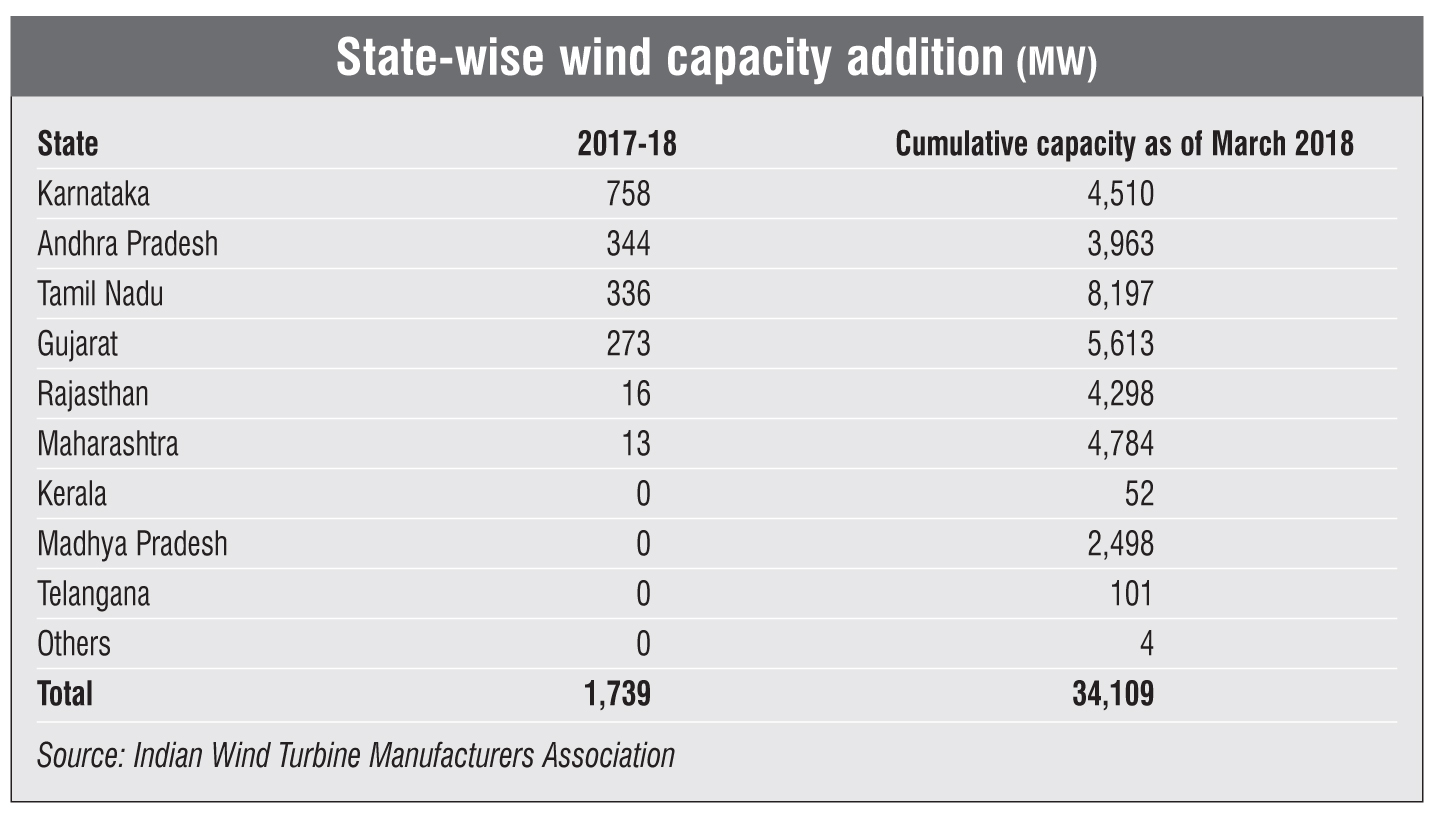

After a record capacity addition of over 5,400 MW in 2016-17, the wind power segment witnessed significantly subdued growth in 2017-18. Capacity addition dropped to 1,739 MW, a 68 per cent decline over the previous year. It is much lower than the capacity addition needed to achieve the 60 GW wind power target for 2022. The total installed wind capacity increased from 32.3 GW as of March 2017 to merely about 34 GW as of March 2018. Among states, Karnataka recorded the highest capacity addition of 758 MW in 2017-18, followed by Andhra Pradesh at 344.1 MW. On the other hand, Madhya Pradesh and Telangana did not add any capacity. In 2016-17, Andhra Pradesh had the highest installations of 2,190 MW, followed by Gujarat at 1,275 MW and Karnataka at 882 MW. While the record capacity addition in 2016-17 was on account of a combination of factors such as phasing out of accelerated depreciation benefits and generation-based incentives, the significant slowdown in 2017-18 can be attributed to the change in the project allocation process that determines wind power tariffs in the country.

Earlier, the electricity regulatory authorities of various states would fix a feed-in tariff (FiT), which guaranteed long-term payments at a predetermined price, and sign power purchase agreements (PPAs) with private wind power developers at that price. The year 2017 witnessed the transition to a competitive bidding mechanism of project allocation in the wind power space. For at least six months into this decision, the wind power segment was in a state of uncertainty since the auction guidelines were not finalised and there was also a growing risk that the state governments may backtrack on PPAs signed earlier as they sought lower tariffs. However, both risks were mitigated eventually. In December 2017, the government released the Guidelines for Tariff-based Competitive Bidding Process for Procurement of Power from Grid-connected Wind Power Projects. Based on these, the state governments have devised their own tender guidelines. The risk of state governments backtracking on their earlier commitments was mitigated.

The issue started with the discovery of the lowest bid tariff of Rs 3.46 per kWh quoted in February 2017. This prompted several discoms to openly voice their reservations about honouring the PPAs and letters of intent (LoIs) for nearly 3 GW of capacity in the pipeline. These included the discoms of Andhra Pradesh, which refused to purchase power from 1.1 GW of projects, Gujarat (250 MW), Karnataka (900 MW) and Tamil Nadu (500 MW). All these discoms had signed PPAs/LoIs at FiTs that were much higher than the bid tariffs realised in any of the wind auctions held so far. Since the PPAs were awaiting regulatory approval, the discoms approached the state electricity regulators to either cancel their PPAs or work towards a renegotiated rate. In a positive development, most of the regulators have ruled in favour of the developers that had already installed the projects. For instance, in December 2017, the Andhra Pradesh Electricity Regulatory Commission approved PPAs for 41 wind projects aggregating 841.32 MW. Prior to this, Karnataka’s power regulator approved certain old PPAs with wind energy developers at the pre-committed rates with the discoms.

Another big positive has been the series of wind power tenders released over the past few months. The Solar Energy Corporation of India has launched three tenders since February 2017, Gujarat has launched two, and Maharashtra and Tamil Nadu one each. Besides, NTPC has recently launched a 2 GW wind project tender. In total, about 9 GW of wind power capacity has either been tendered or is in the process of being tendered. This clearly implies that project development is going to be a high priority during the current year. As the challenges pertaining to project supply get resolved with continuous tender announcements, tariffs are going to stabilise, providing greater confidence to investors.

All in all, the segment looks set for higher capacity addition in 2018-19 and is expected to exceed the targeted capacity for 2019-20.