As the Indian solar power market continues to grow amid declining capital costs and tariffs, several opportunities have opened up for engineering, procurement and construction (EPC) contractors. The past few years have seen a steep rise in the installed solar capacity as the country strives to achieve the 100 GW target in the next five years. The EPC contracting market has also evolved over time, moving from only large complicated projects to smaller diverse assets. Its scope has extended to providing turnkey solutions, from concept and design to operations and maintenance. The international model of EPC management is also gradually gaining traction in the Indian solar market.

Outsourcing EPC work to competent contractors also helps in reducing the project risk, thus boosting financier confidence. For developers whose core competency is not project development but operations and investment management, hiring EPC contractors can be particularly beneficial. The concept of developing renewable energy projects as an investment is becoming increasingly popular in the Indian solar market as it is looking to rapidly increasing capacity over the next five years to meet the 100 GW target, thereby opening up opportunities for EPC contractors.

Key features of the solar EPC contract

An EPC contract includes the complete engineering and design of the project, the procurement of all necessary equipment and materials, and the construction and commissioning of the plant. These tasks are carried out within a stipulated time frame at a given price, as mutually agreed by the parties involved. In addition, the contract guarantees a specified performance level. The breach of an EPC contract by the contractor attracts financial penalty in the form of liquidated damages paid to the owner of the project.

There are several advantages of engaging an EPC contractor for the development of solar projects in India. As the price and scope of work are specified in the contract, any losses on account of cost or time overruns are borne by the contractor. In addition, the performance specification clause requires the contractor to provide performance guarantee and specific liquidated damages payable to the owner in case of failure to meet the requirements as laid down in the contract. To this end, the contractor is liable to provide repairs for defects that occur within the first 12 or 24 months of completion of performance testing of the project, as may be the case. These defects could pertain to the poor performance of the modules, trackers, inverters or any other equipment of the solar power plant installed by the contractor. In addition, the bank guarantee for the project is to be provided by the EPC contractor and not the owner, in case the project fails to deliver the performance level specified in the contract.

Cost trends

Solar EPC is a major component of the total project cost. It includes civil works, procurement and installation of equipment and construction of mounting structures, trackers, connectors, etc. According to the Central Electricity Regulatory Commission (CERC), in a utility-scale solar power project, EPC works up to the point of interconnection account for 79.86 per cent of the total project cost. As per the benchmark costs determined by the CERC for 2016, of the total project cost of Rs 53 million per MW, EPC costs stand at Rs 45.83 million per MW.

Meanwhile, the cost of EPC projects is declining along with module and balance of system prices. This can be attributed to the rise in the number of players in the segment, offering services at competitive costs. In addition, the increase in demand for solar power has encouraged investors to offer services at low costs to generate greater revenues through economies of scale. As the demand for solar increases and the competition becomes more intense, EPC costs are not likely to increase from the current levels.

