By Sakshi Bansal

By Sakshi Bansal

Pumped storage projects (PSPs) have long been the traditional solution for large-scale energy storage. PSPs offer many advantages, including long discharge durations of 6-10 hours or more, high round-trip efficiency of 75-80 per cent and the ability to provide various ancillary services to the grid. As costs continue to decline and revenue opportunities expand, the PSP market is poised for significant growth. The levellised cost of storage for PSPs is Rs 7.87-Rs 8.15 per kWh. This cost advantage increases in longer-duration applications, with PSPs benefitting from an operational life of 40-60 years.

Rising storage requirements driven by the rapid expansion of renewables have renewed interest in PSPs among policymakers, utilities and developers. PSPs have provided a much-needed revival to India’s hydropower sector, increasingly becoming an integral part of the country’s clean energy transition. They are gaining uptake among utilities as well as commercial and industrial consumers seeking reliable, round-the-clock renewable power.

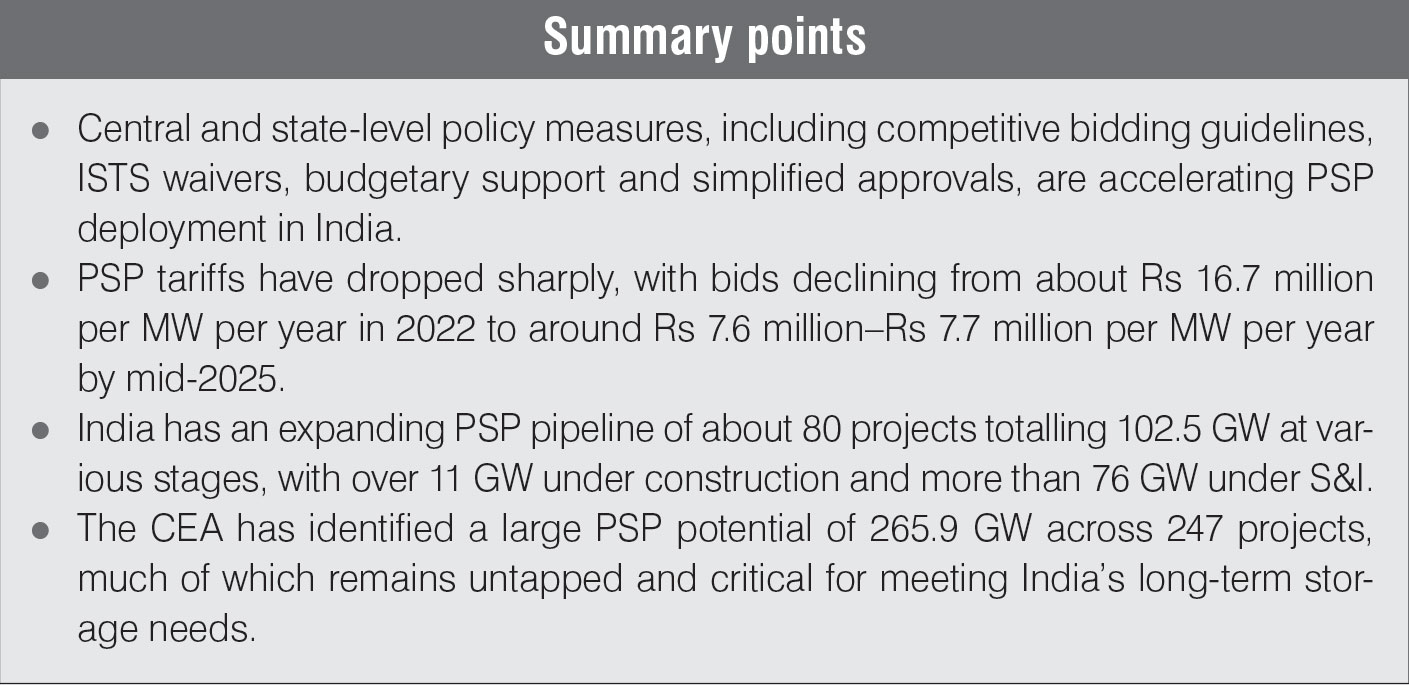

Market trends further indicate the maturation of the PSP segment. Tariff bids have declined sharply from about Rs 16.7 million per MW per year in December 2022 to nearly Rs 7.6 million–Rs 7.7 million per MW per year by mid-2025. These bids typically correspond to storage durations of six to eight hours, aligning well with system requirements for peak load management.

