As the global energy landscape undergoes a historic shift towards sustainability, investment in energy transition assets is gaining unprecedented momentum. Despite geopolitical uncertainty and economic volatility, investors remain committed to funding clean energy initiatives, with an increasing focus on electrification, energy efficiency and renewable infrastructure.

Renewable Watch presents an excerpt from KPMG’s report titled “The Energy Transition Investment Outlook 2025 and Beyond”. Based on insights from 1,400 senior executives across 36 countries and territories, the report highlights key trends, challenges and opportunities shaping this transition…

Capital requirement for energy transition

The transition to clean energy continues to attract significant capital. According to the report, 72 per cent of investors believe that energy transition investments are rapidly increasing. Global energy investments are expected to reach a record high of $3 trillion in 2024, with $2 trillion allocated to clean energy technologies and infrastructure, nearly double the investment in fossil fuels.

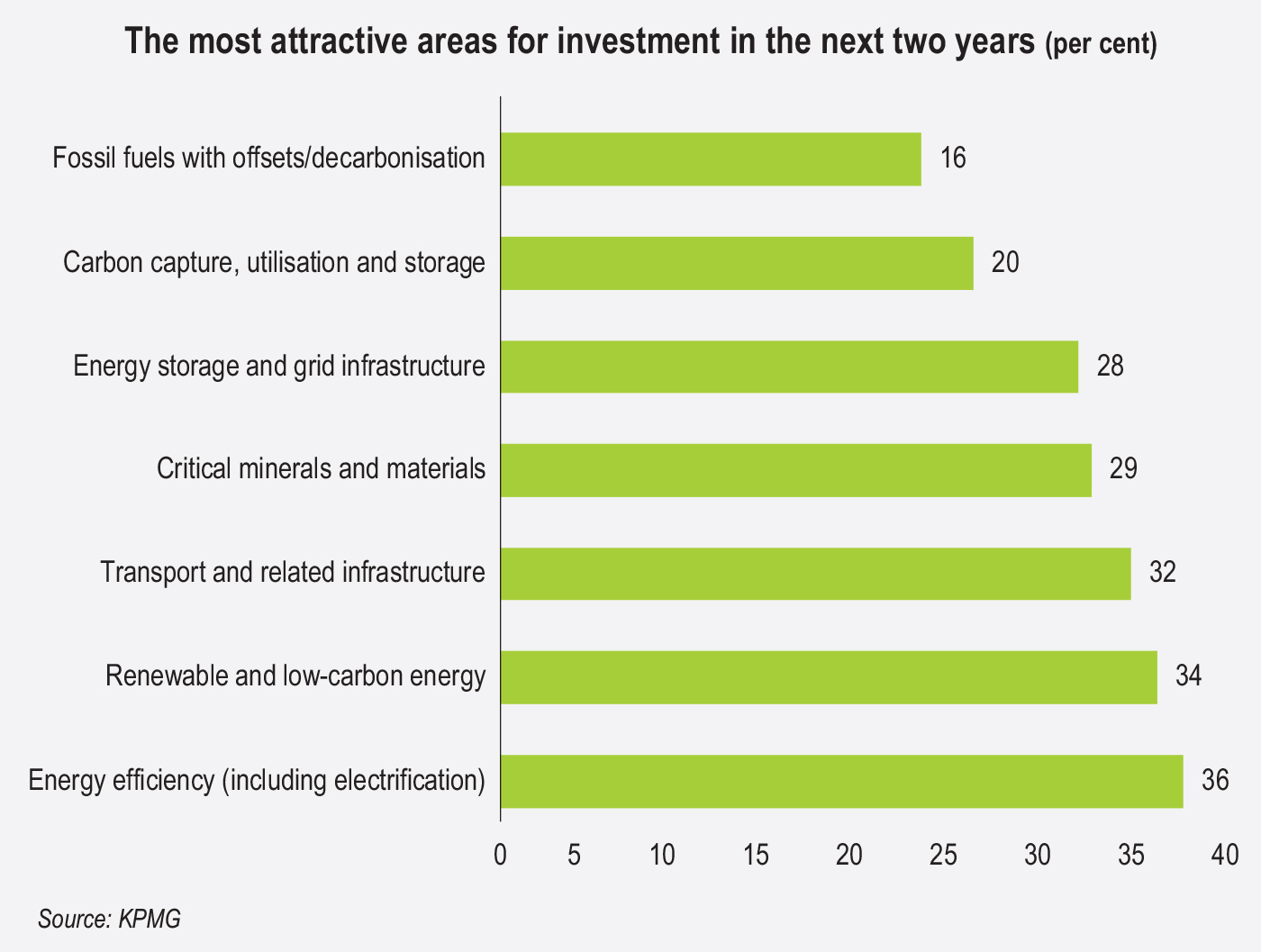

Investors are leveraging a diverse range of opportunities, including energy storage, electrification and transport infrastructure. The report states that 56 per cent of investors have funded energy storage and grid infrastructure projects, while 51 per cent have focused on transportation and related infrastructure. With increased funding in critical minerals and materials for battery storage, the supply chain for clean energy is evolving rapidly. In addition, corporate investment in renewables and carbon reduction is expected to increase, with heavy industries such as steel and cement driving the demand for green energy solutions.

