Amidst all the excitement pertaining to the progress in the grid-connected renewables space, the development and potential opportunities in off-grid renewable energy often get sidelined. However, in a much smaller way compared to its counterpart, off-grid renewable energy is increasingly being viewed as a means to bring sustainable and cheap electricity to the vast sections of the country that are yet to be connected to the electricity grid, especially in difficult terrain.

Today, with the advent of newer, more advanced renewable energy technologies, it is possible to generate electricity from various sources. While solar photovoltaic (PV) is the most popular technology currently in use for domestic electricity generation, there are many other sources that are waiting to be tapped. Biomass has long been used as a source of energy in India, but efficient ways of producing electricity from it are still to be applied.

On the policy front, a number of programmes have been launched in the past with the aim of providing basic energy access through off-grid solutions to remote regions. However, the progress of most rural support schemes and programmes has been hampered by muddled procurement processes and erratic implementation on the ground. Take for instance the case of solar pumps. Solar water pumps offer a compelling application of solar technology for many reasons – improving energy access in remote areas, replacement of dirty and costly diesel pumps and reduction in agricultural power subsidies. The government has, therefore, identified solar water pumps as a policy priority, with ambitious targets and substantial capital subsidy support. In 2014, it announced a target to install 1 million solar water pumps, equivalent to approximately 3,000 MW, for irrigation and drinking water by 2021. But the actual cumulative installed base stood at merely 25,000 pumps as of April 2016. The bleak performance is despite the government offering massive subsidies of as much as 75-95 per cent of the upfront capital cost of the pumps.

Significant headway has also been made in terms of entrepreneurial activity and private sector investment in the renewable off-grid energy segment, both driven by the policy push and market conditions. According to a research paper by The Climate Group, there are nearly 80 businesses (about 40 minigrid enterprises and 40 solar home system [SHS] manufacturers and distributors with an online presence) in the sector. However, the on-the-ground success of these ventures has been limited due to factors pertaining to an ambiguous future policy landscape and constrained financing. A number of barriers, of which many are unique to this market, make it difficult for companies to scale up and increase their reach. These barriers need to be overcome through focused and specialised solutions.

Renewable Watch takes a look at the scenario in the off-grid/decentralised renewable energy segment…

Case for off-grid

Statistics show that the total number of unelectrified villages in India stood at 1,845,240 as of March 2015. In addition to these unelectrified villages, there also exist a large number of hamlets/bastis in electrified villages that do not have access to electricity. The reasons could be power shortage, forced load-shedding or discom unwillingness to reach out to these areas due to financial unviability.

In terms of the number of households that lack adequate access to grid electricity, India currently has 77 million such households (about 360 million people), and another 20 million underserved households (approximately 95 million people) who receive less than four hours of electricity a day. While grid connectivity is expected to improve over the next 10 years, at the current rate of grid expansion, urbanisation and population growth, 70 million-75 million households are likely to not have access to grid electricity by 2024. Since 90 per cent of these households are in rural areas, a significant reduction in the 83 million rural households that are currently not served or are underserved by the grid is unlikely.

Rural underserved households are not equally distributed across India. Large sections of northern and eastern India have significant underserved populations. Further, two-thirds of the underserved rural population, or about 55 million households, live in Uttar Pradesh, Bihar, Odisha, West Bengal and Madhya Pradesh. The opportunity as well as the business case for off-grid enterprises to be successful is, therefore, largely concentrated in these states.

Current industry structure

According to a Climate Policy Group report, there are over 40 decentralised renewable energy players in the sector (with more than 100 kW of mini- or microgrid installations), which have adopted a wide range of technologies and business models, but most are struggling to achieve commercial viability. These include Azure Power, Gram Power, OMC Power, Husk Power, Saran Renewable Energy, Gram Oorja, Solkar, Desi Power, Biotech India, Mera Gao Power and Naturetech Infra. However, the majority are reliant on subsidies and/or grants, and only three have total installed minigrid capacities (capacity of all utilities put together) greater than 300 kW. However, a few enterprises such as Azure Power, OMC Power and Husk Power have shown signs of scaling, and these enterprises project strong growth over the next five years.

