For the past one year, the solar industry has been focusing more on rooftop solar development. An increasing number of states are reforming their net metering regulations. In Uttar Pradesh and Himachal Pradesh, new net metering regulations have been proposed. In April 2018, the Central Electricity Authority issued a draft amendment to technical standard regulations for generation resources like rooftop solar in an effort to maintain grid stability. On the industry front, a large number of players have entered the solar power space, with some of them looking to set up only rooftop plants.

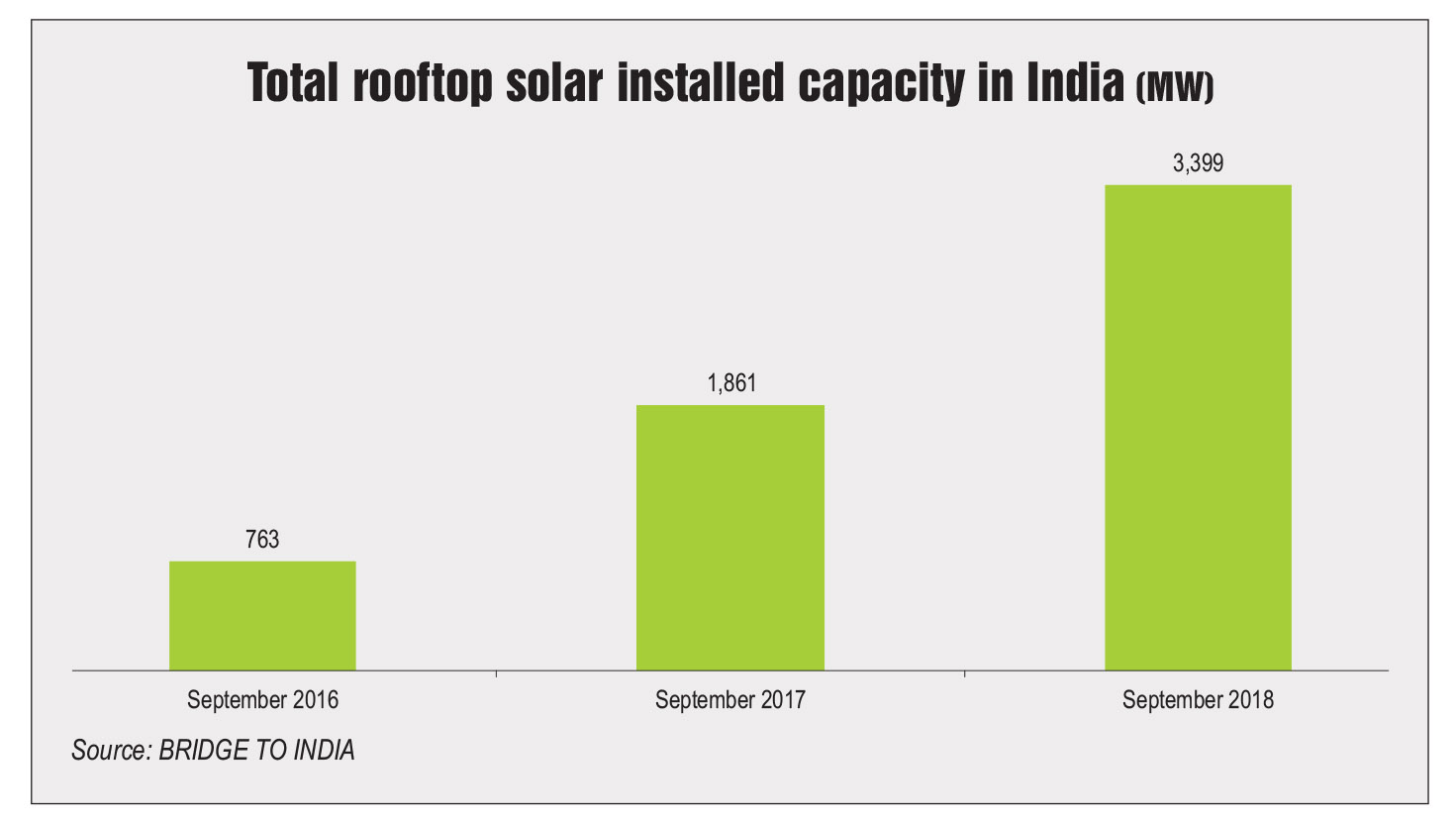

Despite these efforts, rooftop solar photovoltaic continues to be a minority segment in the country’s overall solar power ecosystem. So far, India has installed over 26 GW of solar capacity, of which rooftop solar installations make up only about 11 per cent. This is in stark contrast to some of the top solar countries in the world that have built a huge solar base on the back of rooftop solar installations. However, for countries like China and India, which were late entrants in the solar market, the primary aim was to reduce the cost of solar power procurement to expedite capacity building and inclusion into the mainstream power sector. Thus, the policy thrust has been on large ground-mounted solar capacity installations in order to achieve scale. This resulted in sluggish growth of the rooftop solar segment. However, the