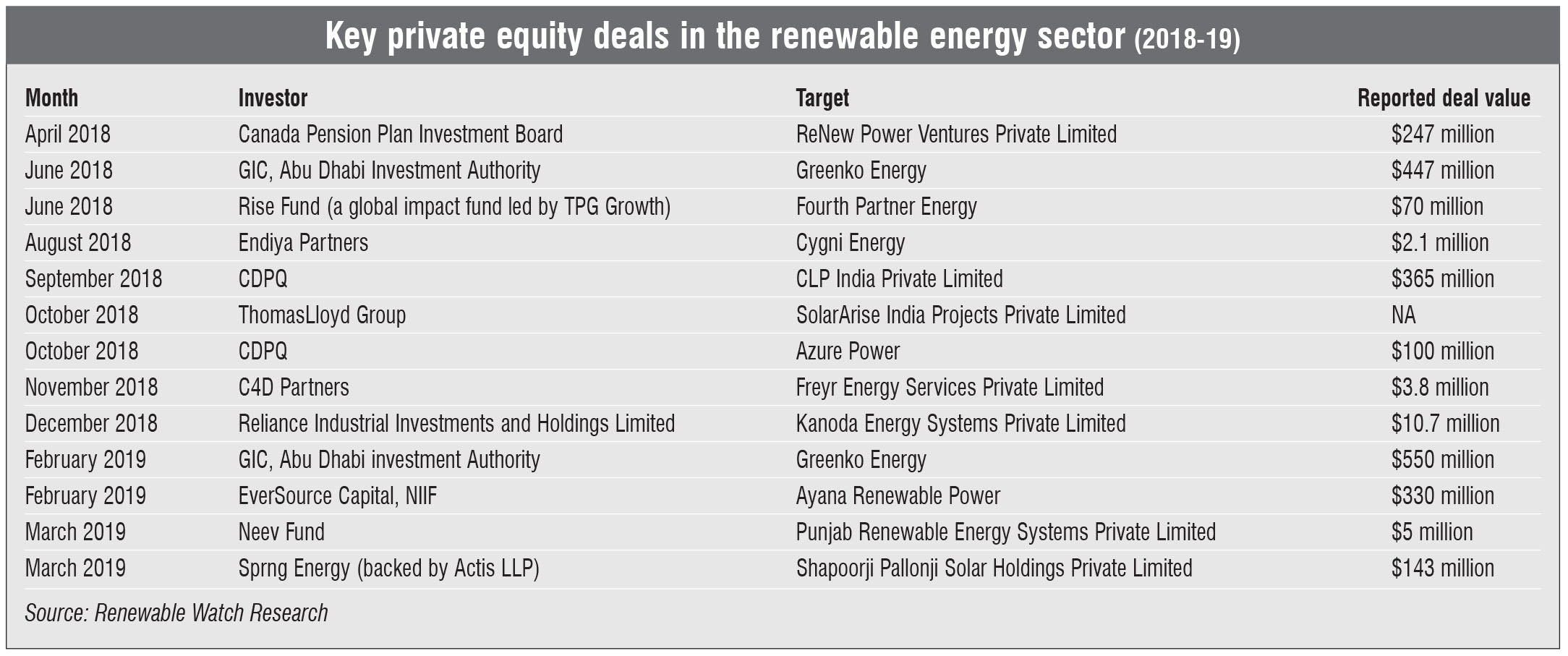

Key deals

Six of the 13 PE deals in 2018-19 were valued at over $100 million each, indicating the high valuation accorded to renewable energy companies in the market. The largest deal of the year was the $550 million investment in Greenko Energy by Singapore-based GIC Private Limited and the Abu Dhabi Investment Authority (ADIA) in a fresh round of funding in February 2019. With this, the enterprise value of Greenko Energy has reached around $5.2 billion. In June 2018, Greenko had raised $447 million from GIC and ADIA, bringing the total PE investment in the company in the year 2018-19 to $997 million, the largest for a single entity in a given year in the Indian renewable energy sector.

