The iron and steel sector is critical for the economic growth of the country. However, it is an energy- and resource-intensive sector. The use of conventional production methods in the steel industry tends to harm the environment. According to the International Energy Agency, the iron and steel sector is already the largest industrial sector in terms of energy consumption and contributes around 7 per cent to global direct CO2 emissions.

According to research undertaken by TERI, even with expected energy efficiency improvements in the iron and steel sector, direct CO2 emissions will increase from around 252 mt in 2019 to 837 mt in 2050. In this regard, there is a consensus that incremental measures will not be enough to improve energy and carbon efficiency in the iron and steel sector. Therefore, new clean technologies need to be introduced in the sector. One such technology option is to use low or zero carbon hydrogen as a reducing agent in a direct reduction plant. Low or zero carbon power can be used in electric arc furnaces for producing green steel.

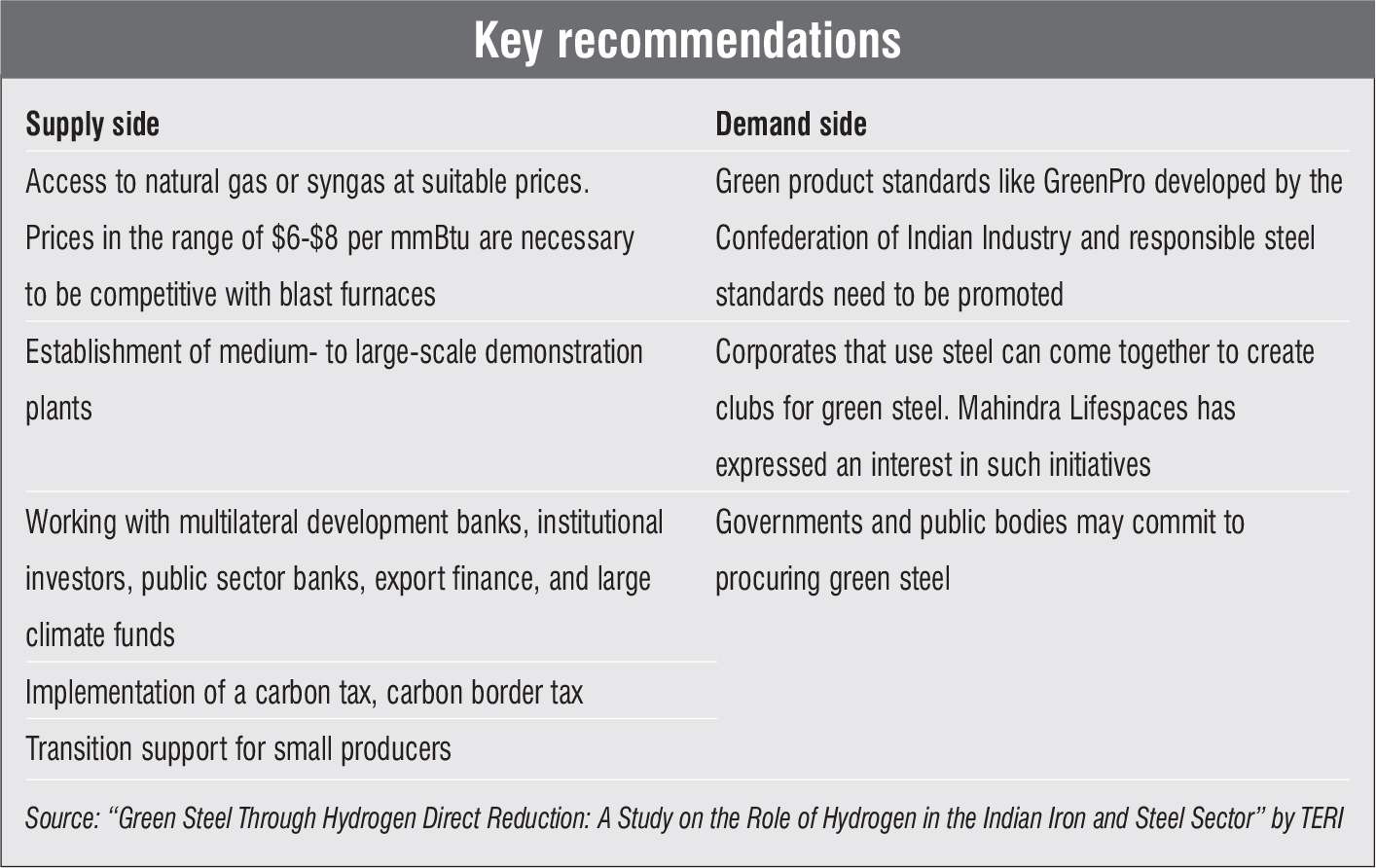

TERI, jointly with Primetals Technologies Austria GmbH and Siemens India, has released a policy brief titled “Green Steel Through Hydrogen Direct Reduction: A Study on the Role of Hydrogen in the Indian Iron and Steel Sector”. The policy brief introduces the direct reduction technology, provides a techno-economic analysis of the technology based on hydrogen, and outlines the potential of green hydrogen technologies. It also gives recommendations to promote this technology.