As capital-intensive businesses, these enterprises face a number of challenges. First, they need significantly high levels of upfront capital for plant installation. Second, debt is a primary unmet need of decentralised renewable energy enterprises as the cost of standard domestic financing is high. Further, current regulations make it difficult for these companies to get foreign financing or leverage equipment and inventory as collateral for lease financing (Azure Power is an exception due to its credentials in the grid-connected space). Third, these players face challenges surrounding affordability as well as collecting regular payments from consumers. This potential for non-payment is a significant risk for anyone wanting to invest in a microgrid project. Lastly, the lack of clarity about the government’s plans for grid extension and interactivity has led to concerns about the long-term viability of the microgrid-based business model. These challenges have made it difficult for enterprises to find financing from traditional sources. However, enterprises in the distributed renewable energy space have addressed these issues in different ways.

A similar trend can be observed in the SHS market, which comprises over 40 established players and new entrants trying to capitalise on the growth opportunity. While no single player has achieved meaningful scale to date, there are some large players linked to conglomerates that have succeeded in winning government tenders, but these enterprises have struggled to claim a sustained pipeline of direct customer sales.

The majority of the remaining players are small, selling less than 5,000 units a year, mostly through third-party distributors and dealers. There are a few players, however, who have seen success in reaching rural households by building their own rural distribution networks, focusing on branding and building relationships with consumers.

Issues around affordability have put pressure on these enterprises’ margins, as they keep prices low to stay competitive. As a result, there has been a significant emphasis on consumer finance. Gross product margins hover around 10-25 per cent, but after adjusting for marketing, transportation and distribution, margins, are closer to 1-5 per cent. A lack of meaningful scale has meant few enterprises have achieved profitability till date. Even leading players claim they need to grow to at least two to four times their current size in order to break even. As a result, the SHS market seems viable, but enterprises that sell only solar home systems are unlikely to see high returns. Despite these challenges, fast growth and cross/up-sell opportunities mean SHS enterprises could represent a high potential, albeit risky, investment opportunity for investors.

Policy push and progress report

Renewable energy-based decentralised applications are playing an important role in servicing the rural demand, thereby making microgrid systems and other off-grid products such as solar pumps, inverters and lights increasingly relevant for the power sector. In such a scenario, concerted efforts by the government could lead the way to harnessing the underlining potential in this segment.