ecosystem seems to be changing now. Of the 100 GW by 2022 solar power target, 40 GW is envisaged to come from rooftop solar. This shows that the market is beginning to evolve. Rooftop capacity has grown at a compound annual growth rate of over 111 per cent between 2016-17 and 2018-19. The total rooftop solar capacity in India increased from 763 MW in September 2016 to 1,861 MW in September 2017, experiencing a year-on-year growth of 144 per cent. As of September 2018, the rooftop solar capacity in the country reached 3,399 MW, growing at 82.6 per cent over September 2017.

The high growth rates indicate a growing acceptance of the rooftop solar power model in the country. The growth continues to be led by the commercial and industrial consumer segments, followed by the government and institutional categories. The residential segment has seen minimal uptake, except in a few clusters where discoms are pushing for rooftop installations on residential buildings.

Growth drivers

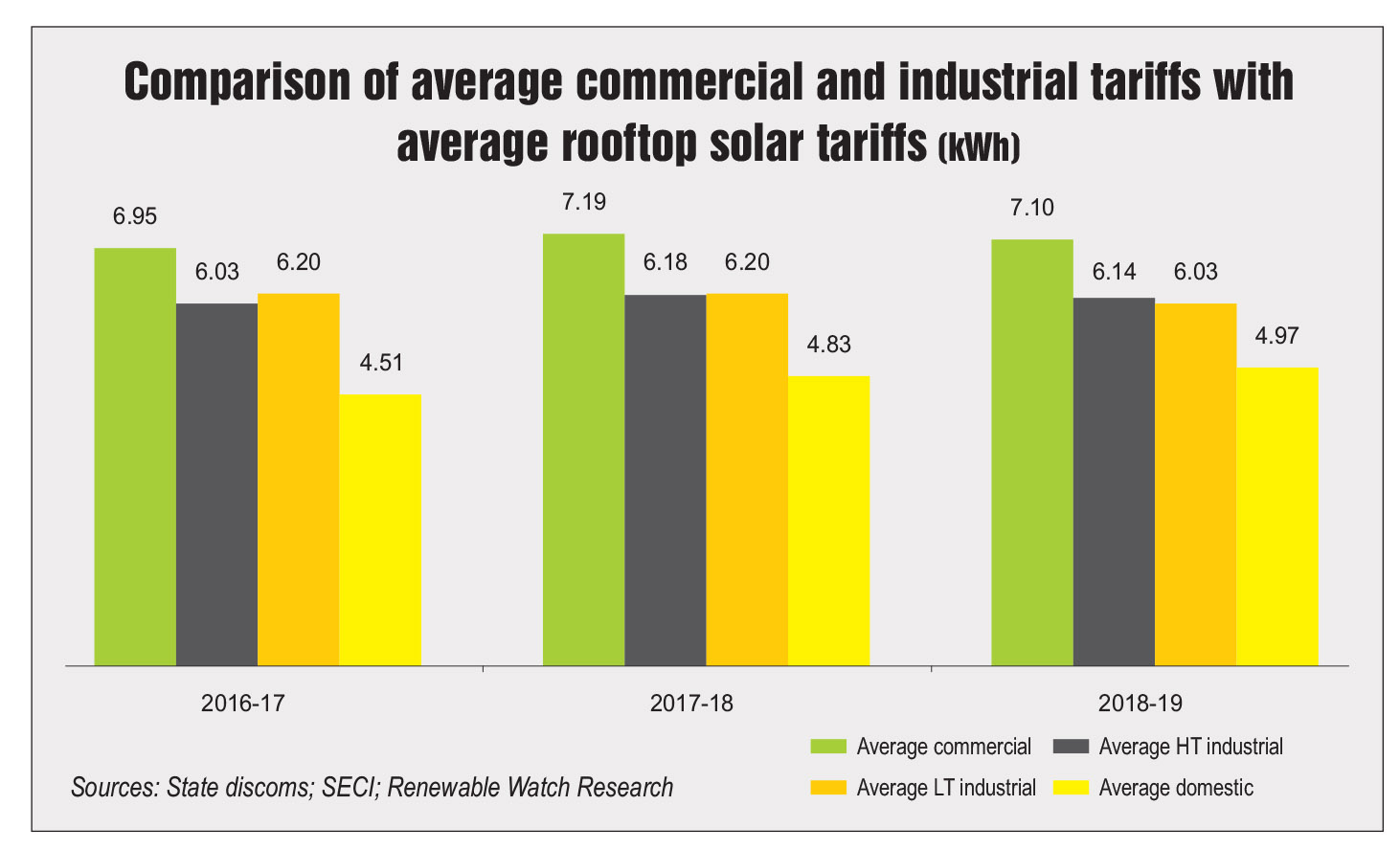

The financial benefits of rooftop solar for large power consumers are considerable. Although they vary across states, commercial and industrial tariffs are typically high in India. This is primarily on account of the cross-subsidisation of power to agricultural and low-income consumers. The average retail commercial tariff in the country stood at Rs 7.10 per kWh, HT industrial tariff at Rs 6.14 per kWh and LT industrial tariff at Rs 6.03 per kWh.

