By Ashay Abbhi

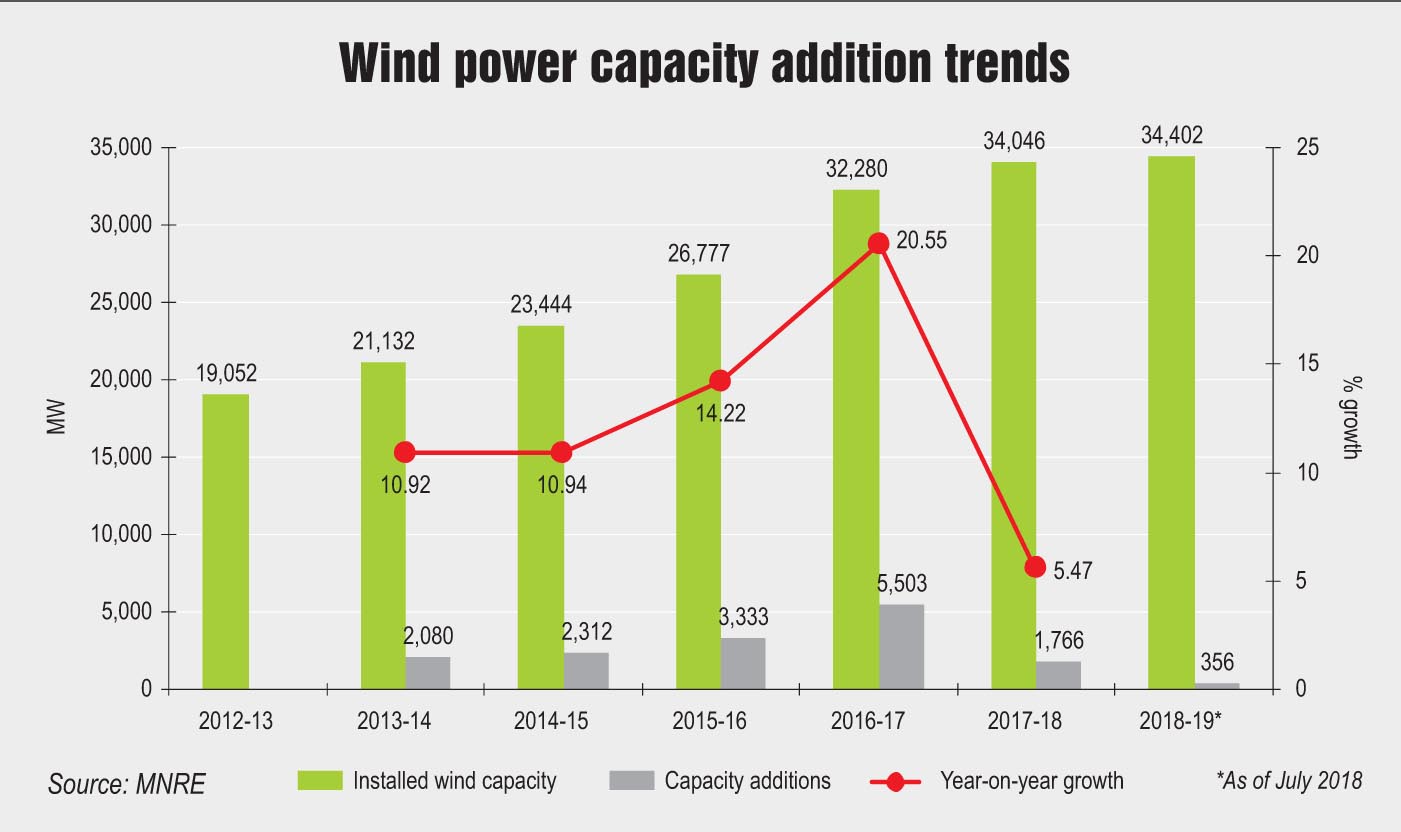

Policy changes during 2016 and 2017 created a temporary depression in the upward trajectory of wind power capacity addition, leading to mixed sentiments in the segment for over a year. Of all the changes, the introduction of the competitive bidding regime yielded several positives. With over 15 GW of capacity either tendered or in the process of being tendered, the segment seems to have regained momentum in 2018. The current installed wind capacity in the renewables sector stands at 34.4 GW, implying that an average of 6 GW of capacity needs to be added per annum to achieve the 60 GW target by 2022. In the long term, the government intends to have 140 GW of wind power capacity by 2030.