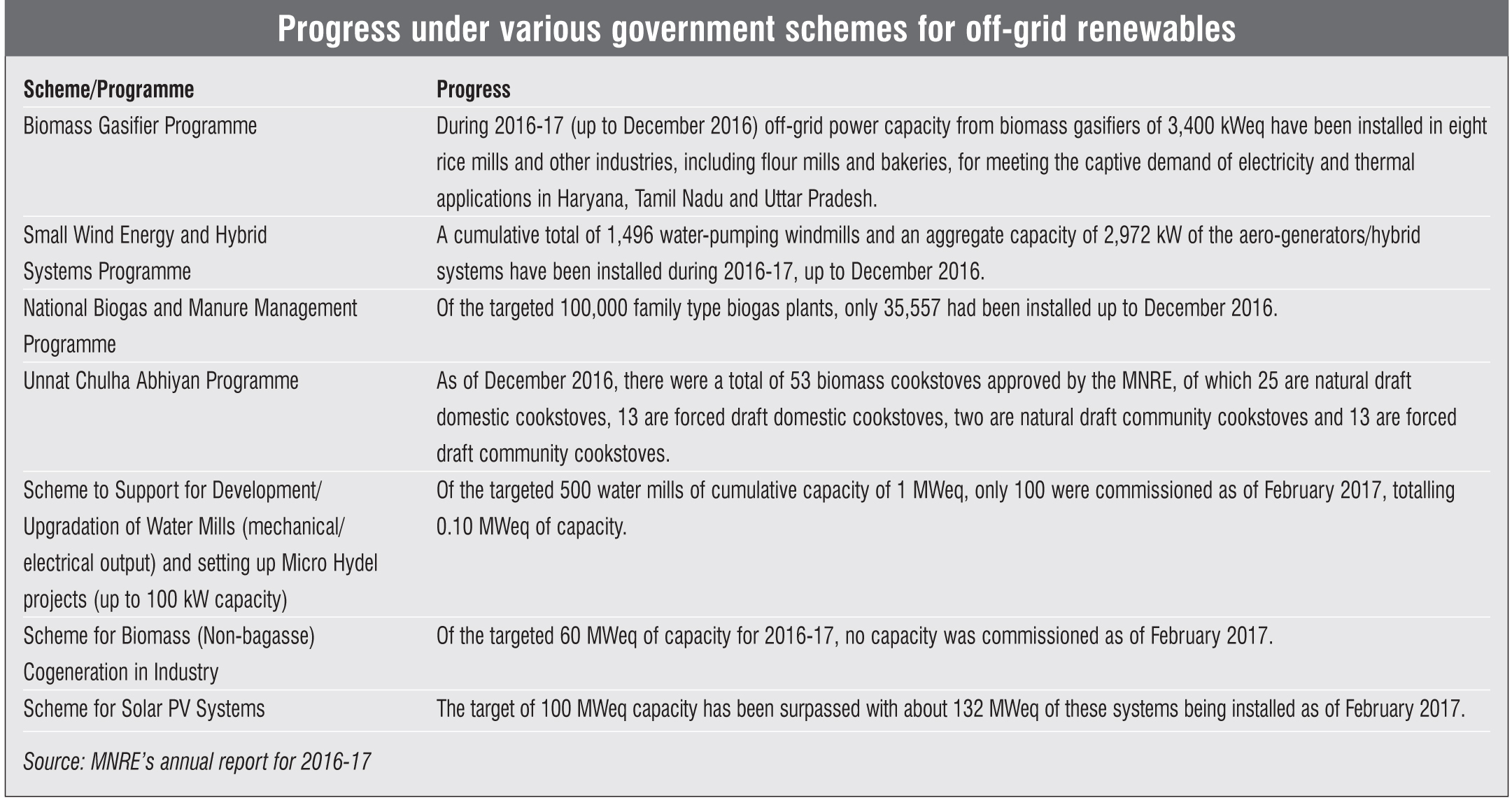

The Ministry of New and Renewable Energy (MNRE), through various central and state-level programmes, is providing budgetary as well as technical support to this segment. The MNRE, through its channel partners, is providing capital subsidy under various programmes to promote the deployment of renewable energy systems such as family-type biogas plants, solar water heating systems, solar cookers and other solar energy devices.

One such initiative is the Off-grid and Decentralised Applications Programme, being implemented under the National Solar Mission, in which mini/microgrids are a key segment. However, the development of this segment is lagging behind due to the nature of risk in such types of projects. To overcome these challenges and give greater thrust to minigrids, the ministry has started empanelling energy service companies as rural energy service providers, based on the specific eligibility criteria. The Ministry of New and Renewable Energy (MNRE) has also specified the benchmark cost for minigrid systems (of size >10 to 250 kWp) as Rs 300 per Wp, which mainly consists of solar power generation costs and associated public distribution network costs. In order to support these segments, the ministry is providing central financial assistance to solar PV micro/minigrid systems ranging from Rs 85 per Wp to Rs 115 per Wp, depending on the category of the state, and the size and mode of the project.

Another major initiative is the National Biogas and Manure Management Programme (NBMMP), under which family-type biogas plants are set up, where a minimum quantity of about 25 kg of organic biodegradable waste is available with a household, particularly in rural and semi-urban areas of the country. The progress under this programme, which was launched in 2002-03, has been slow. Against annual physical targets of 100,000 plants for 2016-17, about 35,557 family-type biogas plants are reported to have been set up till December 2016.

During the Twelfth Plan period (2012-17), about 394,000 biogas plants have been set up as of December 2016. The estimated average biogas production capacity of these biogas plants is 787,000 cubic metres per day. These biogas plants are leading directly to an annual replacement saving of about 8,750,000 LPG cylinders equivalent. With a cumulative installation of about 4,940,000 family-type biogas plants as of December 2016, about 41.1 per cent of the total estimated potential based on cattle dung waste only has been harnessed.