The second largest deal of the year was a Rs 26.4 billion (about $365 million) investment made by Quebec-based investor Caisse de Dépôtet Placement du Québec (CDPQ) in September 2018 to acquire a 40 per cent stake in CLP India Private Limited. CDPQ, the second largest pension fund of Canada, has made several investments in the Indian renewable energy sector. In October 2018, it invested $100 million in Azure Power, bringing its total investment in the sector in 2018-19 to $465 million. The pension fund is reportedly looking to acquire Morgan Stanley-backed Continuum Wind Energy’s assets. This includes 700 MW of operational wind assets and a pipeline of almost 1,700 MW. In February 2019, EverSource Capital, a joint venture between Everstone Capital and Lightsource BP, along with the National Investment and Infrastructure Fund (NIIF), invested $330 million in Ayana Renewable Power, a renewable energy platform floated by UK-based development finance institution CDC. EverSource Capital has plans to set up a Green Growth Equity Fund with a corpus of £500 million ($710 million).

The largest Canadian pension fund, the Canada Pension Plan Investment Board (CPPIB) invested $247 million in ReNew Power Ventures in April 2018. These funds were targeted at the acquisition of Ostro Energy, a rival power producer backed by Actis LLP. With this, CPPIB’s total investment in ReNew has increased to $391 million. In an earlier round of funding in January 2018, CPPIB had invested $144 million in ReNew. The most recent PE deal in the sector was the acquisition of a 49 per cent stake in Shapoorji Pallonji Solar Holdings Private Limited (SPSHPL) by Actis LLP-backed Sprng Energy for $143 million in March 2019. The acquisition is a part of Actis’s commitment to build renewable power projects with a cumulative capacity of 2,000 MW in India. With this deal, Sprng Energy’s operational and under-construction assets have grown to 1,650 MW. In an earlier round of funding, Sprng Energy had received $450 million from Actis. Other notable deals include a $70 million investment in Fourth Partner Energy by Rise Fund, a global impact fund led by TPG Growth. Fourth Partner Energy is focused on financing and building rooftop solar projects in India through the resco model. The company is targeting a cumulative asset portfolio of 1,000 MW by 2022. It also plans to expand its reach to other countries in Southeast Asia, West Asia and Africa. Besides this, Endiya Partners invested $2.1 million in Cygni Energy in August 2018. In October 2018, the ThomasLloyd Group invested an undisclosed amount in SolarArise India Projects. In November 2018, C4D Partners invested $3.8 million in Freyr Energy Services, and Reliance Industrial Investments and Holdings Limited infused $10.7 million in Kanoda Energy Systems. In March 2019, Neev Fund invested $5 million in Punjab Renewable Energy Systems Private Limited.

Attractive opportunity

Attractive opportunity

The renewable energy space presents an attractive opportunity for investors and PE players. There is considerable ease of project implementation as compared to some of the other infrastructure sectors due to short gestation period and fewer regulatory hurdles. The must-run status of renewable energy projects ensures power offtake, thereby guaranteeing a constant cash flow. Moreover, with only a handful of companies listed in this sector, viable exit options are available for PE investors through initial public offerings (IPOs). Within renewables, the solar segment has witnessed greater investor interest vis-a-vis wind energy. Project equity has also emerged as an investment option. This involves the investment of funds in specific projects in lieu of a share of equity. Usually, operational projects are more likely to get project equity, considering that power purchase agreements are in place. This significantly reduces the risks otherwise seen in under-construction projects.

Challenges and the way forward

Challenges and the way forward

The renewable energy sector has its own set of risks and challenges. Both solar and wind energy are dealing with land acquisition challenges – limited land availability for setting up projects and the high cost of land, which significantly adds to the total project cost. The must-run status of renewable energy projects has often been questioned, given the grid integration issues being faced in states such as Tamil Nadu and Karnataka. A recent order issued by Karnataka to stop procuring more solar power as its discoms had met their renewable purchase obligations has further diluted investor interest in the segment. Transmission constraints continue to impact project development while payment delays by cash-strapped discoms are adding to financiers’ woes by elevating the risk profile of projects. The recent fall in tariffs in the solar and wind power segments has left investors with single-digit returns from projects. Since the basic premise of a financier is to get returns on investments, the low-return situation adversely impacts investor confidence.

The issues notwithstanding, there has been a considerable growth in PE deals in the past five years. The sudden spike in deal value in 2018-19 indicates the growth opportunities that exist for developers and investors alike. With a number of players announcing their IPOs, the sector can expect an even higher level of PE participation in 2019-20 in the form of pre-placements. Finally, with a number of renewable energy players exploring synergies with and diversifying into new segments such as e-mobility and battery storage, investment opportunities in renewables are likely to open up further for PE investors.