Competitive bidding for project allocation and tariff determination was introduced in November 2016, making the segment entirely market driven. Pegging it directly to market forces meant withdrawal of regulated tariffs and financial aid available to wind power generators in the form of accelerated depreciation (AD) and generation-based incentives (GBIs).

On the bright side, tariffs fell to an all time low, resulting in greater wind power offtake as discoms now prefer it to other sources. A transparent and streamlined project allocation mechanism has now been put in place with well-defined trajectories to achieve the desired targets. Greater consolidation is witnessed in the industry as competition evolves into the matured phase, weeding out the non-serious-non-core developers. Moreover, project sizes are becoming larger, bringing in advantages of scale.

Investor outlook for the segment has thus improved, making finance increasingly accessible to project developers as wind power becomes a safe bet for the industry. The availability of competitive capital has countered the ill-effects of falling tariffs for developers, thereby improving profit margins. Meanwhile, there is an increased focus on technological innovation by manufacturers as they work towards bringing down the levellised cost of energy and increasing the plant load factors (PLFs). Domestic and international manufacturers have envisaged next generation turbines that are likely to deliver around 35-40 per cent PLFs in high wind states, nearly twice that of solar.

New technologies and project designs have also received significant government impetus. While the solar-wind hybrids and offshore wind power policies have been finalised, initial projects have reached advanced stages to achieve the targets set for solar-wind hybrids at 10 GW by 2022, and that for offshore wind energy at 5 GW by 2022 and 30 GW by 2030. The Ministry of New and Renewable Energy (MNRE) is now working towards creating a policy-based market for energy storage by finalising the National Energy Storage Mission, which will have significant implications for the wind power segment.

These gains are, however, riddled with multiple challenges that can potentially derail the progress made by the segment so far. The biggest challenge pertains to grid connectivity allocation and access. It will lead to significant time and cost overruns during project development and possibly idle capacity post-erection for the lack of transmission capacity. This stems from the general progress of transmission and distribution infrastructure being sluggish. The challenges are further amplified by the short-term pressure point created by competitive bidding that questions the viability of wind power projects at such low tariffs.

The year 2018-19 marks the first year of operations after the shape of the three decade-old Indian wind power market was altered forever with the introduction of the competitive bidding regime. It is, therefore, the benchmark against which these policy developments will be judged as the fruits of the regime change have begun to show. In October 2018, the first competitive bidding-based capacity (auctioned in Solar Energy Corporation of India Limited [SECI] I) was commissioned. Located in Chandragiri, Tamil Nadu, it is a 250 MW wind power project owned by Sembcorp Energy and developed by Suzlon.

Renewable Watch analyses the key developments in 2018 so far, their effect on the wind power market, challenges faced and the future of the segment.

Current status

The capacity addition of wind power in India saw a steady increase until 2017-18. It was one of the worst years in the past half decade, with only 1.7 GW of capacity added in the aftermath of various policy decisions taken in the preceding year. Competitive bidding was introduced in November 2016 and the first bidding round took place in February 2017. The severity of the policy impact can be judged by the fact that against a potential to add around 8 GW-10 GW per year, less than 2 GW was added.

This had immediate fallouts for the wind power segment in the country. First, the major policy shift sent shockwaves through the market, throwing off the existing business models of developers and manufacturers alike. The first round of bidding discovered tariffs much lower than feed-in-tariffs (FiTs) prevalent at the time (Rs 3.46 per kWh discovered against a FiT of Rs 5 per kWh). This further aggravated the frenzy as the double digit internal rate of returns (IRR) now reduced to sub-10 per cent levels for developers. Second, the market anticipated states to follow the centre and implement competitive bidding. There was, as a result, a rush to get projects approved under the then existing FiT regime to make the most of the higher tariffs while they lasted.

The removal of GBI and slashing of AD by half did not help matters for project operators. These came into effect on April 1, 2017, and the quarter before that saw large capacity additions to avail of these benefits. Moreover, the decrease in capital costs was not proportional to the fall in tariffs, thereby further diminishing profit margins. The threat of potential reneging of power purchase agreements (PPAs), after Andhra Pradesh and Karnataka backtracked on their signed PPAs with the discovery of Rs 3.46 per kWh of tariff in the first tranche of wind power auctions, also loomed large over the market.

