Asia is one of the fastest growing regions in the world, projected to require $6.35 trillion worth of infrastructure investments through 2030. Such rapid economic development will mean a significant increase in energy consumption, which will result in significant new capacity additions. South Asia needs to transition to modern and clean energy sources, given the forecast of burgeoning energy demand in the near future and the region’s vulnerability to climate change.

India, which is one of the major South Asian countries, has pledged to install 500 GW of non-fossil fuel electricity capacity, sourcing half of all its energy requirements from non-thermal sources, by 2030. Reaching these important targets will require capital investments of over $500 billion in the renewable energy sector over the next eight years. Further, the government, in its quest to make the country a $5 trillion economy by 2025, has announced the Gati Shakti Plan, which envisages an investment of $1.5 trillion in infrastructure by 2024-25.

Besides a conducive policy and regulatory framework, a combination of conventional and new financing instruments is required to mobilise capital for India’s ambitious clean energy and infrastructure targets. Infrastructure investment trusts (InvITs) are one such financing instrument, which could contribute significantly to the investment needs of the renewable energy sector.

Renewable energy financing needs

As of 2020, India was ranked fourth globally in wind power, fifth in solar power, and fourth in renewable energy installed capacity. This was achieved through multiple fiscal/policy incentives launched by the Government of India over the past decade, including accelerated depreciation, generation-based incentives, tax holidays, viability gap funding and soft loans from the Indian Renewable Energy Development Agency. However, as the sector matured, these incentives were gradually replaced by commercial lending in various forms of debt, equity and mezzanine finance. Investments grew almost five-fold in the period 2015-21.

Even though the renewable energy sector has grown exponentially since 2010, solar and wind capacity additions slowed down towards the end of the decade. Several internal and external factors impacted the growth, such as rupee depreciation and lower tariffs, affecting investor sentiment and leading to sluggish growth in the renewable energy sector. Coupled with the nature of India’s financial markets, characterised by high capital costs and lack of adequate debt financing, this poses financing challenges for the sector. In the past, India’s renewable energy sector has raised funds from multiple sources, including strategic equity investors, commercial banks, non-banking financial companies (NBFCs), development financial institutions and private equity (PE) investors. The outstanding debt exposure to the power sector by Indian banks and NBFCs totalled approximately $168 billion in March 2020.

While the current policy framework has allowed India to reach the 100 GW renewable energy capacity mark, the new targets for 2030 necessitate further reinforcement of that support, especially in terms of capital deployment. Refining public-private partnership policies, building institutional capacity, lowering costs of capital, encouraging novel financing instruments and frameworks, and developing new business models can help create the investment climate required to achieve India’s green goals.

Out of the 500 GW capacity announced at COP26, it is estimated that 425-450 GW will be contributed by renewable energy, with another 70-80 GW coming from large hydro. This will entail the addition of nearly 28 GW of solar and 12 GW of wind capacity annually, which will require a cumulative investment of $163 billion, entailing debt financing in the range of $121 billion, and $41 billion of equity. Indian banks have limited ability to ramp up lending to the renewable energy sector, considering the current high levels of debt exposure to the power sector ($168 billion).

Benefits of InvITs

The Securities and Exchange Board of India (SEBI) rolled out the InvIT regime in 2014. Since then, InvITs have been registered across infrastructure assets such as roads, power transmission facilities, telecom towers and gas pipelines. InvITs are likely to gain significant traction over the next few years, and have the potential to channel significant long-term capital (such as pension and insurance funds) into the Indian infrastructure sector.

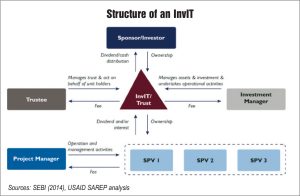

An InvIT is a pooled investment vehicle, like a mutual fund, in which an individual and/or institution buys units. It is a way of pooling funds to invest in an asset. InvITs are designed to offer a more stable and liquid financial instrument for investment in infrastructure.

InvITs facilitate the recycling of capital over short intervals and enable subsequent reinvestment in new/greenfield projects, thus accelerating the transition to clean energy. Renewable energy projects require high amounts of capital expenditure, with returns on these projects generated over long periods of time (15-20 years). For this reason, investments made by renewable energy developers are tied up, limiting cash reserves for investment in new projects. To undertake fresh capital expenditure and build new assets, renewable energy developers may need to resort to external borrowing or asset monetisation. InvITs unlock the true value of existing operational assets and help remove funding limits and increase equity for renewable energy developers, which can then be reinvested.

