With the Twelfth Plan ending in March 2017, the Central Electricity Authority (CEA) released the draft National Electricity Plan (NEP) with a short-term perspective for the next five years and a long-term vision for 15 years. The draft NEP, released in December 2016 after a five-year interval, outlines the roadmap for the development of the power industry during the Thirteenth Plan period (2017-22). The draft is open to stakeholder suggestions and inputs. It also provides information on the suggested areas for capacity addition in generation and transmission keeping in view the economics, associated losses, requirements, grid stability, security of supply and quality of power. In addition, it lists grid integration mechanisms for new capacity, the different technologies available for power generation, transmission and distribution, as well as the optimum fuel choices according to requirements.

According to the NEP, under the Twelfth Plan, the country has achieved 115 per cent of its installed capacity targets for conventional sources of coal-based, hydro and nuclear power, of which about 56 per cent has come from the private sector. Also, the plan estimates that energy savings will be about 26 BUs, 137 BUs and 204 BUs for 2016-17, 2021-22 and 2026-27 respectively, over the 2015-16 values. The plan estimates a peak demand of 235 GW and an energy requirement of 1,611 BUs by the end of 2021-22, which is 17 per cent and 15.4 per cent lower respectively, than the projections by the CEA in the 18th Electric Power Survey report. The NEP also suggests that the peak demand and energy requirement will increase to 317 GW and 2,132 BUs respectively, by the end of 2026-27.

As per the NEP, 50,025 MW of coal-based power plants are at different stages of construction while 4,340 MW of gas, 15,330 MW of hydro, 2,800 MW of nuclear and 115,326 MW of renewable energy capacity is committed for construction, which will take the total estimated installed capacity addition to 187,821 MW. A significant forecast by the CEA is that no coal-based capacity addition is required for this period, apart from the capacity already under construction. This is primarily due to decreased power demand as well as the high growth of renewable energy capacity. The NEP estimates the coal-based capacity requirement to be 44,085 MW in 2022-27, which will be fulfilled by the capacity currently under construction.

The share of renewable energy sources in power generation is expected to increase to 20.3 per cent by 2021-22 and 24.2 per cent by 2026-27, as opposed to 14.8 per cent as of March 2016.

Renewable Watch takes a look at the CEA’s plans for the renewable energy sector…

Development so far

Over the previous three five-year plans, there has been a considerable increase in the country’s installed renewable energy capacity. While this capacity stood at 10,252 MW in 2007 (end of the Tenth Plan), it rose at a compound annual growth rate (CAGR) of 24.9 per cent to 24,920 MW by 2012. Given the concerted efforts of the government to provide a favourable business environment and incentivised financial mechanisms for harnessing renewable energy, the sector witnessed the largest development during the Twelfth Plan period. As of March 2016, the installed renewable energy capacity reached 42,839.4 MW at a CAGR of 14.5 per cent. It further increased to 50,017.9 MW by December 2016.