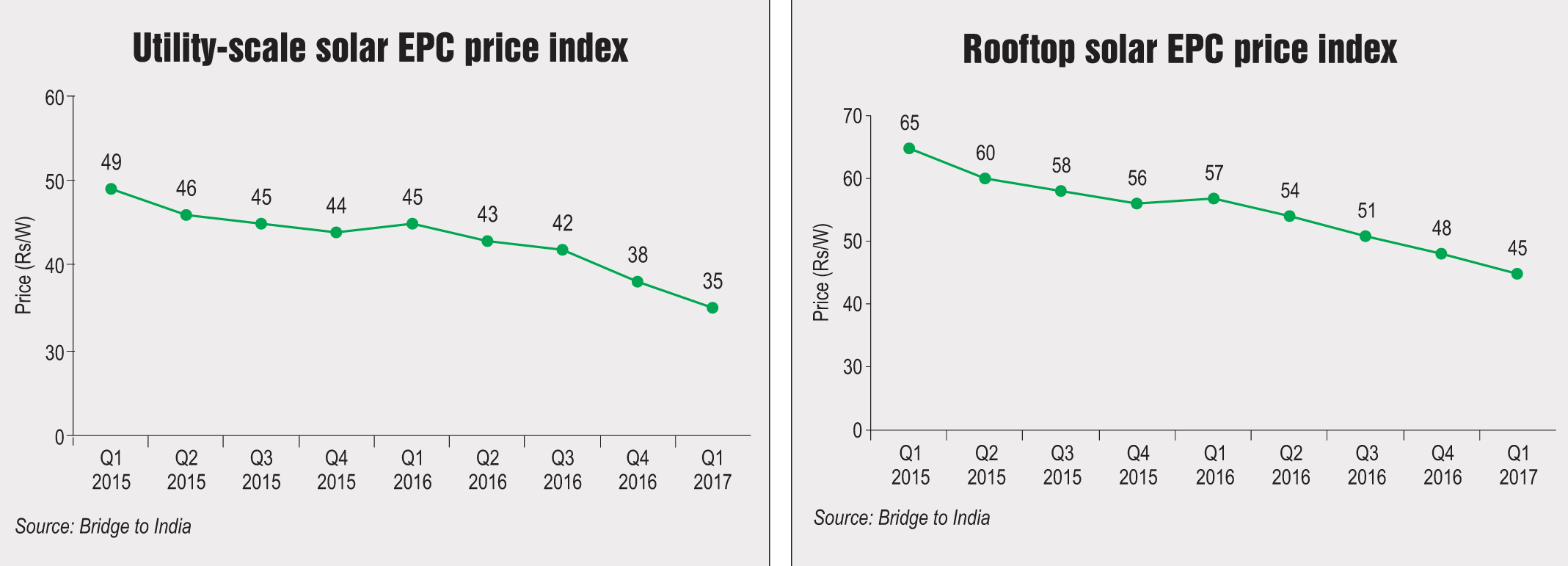

According to BRIDGE TO INDIA, EPC prices for the utility-scale solar market fell by about 8 per cent in the first quarter of 2017 from the fourth quarter of 2016 and 22 per cent year on year in 2016-17 over 2015-16. Over the past two years, solar EPC prices have declined at a compound annual growth rate of 8.7 per cent, from Rs 49 per watt in the first quarter of 2015 to Rs 35 per watt in the corresponding quarter in 2017. Meanwhile, in the rooftop EPC market, while the annual decline stood at 27 per cent, the quarterly decline was only 6 per cent. The prices fell from Rs 65 per watt in the first quarter of 2015 to Rs 45 in the same quarter of 2017, indicating a decline of 9 per cent compounded annually. In the first quarter of 2016, solar rooftop EPC prices increased by Re 1 per watt over the previous quarter due to multiple reasons. Since then, the prices have been falling consistently by Rs 3 per watt per quarter in 2016.

Market share

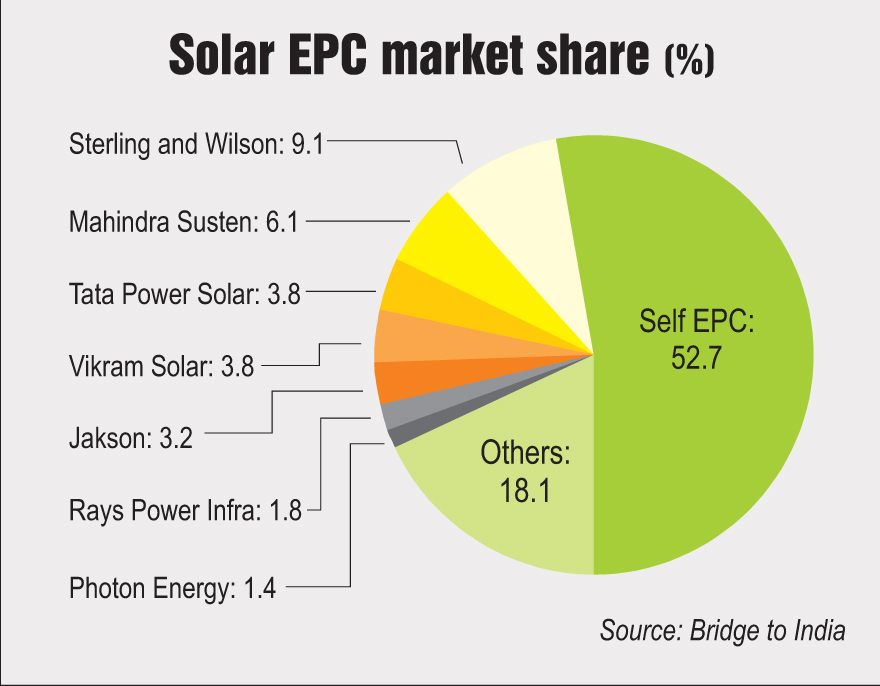

The solar EPC market has evolved over the years, with new companies entering the segment even as the trend of consolidation and vertical integration continues. According to BRIDGE TO INDIA, EPC works carried out by the project owner or investor (self-EPC) accounted for 47.5 per cent of the total projects installed in 2015-16, and this share increased to 52.5 per cent in 2016-17. This indicates a shrinking market for EPC contractors as more project owners carry out the EPC works themselves.

The remaining 47.5 per cent of the EPC market is highly fragmented. Sterling and Wilson is leading the market with a 9.1 per cent share in 2016-17, a decline of 0.5 per cent over 2015-16. Mahindra Susten accounted for a 6.1 per cent share in 2016-17, a steep decline from the largest market share of 10.4 per cent in 2015-16. Tata Power Solar has become the third largest player as its market share increased from 2 per cent in 2015-16 to 3.8 per cent in 2016-17. Larsen & Toubro, on the other hand, witnessed a decline from a 3.8 per cent market share to only 0.7 per cent.

Other major EPC players in 2016-17 include Vikram Solar (3.8 per cent), Jakson (3.2 per cent), Rays Power Infra (1.8 per cent) and Photon Energy (1.4 per cent). Companies such as Gamesa Solar and Premier Solar that accounted for 1 per cent of the market share each in 2015-16, held a share of less than 0.4 per cent in 2016-17. This is a result of the evolving solar EPC market where traditional market dynamics and business models are making way for new companies.

Key challenges

Although the 100 GW solar target has created ample opportunities in the segment, the EPC market segment continues to experience a number of challenges. One of the key challenges for EPC contractors is the goods and services tax as the earlier untaxed renewable energy equipment is now being taxed at 5 per cent. Moreover, there are several equipment categories that fall under the 12-18 per cent bracket as these do not pertain specifically to the renewable energy market. The ambiguity surrounding the taxes levied on solar energy equipment is also expected to delay EPC works of under-construction projects. This could result in EPC services becoming slightly dearer in the coming few months until the market realigns itself.

In addition, developers do not always deem it necessary to carry out feasibility studies and make detailed project reports to save small costs and increase their profit margins. These margins, according to industry estimates, hover around 5-10 per cent depending on the execution and management of the projects. In recent times, however, high labour costs, logistical issues and increasing commodity prices have led to further shrinkage of contractor margins.

The way forward

Solar EPC contractors have moved from being large-scale project facilitators to turnkey solution providers. However, the market for EPC contactors is facing a sharp rise in competition, not only from new companies entering the segment, but also from project developers that are carrying out EPC tasks themselves. Therefore, the declining trend in EPC prices and contractor margins is likely to continue. Going forward, while more opportunities are expected to open up given the increase in installed solar capacity, EPC contractors will have to evolve their service portfolio in order to survive in the growing market.