Meanwhile, in the recent 500 MW auction conducted by the Solar Energy Corporation of India under the opex model, the average rooftop solar tariff stood at Rs 3.32 per kWh. Thus, rooftop solar makes considerable economic sense for the commercial and industrial segments. However, the national average of retail tariff in the domestic segment stood at Rs 4.97 per kWh. The financial benefits for the domestic segment are not very high. This is the primary reason for the low uptake of rooftop solar power by residential consumers.

The commercial and industrial consumer segments, therefore, are the mainstay of the rooftop solar business in the country. The returns on investment for these consumers are high while the payback period is low. According to Anvesha Thakker, executive director, Energy & Utilities, Management Consulting, KPMG India, “The commercial and industrial segments have the largest market share in solar rooftop deployments. The primary driver is, of course, the attractive economics, which results in substantial savings in power cost per unit. Another major driver is the ‘green image’ of the firm and ‘carbon neutrality’, aside from renewable purchase obligations of companies procuring fossil fuel-based power.”

Comprehensive rooftop solar policies and net metering regulations along with utility interconnection processes have given confidence to the entire value chain. With greater uptake of rooftop solar systems, the business models for the segment have also evolved. Historically, the capex model has been the most prevalent for such projects. Of the 3,399 MW of rooftop solar capacity installed as of September 2018, about 2,496 MW (65 per cent) was set up under the capex model.

However, the adoption of the opex model is increasing due to high upfront capital costs of the solar system, and the lack of expertise among rooftop owners to undertake efficient operations and maintenance of these systems. The share of the opex model increased from merely 3 per cent in 2012 to 35 per cent in 2018. P. Vinay Kumar, founder, Varp Power, says, “The capex and opex models have been the mainstay of the onsite rooftop business for commercial and industrial customers. There is scope for much financial innovation in this space. Leasing models that allow customers to retain depreciation benefits are likely to find favour as we go forward.”

Key challenges

The rooftop solar regulations vary from state to state. This lack of standardisation creates a significant challenge for developers in terms of business models and policies. Further, the implementation of these regulations is sketchy at best. Net metering is a prime example of a favourable initiative that has suffered due to lack of execution. While on paper it has been adopted by every state, its usage on field remains ineffective, thereby restricting the growth of rooftop solar. Financing is a significant challenge for rooftop solar project developers and consumers. Financiers are not yet comfortable in lending to rooftop projects on account of the borrowers’ low credit profile, and quality concerns related to equipment and contractors. Another key reason for the low popularity of rooftop solar in contrast to the ground-mounted solar segment is the reluctance of many state discoms to let go of their high-paying customers. Other challenges include quality concerns that stem from lack of skilled professionals in the segment. Moreover, with no set standards, contractors offer products and services of various quality levels. With the rise in the opex business model, standardisation and legal enforcement of power purchase contracts become important.

Potential and outlook

The rooftop solar segment will have to add about 36.6 GW of capacity over the next four years, an average of 9 GW per annum, to achieve the set targets by 2022. However, given the current pace of growth in the segment, this seems highly unlikely. Inefficiencies in the approval process of net metering applications along with the delayed payment of subsidies continue to restrict the growth of the segment. Focused measures will need to be undertaken to tap the segment potential.

The biggest roadblock in the growth of the rooftop segment is discom reluctance, which will need to be effectively addressed. The Ministry of New and Renewable Energy (MNRE) is reportedly working to revamp the process with the help of various stakeholders. Kumar says, “There is an urgent need to make discoms a stakeholder in the roll-out of decentralised solar plants and not just victims of lost revenue and customers. Various ideas are being discussed in the industry and the MNRE seems to be on the right path here.”

While commercial and industrial consumers are currently the largest growth centres in the rooftop segment, residential consumers also present significant untapped potential. At present, solar awareness in the retail sector is still limited and people need convincing to choose this energy as a cheaper and cleaner alternative to grid power. The government and industry stakeholders need to develop consumer interest through collective marketing and affordable financing options. Group housing societies with large rooftop areas and small towns with low-income groups could be provided viability gap funding and subsidies to develop their rooftop solar plants.

In sum, the future for the rooftop solar segment remains optimistic with newer business models and policies expected over the next few years.

By Ashay Abbhi