The impact of these developments created uncertainties that spilled over into 2017 and 2018. The growth rate of the segment fell drastically while the developers and manufacturers realigned themselves with the reality of competitive bidding. The wind power capacity has increased at a compound annual growth rate of 13 per cent from 2012 to 2017, with varied growth rates from one year to the next. There was an impressive 20.55 per cent growth from 2015-16 to 2016-17, while the growth in capacity additions dropped to a meagre 5.47 per cent after the introduction of competitive bidding.

Even in 2018-19, ripple effects of these decisions continue to hinder the market growth. During April-July 2018, only 356 MW of wind power capacity was added, according to the MNRE. The annual target remained stagnant at 4 GW. Industry estimates suggest that the capacity addition in 2018-19 will remain low, at around 2 GW-2.5 GW, seriously hampering the achievement of the annual as well as 2022 targets.

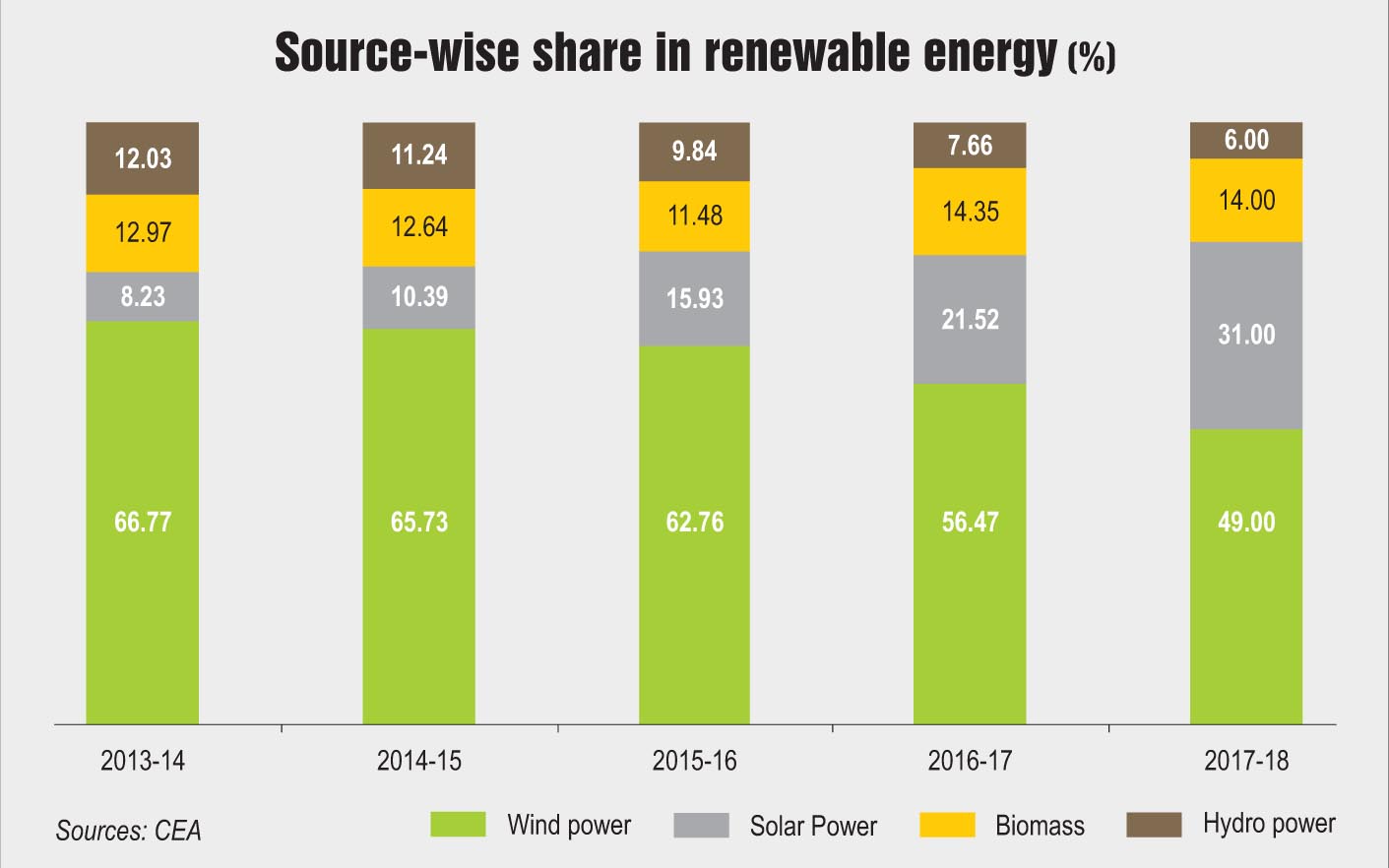

Wind power contributes 49 per cent to the renewable power mix and 9.8 per cent to the total power capacity mix of the country. However, this share is decreasing every year, owing to the rapid capacity additions in the solar segment, in contrast to the wind segment. Given the recent policy developments, the share of wind power is expected to fall even further in the coming years as the expected solar capacity additions are likely to surpass that of wind by a significant margin.