Role of fossil fuels

Despite the rapid growth of renewables, fossil fuels are expected to remain a critical part of the energy mix over the next two decades. According to the report, while there is a shift towards sustainable assets, only 25 per cent of current investors have stopped making new investments in fossil fuels. Although the pace of renewable adoption can sometimes obscure the world’s continued dependence on fossil fuels, replacing the vast share of fossil fuel energy in the current mix, at 82 per cent, remains a significant global challenge.

Drivers for clean energy investments

Various investor types have distinct motivations for investing in energy transition assets. A diverse range of investors are driving this transition. These include governments, infrastructure funds, private equity groups, energy companies and energy-intensive businesses, each with its own context, objectives and risk profile.

According to the report, investors can be broadly divided into two groups – financial investors (banks, asset managers, venture capital firms, private equity and infrastructure funds, etc.) and operational investors (energy utilities, oil and gas, and natural resources companies, as well as the automotive and transportation industries). One major difference between these groups is that operational investors are active users of the assets they invest in, whereas financial investors provide funding and expertise for investment returns. Corporate reputation is also a notable factor, with operational investors prioritising reputation while financial investors put risk-return considerations first.

For financial investors, key drivers include financial returns, portfolio diversification, regulatory compliance and risk management. These factors typically remain consistent across financial investors, regardless of their specific themes or strategies. Meanwhile, Operational investors prioritise energy security and regulatory compliance, followed by considerations such as reputation, social impact, financial returns, technological advancement and environmental impact.