In the past, banks and public funds were the major sources of finance for renewable energy projects. However, with greenfield renewable energy projects, developers are faced with multiple demands from financial institutions, such as upfront security creation, stringent lending terms, corporate guarantees and negative liens on shares, in addition to the issues posed by asset-liability mismatches. This is where InvITs provide true ease of funding and can become a game changer for the renewable energy sector in India. The major benefits of using InvITs as a financing instrument for renewable energy developers include access to a larger pool and constant flow of capital, higher valuation, the ability to raise money without the need to list, and debt financing. It is also helpful for investors as it provides a global platform for investment in renewable energy projects and securing assets with low volatility, offers attractive long-term investment and a tax efficient structure, and allows greater control over assets.

Market potential of InvITs

InvITs have been more actively used in India over the last three to four years. As per CRISIL estimates, InvITs can raise more than $100 billion over the next five to six years. However, investors in India must be encouraged to exercise the InvIT option, as evidenced by the fact that Indian InvITs constitute only 0.7 per cent of the market-cap-to-GDP ratio, compared to 20 per cent in Singapore and 7 per cent in Hong Kong.

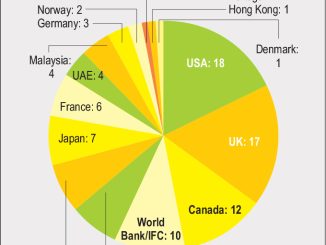

In the past, India has seen many large investors, including pension funds, insurance funds, sovereign funds, development finance institutions and PE firms invest heavily in the renewable energy market. Key investors active in the Indian renewable energy space include KKR, Caisse de dépôt et placement du Québec, the Canada Pension Plan Investment Board, Temasek Holdings, the World Bank’s International Finance Corp, Goldman Sachs, Brookfield, SoftBank, JERA Co., Inc., GIC Holdings Pte Ltd, Global Infrastructure Partners, Commonwealth Development Corporation Group Plc, EverSource Capital, Reliance Nippon Life Insurance Company, and Copthall Mauritius Investment.

Pension Plan Investment Board, Temasek Holdings, the World Bank’s International Finance Corp, Goldman Sachs, Brookfield, SoftBank, JERA Co., Inc., GIC Holdings Pte Ltd, Global Infrastructure Partners, Commonwealth Development Corporation Group Plc, EverSource Capital, Reliance Nippon Life Insurance Company, and Copthall Mauritius Investment.

With their current portfolios and future investment plans, it is estimated that these global investors have the appetite to invest anywhere between $100 million and $500 million in a single transaction, and act as anchor investors, provided other requirements such as taxation and transaction structure are aligned with their investment policies. Assuming a conservative investment of $100 million by a single investor, which may act as the anchor investor, the total equity capital base for an InvIT works out to be $400 million. With a leverage of around 50 per cent, the minimum scale of investment for a renewable energy InvIT is expected to be around $800 million at the time of issuance. If the anchor investor is large, the asset portfolio investments can easily double in one to two years post of issuance.

Limitations

As per regulations, InvITs must be AAA rated. However, in renewable energy, many PPA counterparties are discoms whose financial and operational performance is not up to the mark, and so they do not have good credit ratings. Second, although long-term PPAs/offtake agreements have been signed for renewable energy projects, providing clear visibility on tariffs over the next 20 years, there have been instances of governments/regulators trying to renegotiate or revise the terms of PPAs. This could have a detrimental impact on revenues, thereby affecting the stability and predictability of cash flow, which forms the basis of the InvIT structure. Third, only operational assets can be transferred to InvITs with stable and predictable cash flows, and the growth potential of such assets is limited.

The policy and regulatory framework for InvITs has been evolving over the past three to four years. The financial instrument is relatively intricate and needs greater understanding and acceptance among investors. The multifaceted nature of InvITs limits participation from all investor classes, and requires a greater understanding of underlying renewable energy assets. Moreover, the size of an InvIT issue is also critical for attracting large pension funds and other investors, as they operate with minimum investment thresholds. Therefore, smaller InvITs may not attract investor interest. Further, considering the smaller size of renewable energy assets, a lot of assets need to be bundled together to achieve such critical mass.