New normal

New normal

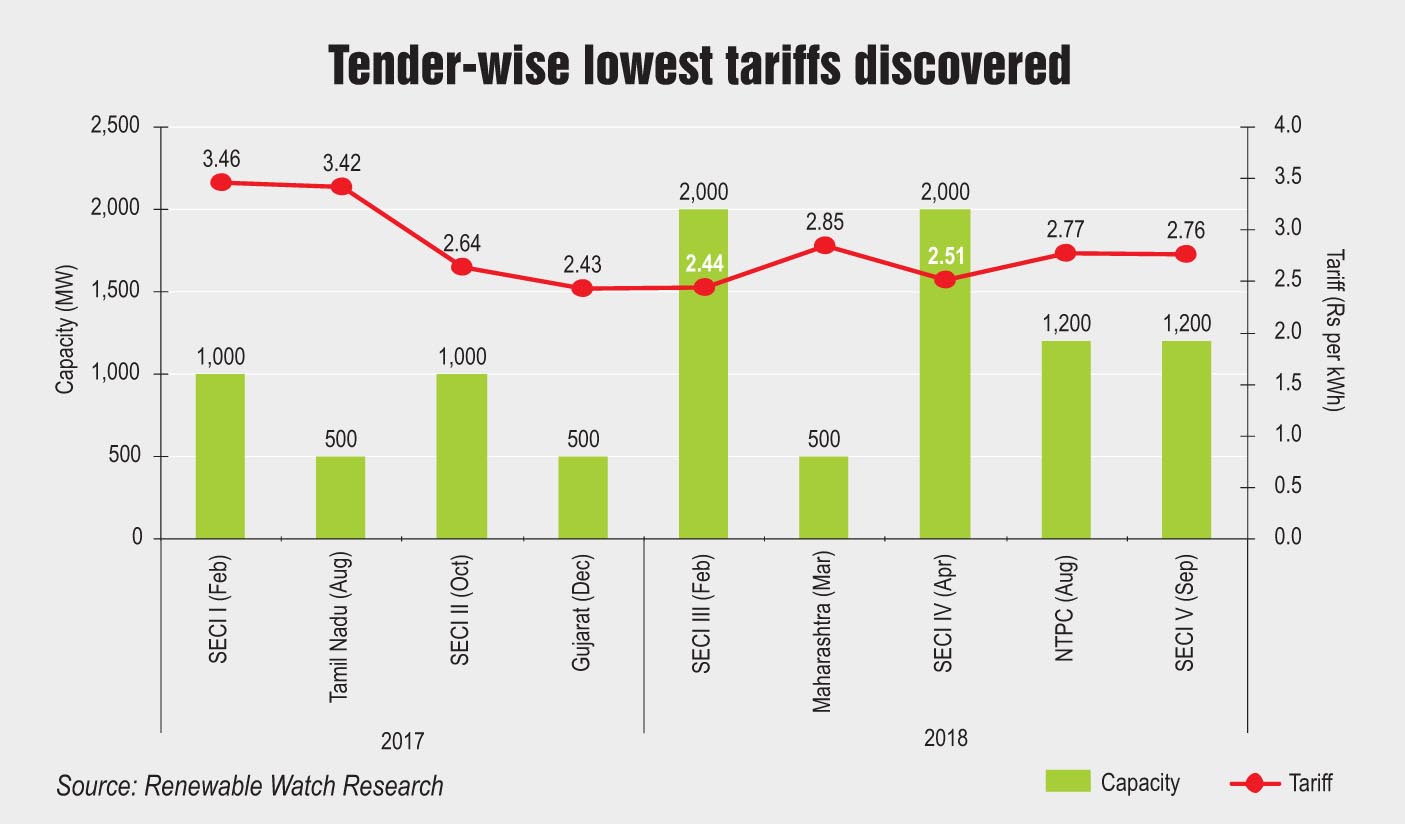

So far, tenders for about 9 GW have been released across four tranches by SECI and the states of Tamil Nadu, Gujarat and Maharashtra in 2017 and 2018. The low levels of tariffs set by the first wind power auction have continued through subsequent state and central tenders, setting a new normal for the segment. From February 2017 to December 2017, the lowest tariffs discovered fell from Rs 3.46 per kWh to Rs 2.43 per kWh across 3 GW of capacity in two tenders by SECI and one each by Tamil Nadu and Gujarat.

In February 2018, the southward tariff trend reversed slightly with the SECI Tranche III tender wherein 2 GW of capacity was auctioned. The lowest tariff discovered was at Rs 2.44 per kWh, followed by Rs 2.51 per kWh in the 2 GW SECI Tranche IV tender released in April 2018. Meanwhile, the lowest tariff discovered in the 500 MW Maharashtra tender rose to Rs 2.85 per kWh. In August 2018, NTPC released its first wind tender with 2,500 MW of capacity. However, it received bids only for 2,000 MW and was further reduced to 1,200 MW. The lowest bid discovered in this tender was at Rs 2.77 per kWh, indicating an upward trend in tariffs, though not too far from the normal.

Meanwhile, there has been a spate of tenders cancellations due to severe unavailability of transmission capacity. As a result, the interest in tenders has been falling and tariffs have been increasing marginally. Lack of interest in tenders eventually led to cancellations and retendering of capacity. In July 2018, SECI Tranche V tender with 2 GW of wind power capacity was cancelled as it failed to garner sufficient bids owing primarily to transmission issues. It was then retendered in August 2018 with a total capacity of 1,200 MW and was heavily oversubscribed. The lowest tariff