On the development front, the pipeline for pumped storage projects is expanding rapidly. As per the Central Electricity Authority (CEA), as of November 30, 2025, India has a total of 80 PSPs aggregating 102.5 GW at various stages of development. These include nine on-river PSPs in operation with a total capacity of 5,246 MW, with two each in Telangana, Maharashtra and Gujarat, and one each in Uttarakhand, Tamil Nadu and West Bengal. Meanwhile, there is only one off-stream operational PSP with a capacity of 1,680 MW. However, only eight plants with a total capacity of 5,485.6 MW are operating in pumped mode, whereas 1,440 MW of capacity across two sites in Gujarat remains non-operational in pumped mode. Further, four on-stream (4,350 MW) and six off-river (7,520 MW) PSPs are under construction. Meanwhile, one on-stream and four off-stream PSPs, with a capacity of 1,000 MW and 5,580 MW, respectively, have been approved by the CEA. One on-stream PSP of 640 MW is currently under examination. Survey and investigation (S&I) activities are under way for 20 projects totalling 30,690 MW. Of these, one is an on-river project of 1,000 MW and 19 are off-river projects totalling 29,690 MW. Additionally, one on-river 500 MW PSP and 33 off-river PSPs with a total capacity of 45,350 MW are under S&I but not in the CEA.

Policy developments

Recognising the crucial role of PSPs in renewable energy integration, various policy measures have been introduced to encourage adoption. In February 2025, the MoP introduced tariff-based competitive bidding guidelines for the procurement of storage capacity from PSPs, providing much-needed policy clarity. Considering the distinct requirements of PSPs with respect to land acquisition, permits and clearances, project timelines and performance parameters, separate guidelines for PSPs have been formulated to address the unique nuances of PSP technologies. The guidelines have introduced two procurement modes. In Mode 1, procurers can develop PSPs at government-identified sites on a build-own-operate-transfer basis for 25-40 years. The procurer will be responsible for all pre-feasibility activities before handing over the project to a successful bidder via a special purpose vehicle. In Mode 2, PSPs can be developed at sites identified by bidders, or based on already commissioned or under-development projects, on a build-own-operate basis for 15-40 years.

In June 2025, the MoP issued amended specific provisions for hydro PSPs. Under the revised provisions, a 100 per cent interstate transmission system (ISTS) charges waiver will be granted to hydro PSP projects for which construction is awarded on or before June 30, 2028. However, hydro PSP projects awarded after June 30, 2028, will not be eligible for the waiver. Furthermore, in August 2025, the power ministry issued a notification for the revision of the capex limit for hydro projects requiring CEA concurrence for PSPs. Projects for setting up hydro generating stations with an estimated capital cost above Rs 30 billion require the CEA’s approval. However, off-stream closed-loop PSPs, regardless of their capital cost, will be exempt from the requirement of CEA approval. Developers of exempted projects may still seek technical guidance from the authority.

In June 2025, the MoP issued amended specific provisions for hydro PSPs. Under the revised provisions, a 100 per cent interstate transmission system (ISTS) charges waiver will be granted to hydro PSP projects for which construction is awarded on or before June 30, 2028. However, hydro PSP projects awarded after June 30, 2028, will not be eligible for the waiver. Furthermore, in August 2025, the power ministry issued a notification for the revision of the capex limit for hydro projects requiring CEA concurrence for PSPs. Projects for setting up hydro generating stations with an estimated capital cost above Rs 30 billion require the CEA’s approval. However, off-stream closed-loop PSPs, regardless of their capital cost, will be exempt from the requirement of CEA approval. Developers of exempted projects may still seek technical guidance from the authority.