The way forward

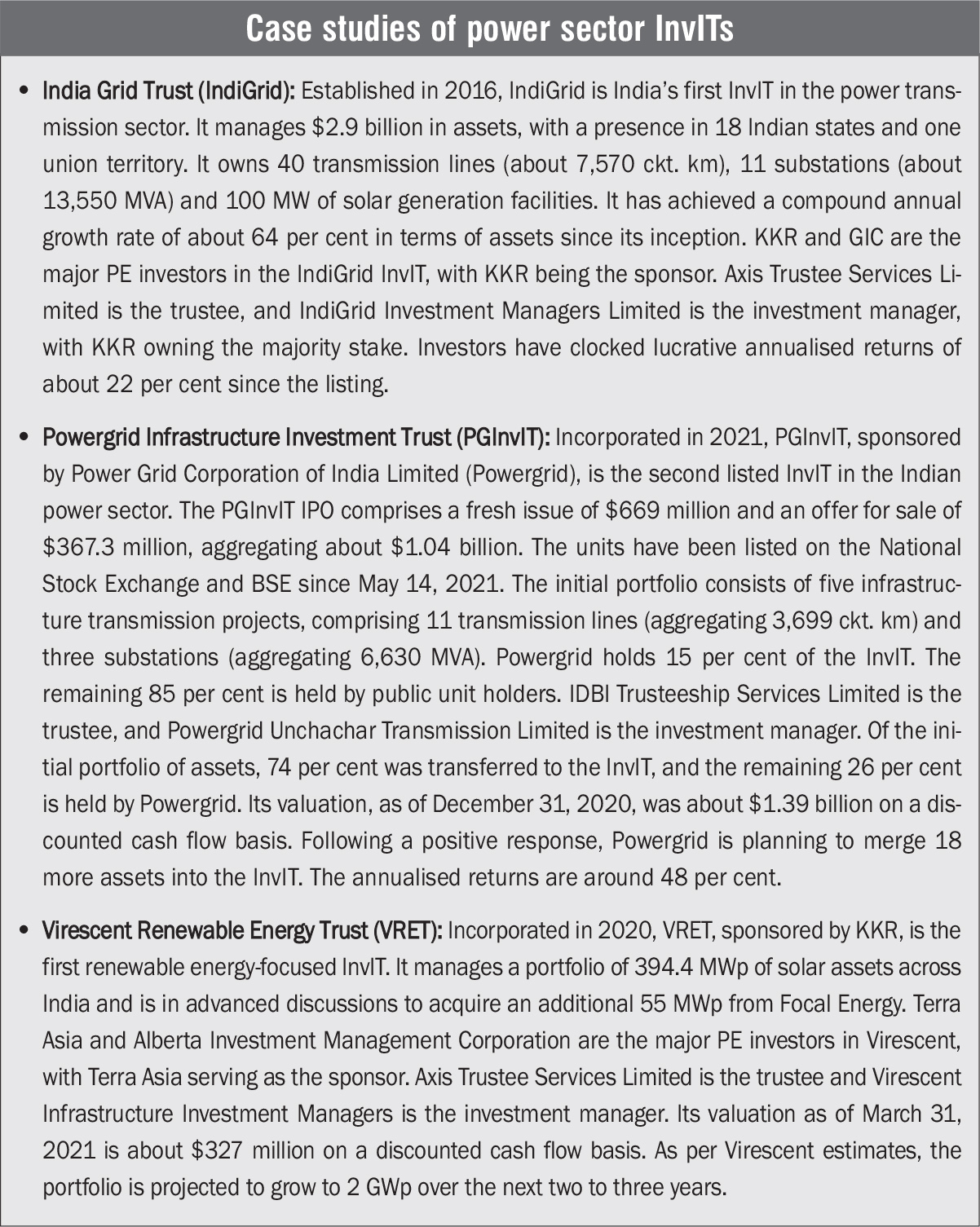

Despite their many advantages and vast potential, InvITs have not taken off in the Indian renewable energy sector. Virescent is the only renewable energy InvIT, and IndiGrid holds only a small renewable energy asset as part of its portfolio. To date, the proportion of renewable energy in InvIT investments is a minuscule 1 per cent.

Despite their many advantages and vast potential, InvITs have not taken off in the Indian renewable energy sector. Virescent is the only renewable energy InvIT, and IndiGrid holds only a small renewable energy asset as part of its portfolio. To date, the proportion of renewable energy in InvIT investments is a minuscule 1 per cent.

For a renewable energy InvIT to succeed in the Indian market, it needs to be AAA rated. Assured yields are imperative to attract sufficient investor interest. The renewable energy projects chosen for InvITs should have strong counterparties such as SECI or discoms that are financially viable, as well as a proven track record of timely payments to private developers. Further, at least 80 per cent of the projects under renewable energy InvITs must be operational; however, there is currently a limited amount of such projects in renewable energy, although a large number of operational renewable energy assets will become available over the next 12-18 months. The revenues from operational renewable energy projects are fairly constant, so continuous acquisition of assets is the only way to enhance investor yields over longer time frames. Future cash flow growth will help to ensure the smooth entry and exit of InvIT investors. Further, the choice between public listed, private listed or private unlisted InvITs should depend on capital requirements, cost of capital, leverage ratios, etc.

Net, net, improving the deployment of renewable energy in South Asia will require alternative funding sources, especially at a time when public finances are stretched in many South Asian countries. The experiences and lessons from InvITs in the Indian market could help the South Asian region act as a magnet for institutional investors.

(Based on the handbook, “An InvIT(e) to Renewables Growth in India”, developed by USAID’s South Asia Regional Energy Partnership in collaboration with India’s Ministry of New and Renewable Energy)