discovered was at Rs 2.76 per kWh, won by Torrent Power (115 MW) and Adani Green Energy (300 MW). While the tariff discovered in this auction is Re 0.01 per kWh less than that of NTPC’s 1,200 MW tender, it is Rs 0.25 per kWh more than the lowest tariff discovered in SECI Tranche IV.

Gujarat Urja Vikas Nigam Limited (GUVNL) had annulled its 500 MW wind power tender in July 2018, for lack of adequate transmission infrastructure. The recent fall in wind power tariffs has tempted many states to auction wind capacity to fulfil their renewable purchase obligations (RPOs). However, tight transmission capacity and low land availability in high PLF areas can lead to higher tariffs or tenders being cancelled altogether.

Driving growth

Driving growth

Though there are several hurdles in the growth of the wind power market, they can safely be called transitional issues. There are various factors that are pushing the segment forward and ensuring a more transparent and efficient project development system.

With competitive bidding securely established as the primary route for project allocation and tariff determination, the multi-level auctions held by the centre and states help create a decentralised and transparent tendering process. Over 8 GW of capacity has been auctioned through central agencies (SECI and NTPC), wherein the projects can be set up in any of the wind-rich states and the power will be sold through inter-state transmission system (ISTS) to non-windy states for RPO compliance. Moreover, the centre has plans to auction 10 GW-12 GW of wind capacity each year to meet the 60 GW target of installed wind capacity by 2022. Meanwhile, states have begun auctioning the available wind power capacity, led by Tamil Nadu, Gujarat and Maharashtra, with auctions for 500 MW each. Other states are soon likely to follow suit.