Edited excerpts from the policy brief…

Direct reduction of iron ore

Currently, over 90 per cent of iron production is through the blast furnace route. The direct reduction technology is slowly gaining uptake. Since 2000, the production of direct reduced iron (DRI) has increased by 250 per cent. Further, the global DRI production increased by 7.3 per cent to 108 mt in 2019. India has the largest DRI production, which stood at 34 mt in 2019. This is one-third of the global DRI production. However, the majority of the Indian DRI is produced through the coal-based route. Across the world, direct reduction based on natural gas dominates given the availability of low-cost natural gas and reduced emissions.

In India, the uptake of gas-based direct reduction technology has been low due to the limited availability of natural gas at competitive prices. At present, there are several gas-based direct reduction units in India. It is an established technology with a production rate of nearly 82 mt in 2019. In this space, there are two dominant shaft-based direct reduction processes. MIDREX® technology accounted for an 80 per cent market share in 2019 while the remaining share was held by Tenova HYL™ technology. The policy brief focuses on MIDREX® technology.

Hydrogen-based direct reduction

A steel plant using MIDREX® technology can be operated using hydrogen in a range of 0-100 per cent, resulting in further CO2 reduction. For this technology, hydrogen can be supplied through an external pipeline or can be produced on site. In addition, the process does not require high purity hydrogen.

In terms of costs, assuming a natural gas price of $10 per mmBtu, using hydrogen is competitive at a price of $1-$2 per kg only. In recent years, natural gas prices in India have fluctuated considerably. While the prices are currently low due to reduced demand, they are expected to align with LNG prices at around $10 per mmBtu.

Besides comparing the steel production cost for the direct reduction/electric arc furnace (DR-EAF) route based on natural gas and hydrogen, it is necessary to compare the steel production costs for the conventional blast furnace/basic oxygen furnace (BF-BOF) route. The latter is adopted for primary steel production in India.

The production costs of a BF-BOF route tend to be slightly lower than for the natural gas-based DR-EAF route, mainly due to the relative price differences of coking coal and natural gas. The range of these production costs reflects the five-yearly natural gas and coking coal prices for India. The brief mentions that DR-EAF can compete with BF-BOF at prices in the range of $6-$8 per mmBtu. The BF-BOF route could still be competitive without further policy measures even with low hydrogen costs. To accelerate transition from fossil fuels towards low-carbon hydrogen policies, a carbon price could be introduced. According to TERI, by 2030, the cost of hydrogen in India could be around $2 per kg. At this price, a carbon price of around $40 per tCO2 would be needed to support the transition from BF-BOF to the DR-EAF route.

Green hydrogen for green steel

The report discusses the production of green hydrogen through PEM electrolysers. The cost of hydrogen from electrolysis can range from $3 to $10 per kg in less favourable conditions. Meanwhile, the cost of grey hydrogen in India is $1.5-$2 per kg. Therefore, the production of green hydrogen from electrolysis will need additional policy support to compete with grey hydrogen.

The cost of green hydrogen from electrolysis will reduce significantly with the decrease in the cost of electrolysers and renewables. In the long run, it is expected that the cost of green hydrogen will be around $1 per kg under favourable conditions, and in the range of $2-$3 per kg under less favourable conditions. At these costs, green hydrogen will start to compete with grey hydrogen.

In sum, the report highlights that electrolyser technologies like PEM provide a viable option for producing green hydrogen for direct reduction at the scale required in the steel sector. It adds that a clear pipeline of projects will be required to allow the scale-up of manufacturing capacity. These will in turn lead to decarbonisation targets of the iron and steel sector going forward.

Market for hydrogen direct reduction in India

The policy brief assumes that gas-based direct reduction plants (primarily using natural gas) are installed during the 2020s. Gas imports will need to increase given the limited domestic gas supplies. Also, a support system will be provided to steel producers given the higher prices. These gas-based plants can switch to hydrogen when low-cost hydrogen will be available. It is assumed that direct reduction plants using high shares of green hydrogen will be constructed from 2030 onwards. Meanwhile, it is expected that the existing blast furnaces will be steadily decommissioned as they reach the end of their economic life. By 2060, a few blast furnaces may remain operational and they will be fitted with carbon capture technology. As coal-based direct reduction plants have a shorter lifetime vis-à-vis blast furnaces, such units will be phased out before 2050. In their place, natural gas- and hydrogen-based direct reduction units will be set up.

Based on this scenario that has been developed in the policy brief, the demand for key fuels in the iron and steel sector will change significantly. At present, the iron and steel sector consumes around 60 mt of coking coal. Of this, over 80 per cent is imported. According to the policy brief, the demand for coking coal will start declining in the 2020s as gas-based capacity is introduced. By 2060, the sector could consume approximately 20 mt of low carbon hydrogen requiring approximately 1,000 TWh of electricity and 250 TWh of electricity for EAFs using DRI and scrap steel. The pace and scale of the expansion of renewable projects will remain a challenge even though there will be significant benefits of reducing coal and natural gas imports.

All in all, the policy brief estimates that the carbon price in the steel sector will need to be approximately $40 per tCO2 in 2030. This would make hydrogen direct reduction competitive with BF-BOF plants (assuming a cost of hydrogen at $2 per kg). A subsequent increase in carbon price would ensure a steady phase-out of natural gas in the direct reduction process, aided by the falling cost of green hydrogen. n