The Solar Energy Corporation of India is also focusing on solar off-grid generating systems, solar home lighting systems and various other forms of solar-based heating/cooling/thermal applications in the domestic, commercial and industrial segments. However, the progress again has been limited.

To give a push to the segment, the government is now streamlining the policy and regulatory process. Some of its recent initiatives are as follows…

Policy roadmap for microgrids

India has an appalling record in providing reliable grid electricity to large parts of the country. At the same time, the minigrid and microgrid segment has had limited success, with players in this space unable to scale up to profitable levels. Therefore, in June 2016, the MNRE released a national draft policy for mini- and microgrids. Under the policy, the aim is to deploy at least 10,000 renewable energy projects in the next five years in “unserved and underserved parts of the country”, with an average capacity of 50 kW per project. The draft policy provides the much-needed policy certainty to the segment and includes measures such as single-window clearances, grid connectivity and pricing visibility for the evolution of bankable business models. But surprisingly, it does not offer any direct financial incentives or subsidies. Grid power is heavily subsidised for residential and agricultural consumers, and the ability of these consumers to pay for more expensive mini/microgrid power continues to be a concern. Nonetheless, the policy is intended as a guideline for the states, which can adapt or modify it based on their local needs.

So far, Uttar Pradesh is the only state with a policy for minigrids. It aims to cover nearly 20 million households, about a tenth of its population, through minigrids. The state offers a 30 per cent subsidy for these grids, which may also be powered by wind, biomass or water, and must guarantee at least eight hours of electricity to homes and six hours for commercial needs. Importantly, the policy offers exit options when the areas have adequate grid supply; either the discom can receive power from the minigrid at an agreed tariff or the project can be transferred to the distribution company. Policy clarity, besides the promising business case for minigrid and microgrids, is one of the key reasons that the state is home to the largest number of microgrid operators. These include Azure Power, Gram Power, OMC Power, Husk Power, Saran Renewable Energy, Mera Gao Power and Naturetech Infra. Other states are yet to come up with microgrid policies.

Towards a kerosene-free India

For the longest time, one of the key challenges faced in the off-grid renewable energy arena was the government subsidies for kerosene, which made it difficult for off-grid products to displace kerosene, despite being more cost-effective on a lifecycle basis.

Kerosene is predominantly used as a lighting fuel in rural India, with less than 1 per cent of households using it as a primary cooking fuel. In urban-poor households, it is used for both lighting and cooking. A recent report by the Council on Energy, Environment and Water (CEEW) shows how shifting from kerosene to alternatives such as solar-assisted solutions for lighting and LPG for cooking could be economically beneficial for both the government and households. The shift would provide households with much better end services and avoids the adverse health impacts associated with kerosene use.

A recent analysis conducted by a research firm suggests that such a transition could result in annual savings of between Rs 80 billion and Rs 120 billion to the exchequer. Moreover, there is a bottom-up demand for such a change. The largest energy access survey in India, conducted by CEEW and Columbia University, shows that 78 per cent of rural households in six major states are willing to adopt solar-based lighting solutions in lieu of a reduction in their kerosene subsidy.

Against this backdrop, the government, in 2016, launched the Ujjwala scheme to reduce the consumption of kerosene by shifting from the subsidy on kerosene model to a direct transfer of funds to bank accounts of people below the poverty line. The scheme has resulted in a fall in kerosene supplies, from 6.3 million tonnes in the first 11 months of 2015-16 to 5 million tonnes during the same period in 2016-17. This is a big positive for the solar off-grid lighting industry. Besides, the government has been running massive awareness programmes to educate people about the commercial benefits of shifting to renewable solutions.

Conclusion

Although growing awareness, falling technology prices, proactive policymaking and improved access to finance have played a positive role over the years, these have not been enough to bring about change at the desired scale. The impetus for more rapid and large-scale growth of off-grid renewable energy products has to come from better technology and effective policies, and be sustained through functional business models and specialised financial solutions.