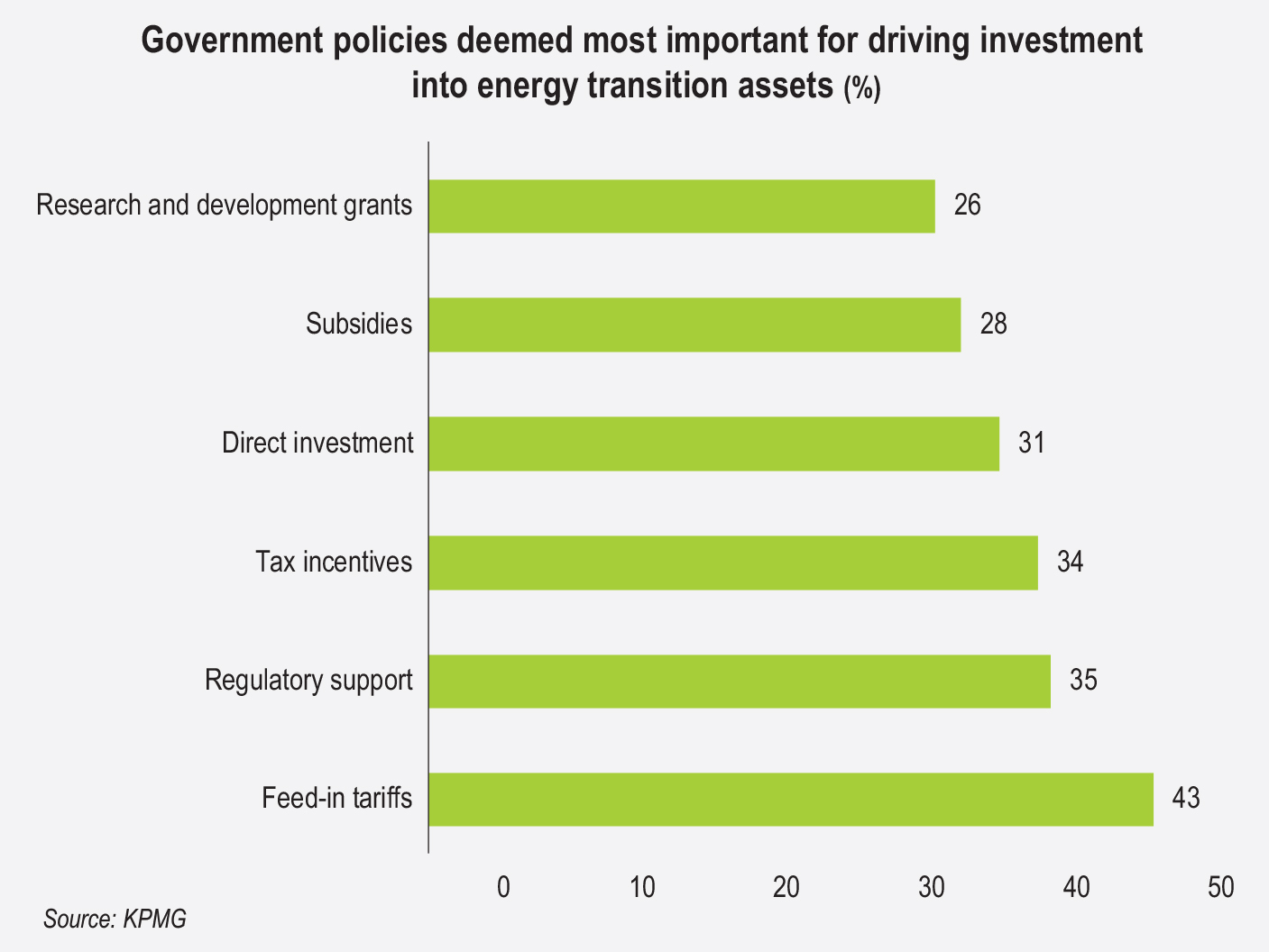

Investment barriers

Policy or regulatory risks are the most significant obstacles to investing in energy transition assets. Geopolitical and economic uncertainty has made investors more cautious, with survey respondents identifying market volatility or uncertainty as the second-largest barrier. However, the impact of volatility is not uniform and investors with a long-term outlook remain undeterred by short-term fluctuations, especially when investing in a trend with strong long-term momentum. The third barrier is uncertainty in technology performance, compounded by high operating costs and market competition. Investors are often reluctant to invest in energy transition assets due to environmental factors affecting the performance of renewables like wind and solar, as well as concerns over maintenance costs and asset integration into broader energy networks. For new or emerging technologies, key challenges include demonstrating long-term reliability and performance, including efficiency, durability and operational costs.

A stable regulatory environment is essential for long-term investment. However, 51 per cent of investors cite regulatory and policy uncertainty as a top barrier to energy transition funding. Government incentives such as feed-in tariffs, carbon taxes and direct subsidies are critical to maintaining investor confidence. According to the report, regions with strong policy frameworks, such as Europe and North America, attract the highest levels of investments. Policy conditions for investing in energy transition assets are expected to improve in China, the US and Europe over the next two years, while the outlook for India, Japan and particularly Australia is less optimistic.

New ESG reporting standards and international regulatory frameworks are reshaping the investment landscape. The introduction of mandatory climate risk disclosures in key markets is expected to enhance transparency, ensuring that companies align their strategies with global decarbonisation targets. Investors are also increasingly assessing green hydrogen and energy storage policies, which will play a major role in future energy systems.

Power of partnerships

Collaborations across industries and between the public and private sectors are key to mitigating risks. According to the report, 94 per cent of energy transition investors prioritise finding partners that can share financial and operational risks. Strategic alliances in areas such as grid modernisation, hydrogen hubs and storage solutions are driving new investment models. Public-private partnerships are instrumental in accelerating the deployment of clean energy infrastructure. Investors are increasingly engaging with energy companies, asset managers and consultants to navigate market complexities. The report also highlights an emerging trend where private equity and venture capital firms collaborate with renewable developers to scale innovative technologies such as floating offshore wind, direct air carbon capture and synthetic fuels.

Regional investment trends

Investment in energy transition is concentrated in three major regions – Europe, North America and East Asia. These areas provide favourable conditions such as regulatory support, infrastructure readiness and technological innovation. In the survey, 54 per cent of investors have prioritised Europe, 52 per cent North America and 52 per cent East Asia in their recent investments. Emerging markets such as the Middle East, Southeast Asia and sub-Saharan Africa present high growth opportunities, though challenges such as policy instability and infrastructure gaps must be addressed. Saudi Arabia, for example, plans to increase its renewable energy generation capacity from 5 GW to 130 GW by 2030, while the UAE is investing significantly in carbon capture and hydrogen production. However, only 15 per cent of total clean energy investment is currently directed towards emerging markets, even though these regions account for 67 per cent of the world’s population. Increasing investment in these markets is crucial for a truly global energy transition.

The path forward

The energy transition is one of the significant investment megatrends in history. To meet the ambitious COP28 targets of tripling renewable energy capacity and doubling energy efficiency rates by 2030, global investment in clean energy must rise significantly. Investors are increasingly looking beyond traditional asset-heavy projects, exploring opportunities across supply chains, software and advisory services.

With interest rates expected to ease and supply chain disruptions diminishing, the investment outlook for energy transition assets remains strong. The cost of key battery metals (lithium, cobalt and nickel) has fallen sharply over the past year, with further decreases expected. Additionally, the cost of solar panels is at an all-time low. Photovoltaics have become so affordable that residents in the Netherlands and Germany are using them to build garden fences, even though the sunlight angle is not ideal.

Investors are adapting their strategies to align with evolving policy landscapes, technological advancements and regional market dynamics. Those who navigate policy uncertainties, form strategic partnerships and capitalise on emerging technologies will be well positioned to drive and benefit from the future of sustainable energy.