Tariffs discovered in the recent wind auctions are low compared to thermal power tariffs (Rs 3.45 per kWh for NTPC coal-based power). In fact, the lowest wind tariff (Rs 2.43 per kWh for GUVNL) even beat the lowest solar tariff (Rs 2.44 per kWh for Bhadla Solar Park). Such tariffs are expected to result in higher demand for cheaper power among discoms. The lack of transmission capacity is a considerable challenge for the wind power segment and the government has plans in place to address these constraints. The Green Energy Corridor project will help evacuate greater capacities of wind power through the grid. States like Tamil Nadu, Rajasthan and Andhra Pradesh are also working on strengthening their transmission infrastructure to address the issues of wind power curtailment and improve scheduling. Meanwhile, discom finances are slowly improving with the Ujwal Discom Assurance Yojana. Some states have proposed tariff hikes to address their losses, making discoms better suited to sign new PPAs for wind power development and reduce payment delays.

There has been significant progress in emerging areas as well. The solar-wind hybrid segment saw the commissioning of the first commercial-scale project in April 2018 in Raichur, Karnataka owned by Hero Future Energies and set up by Siemens Gamesa. The project entailed an addition of 28.8 MW of solar component to the existing 50 MW of wind power. In June 2018, SECI released a tender for 2.5 GW of ISTS-connected solar-wind hybrid capacity with a fixed upper tariff ceiling of Rs 2.93 per kWh. Meanwhile, in August 2018, the agency had tendered the 160 MW Ramagiri wind-solar hybrid plant integrated with energy storage.

Offshore wind power represents another emerging area for the country’s wind segment. While the National Offshore Wind Energy Policy was released in 2015, there has been little traction on the subject until now. In April 2018, the MNRE called for expressions of interest for 1,000 MW of wind power capacity to be developed offshore at the Gulf of Khambat, off the coast of Gujarat. This was followed by the installation of LiDAR for the assessment of the offshore wind resource at the site in July 2018 by the National Institute of Wind Energy.

Market movements

Market movements

The downward pressures in the wind power market have forced developers and manufacturers to realign themselves with the evolving revenue and profit trends. The resulting consolidation has compelled some to exit the market while others have gained market space. In a low-profit market, the quantum of returns has taken priority over the quality of returns, resulting in the expansion of project portfolios through inorganic growth routes.

Recent acquisitions in the segment point towards a similar trend. The wind segment saw enhanced mergers and acquisitions activity of $3.76 billion in 2017-18. Of this, $1.6 billion ReNew Power-Ostro Energy deal, the biggest transaction to take place in the history of Indian renewable energy sector was completed in April 2018. The company also acquired India Energy Limited for Rs 364 million in May 2018. In October 2018, Greenko was in final stages of acquiring Delhi-based Orange Renewables for $925 million and Skeiron Renewable Energy, a renewable energy platform set up by Suzlon Energy, Olympus Capital and Asia Climate Partners, for a value of Rs 35 billion.

The original equipment manufacturers are in an equally precarious position as they struggle to fill up order books to sustain themselves. In the quarter ended June 2018, Suzlon posted a loss of Rs 5.75 billion, falling from a net profit of Rs 480 million in June 2017. Meanwhile, Inox Wind posted a net profit of Rs 103.7 million in June 2018, a significant progress from the loss of Rs 390 million reported in the corresponding quarter in 2017.

Outlook

Outlook

To conclude, the wind power segment in India has definitely begun bearing the fruits of competitive bidding as the first projects are commissioned. While the policy-based tectonic shifts seem to have subsided, challenges continue to present themselves at regular intervals, in the form of PPA renegotiations, lack of transmission capacity, or even relatively high cost of capital. These hurdles have also played the role of keeping the market on its toes, resulting in dynamic evolution of business models and technology to realign to the changing demands in real time.

The government has announced a wind power auction trajectory, wherein at least 10 GW each would be tendered in 2018-19 and 2019-20. Considering that the country is close to 35 GW of installed capacity at present, another 25 GW will need to be added by 2022 to reach the 60 GW of installed capacity target, which translates to just over 6 GW of annual addition. While this has cleared the air regarding the tender trajectory for developers, given the capacity additions in 2017-18 and so far in 2018-19, the wind segment is likely to take at least 12 more months to gain the momentum to add such large capacities annually.

The role of states cannot be overlooked in the growth of the wind power segment. However, a few states have so far rolled out competitive bidding policies and a fewer still have conducted wind power auctions. It is imperative for at least the windy states to create a target-driven comprehensive policy framework for the development of wind power capacity to provide the much required momentum to the segment. Meanwhile, it is important for the wind power industry to look beyond 2022 and put in place actionable plans for a growth trajectory for 2030.