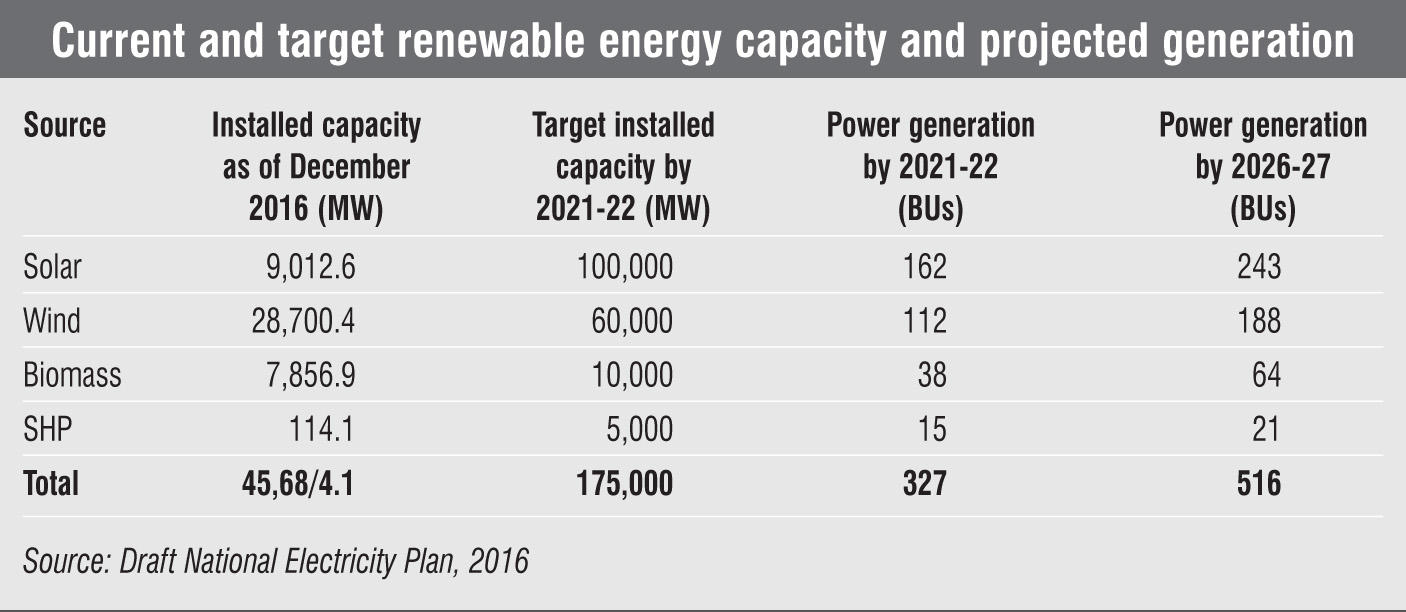

Although the wind energy segment is the oldest and most mature among all sources of renewable energy in the country, the solar segment has received maximum encouragement from the government and the private sector in the recent past. As of December 2016, the cumulative installed capacity for the solar segment stood at 9,012.66 MW, up from 6,762.85 MW in March 2016. Meanwhile, wind power capacity increased from 26,866.66 MW in March 2016 to 28,700.4 MW in December 2016. The installed small-hydro power (SHP) capacity stood at 4,273.47 MW in March 2016 and at 4,333.8 MW in December 2016.

Projections

The government has set a renewable energy target of 175 GW by the end of the Thirteenth Plan. Segment-wise, the target is to install a cumulative 100 GW of solar capacity, 60 GW of wind, 10 GW of biomass and 5 GW of SHP. The NEP has also set region-wise renewable energy targets, with the southern region expected to account for the largest share at 34 per cent, followed by the western region at 31 per cent and the northern region at 27 per cent. The eastern and north-eastern parts of the country will together contribute 8 per cent to the overall renewable energy targets.

Yearly targets have been defined in the NEP for the next five years for each segment (the 2021-22 figures have been adjusted to arrive at the total capacity of 175 GW). The target for rooftop solar is 5,000 MW in 2017-18, progressing by 1,000 MW each year to 8,000 MW in 2020-21 and 8,100 MW in 2021-22, the target for ground-mounted solar systems is 10,000 MW for all years till 2020-21, when it will reduce to 9,500 MW and further to 7,367 MW in 2021-22. For the wind energy segment, the target is 4,700 MW for 2017-18, 5,300 MW for 2018-19, 6,000 MW for 2019-20 and 6,700 MW for 2020-21, and 6,334 MW for 2021-22. In the biomass segment, the aim is to add 750 MW in 2017-18, with the target growing by 100 MW every year till 2019-20, by 50 MW in 2020-21 and by 5 MW in 2021-22. The SHP segment will add 100 MW to the total capacity each year during the five-year-plan period.

Renewable energy-rich states will play a major role in the fulfilment of these targets, which will result in an increase in the share of renewable power among these states. According to NEP projections, Maharashtra is likely to generate 13 per cent of its total power from renewable sources, the highest in any state. It will be followed by Tamil Nadu with 12 per cent, Andhra Pradesh with 11 per cent and Gujarat with 10 per cent. The share of renewable energy in power generation is expected to reach 8 per cent each in Karnataka, Rajasthan and Uttar Pradesh, while in Madhya Pradesh, it will be 7 per cent. These eight states are likely to contribute nearly 77 per cent to the country’s total installed renewable capacity at the end of the Thirteenth Plan.