Earlier, the union cabinet approved a budgetary support scheme of Rs 125 billion for developing PSP projects totalling 15 GW. Also, the CEA revised guidelines for detailed project reports to speed up approvals. The changes include shorter documentation requirements, online submissions, and the elimination of mandatory cost and financial chapter approvals. For off-stream projects, developers no longer need to submit alternative reservoir layouts or certain geological studies, which could reduce approval time by four to five months. Additionally, PSPs have been classified as renewable sources, and budgetary support is being provided for funding enabling infrastructure for hydropower projects and PSPs.

Apart from central policies, several states have introduced dedicated policies to promote PSPs, reflecting growing recognition of their role in grid stability and renewable integration. Bihar notified its Pumped Storage Promotion Policy in July 2025, covering state-identified, CEA-identified and self-identified off-stream sites, including projects at the survey and investigation stage, while excluding projects already commissioned or under construction. The Tamil Nadu Pumped Storage Projects Policy 2024, aims to leverage PSPs for sustainable energy growth. It allows PSP developers to build captive solar or wind capacity (with energy banking provisions) to meet input power requirements.

Uttarakhand launched its PSP policy in September 2023 for projects above 25 MW, including those identified by the state government/CEA and as well as those under the S&I stage. Maharashtra approved its PSP policy in 2023, earmarking 18 sites in the Sahyadri ranges with a potential of over 27 GW to support grid reliability and co-located hybrid projects. Meanwhile, Rajasthan’s Renewable Energy Policy, 2023, targets 10 GW of hydro, pumped storage and battery storage capacity. Odisha’s Renewable Energy Policy (2022–2030) and Karnataka’s Renewable Energy Policy (2022–2027) included pumped storage to strengthen renewable integration and encourage public and private investment. Furthermore, Himachal Pradesh’s Energy Policy, 2021, includes PSPs as part of its broader energy diversification strategy. Madhya Pradesh issued PSP development guidelines in May 2023, highlighting site allotment, fiscal incentives and timelines. The state has an estimated PSP potential of 11.2 GW, which could be further expanded through closed-loop and retrofit projects. Moreover, Andhra Pradesh, having identified over 33 GW of PSP potential, notified its Pumped Storage Hydro Power Projects Policy in December 2022, while Chhattisgarh approved its PSP establishment policy in 2022, identifying seven sites with around 10 GW of potential. While these state-level initiatives are encouraging, their effectiveness will depend on alignment with the central government’s policy framework.

The way forward

India’s PSP roadmap is clearly defined, with storage requirements expected to rise sharply over the next decade. According to the National Electricity Plan 2023, PSP capacity is projected to reach 7.45 GW/47.6 GWh by 2026-27, 18.98 GW/128.15 GWh by 2029-30 and 26.69 GW/175.18 GWh by 2031-32. The country’s identified PSP potential stands at 265,926 MW across 247 projects, which remains largely untapped. Furthermore, meeting the CEA’s projected need of 74 GW of storage by 2032 will require the commissioning of nearly 8 GW of PSP capacity annually, highlighting the importance of timely bidding and contract awards.

While developer interest is strong, actual progress will depend on faster execution. This will require standardised bidding documents, improved coordination among approving authorities and closer alignment of state policies with the central framework. Project risks related to land acquisition, environmental and forest clearances, geological uncertainties and long development timelines must be addressed through rigorous techno-commercial due diligence. Inviting bids after securing land, finalising detailed project reports and obtaining key clearances would help lower risk perception and tariffs. Further, strengthening payment security, streamlining regulatory processes, and enabling predictable cost recovery through inflation-linked operations and maintenance charges and standardised cost benchmarks will help improve bankability.

Net, net, as variable renewable energy capacity expands, PSPs will be indispensable in providing clean balancing power, making their accelerated deployment central to India’s grid reliability and energy transition.