The CEA will consider the achievement of these targets, along with another 100,000 MW during 2022-27, to estimate the power generation from renewable sources of energy. The NEP projects 327 BUs of generation from renewable sources by 2021-22. Of this, the solar segment will contribute nearly half the total power generated at 162 BUs, wind will contribute 34 per cent or 112 BUs, while biomass and SHP will account for 12 per cent and 5 per cent at 38 BUs and 15 BUs respectively. During the period 2022-27, the installed capacity is expected to reach 275 GW and the total generation is likely to be 2,132 BUs. Of this, the solar segment will generate 243 BUs, wind 188 BUs, biomass 64 BUs and SHP 21 BUs.

Recent achievements

The renewable energy sector has seen significant transformation during the past five years with major developments taking place. The year 2015-16 saw record installations of 3,300 MW and 3,019 MW in the wind and solar segments, which surpassed their targets by 38 per cent and 116 per cent respectively. In addition, 32 solar parks with a total capacity of 19,400 MW were sanctioned in 20 states. Also, 31,742 solar pumps were installed in 2015-16, higher than the cumulative number of pumps that had been installed since 1991, the year the programme for solar pumps was started. Solar projects worth 20,094 MW of capacity were tendered in 2015-16, of which 11,209 MW of capacity has been awarded and 9,695 MW is in the process of being awarded.

Several policy initiatives were taken during the period. To enable better grid integration and evacuation of renewable power, Rs 380 billion is being utilised for the Green Energy Corridors (GEC) project. The clean environment cess has been raised eight times, from Rs 50 per tonne of coal to Rs 400 per tonne. The cess received will be used to finance renewable energy projects and for the Ganga Rejuvenation project. Also, India led the formation of the International Solar Alliance, which brings together 121 countries committed to the development of solar energy.

Grid integration

Power from renewable sources of energy is independent of the grid requirements as opposed to generation from traditional sources, which can be programmed to match grid loads. Also, renewable power suffers from variability issues over a period of time such as a daily pattern for solar energy and a seasonal pattern for wind energy. There are also uncertainties, for instance, due to cloud cover, which further makes renewable sources of energy unreliable for integration into mainstream power distribution and transmission systems. Also, since renewable power is mostly generated at the distribution level or at the consumer-end as opposed to power from traditional sources, which is aggregated and then distributed, scheduling issues may affect the power supplied, especially during peak demand. The balancing of power from traditional sources to match the variability of supply makes grid integration of renewable power a major challenge.

Since renewable energy is concentrated in the eight solar- and wind-rich states, the distribution of power produced in these states becomes essential. The GEC project is a positive step in this direction, and is expected to strengthen the renewable energy evacuation and transmission network. Grid integration, however, comes at a cost that involves connecting the power generating station to the existing grid as well as upgrading the grid network to handle additional power. These costs have often constrained renewable energy development in remote locations.

Forecasting of power supply from renewable energy sources helps reduce the uncertainty associated with it, enabling generators to accommodate the operating reserves according to the most likely scenarios. The draft NEP suggests that renewable energy power generators and system operators must partner with the India Meteorological Department and the Indian Space Research Organisation for more accurate sky and weather information, specifically on cloud movement and formation for solar energy.

Conclusion

Renewable energy development in the country is dependent on the progress of multiple factors such as grid infrastructure, besides the installation of power plants. The renewable energy targets are expected to be realised by the end of the next five-year plan. However, to achieve these targets, various issues need to be addressed. These include grid availability, access to finance for renewable energy projects, availability and ease of land acquisition for these projects as well as better tools to reduce variability and uncertainty of power from these sources.

Although the renewable energy scenario, as considered by the CEA in the plan, affirms the country’s domestic and international renewable energy commitments, it could have serious consequences for the power sector as a whole. The plan suggests that no additional coal capacity is required till 2027 and, given the increase in renewable energy capacity, many existing coal-based power plants that are already running on low plant load factors may be rendered defunct. The government will need to ensure a balance in the development of the renewable energy sector with that of the conventional power sector to enable holistic growth of the country’s power industry.

By Ashay Abbhi