Introduced in 2017, competitive bidding for wind power projects has yielded several positives. The bidding mechanism has created a more transparent and competitive industry, as tariffs are determined based on developers’ analysis of location, counterparty risks, wind conditions and other project-specific factors as well as a company’s ability to do financial engineering. Project sizes have become much larger, thereby providing better economies of scale.

As a result, wind tariffs are at an all-time low, making wind energy a preferred source of power for discoms, which were earlier reluctant to purchase this power due to its higher price. These tariffs may propel non-wind-generating states to procure wind power from “windy” states by installing transmission lines, which will overall, increase the offtake from wind projects. On the industry side, maturing competition has propelled greater consolidation as serious players are seeking larger portfolios while smaller and non-serious players are looking to exit this space.

These gains are, however, accompanied by multiple challenges. One, there is a lack of clarity on the frequency of reverse auctions. Two, it has brought the margins of both developers and original equipment manufacturers (OEMs) under tremendous pressure. Three, transmission of wind power has become constrained as the new projects are largely concentrated in Gujarat and Tamil Nadu. Then, there are the older issues that are unlikely to be resolved by switching to competitive bidding. There is a lack of quality standards and a lack of policy clarity in some high-wind potential states. There is also the need for a policy on interstate power transmission that prevents developers from building capacity for open access power sales.

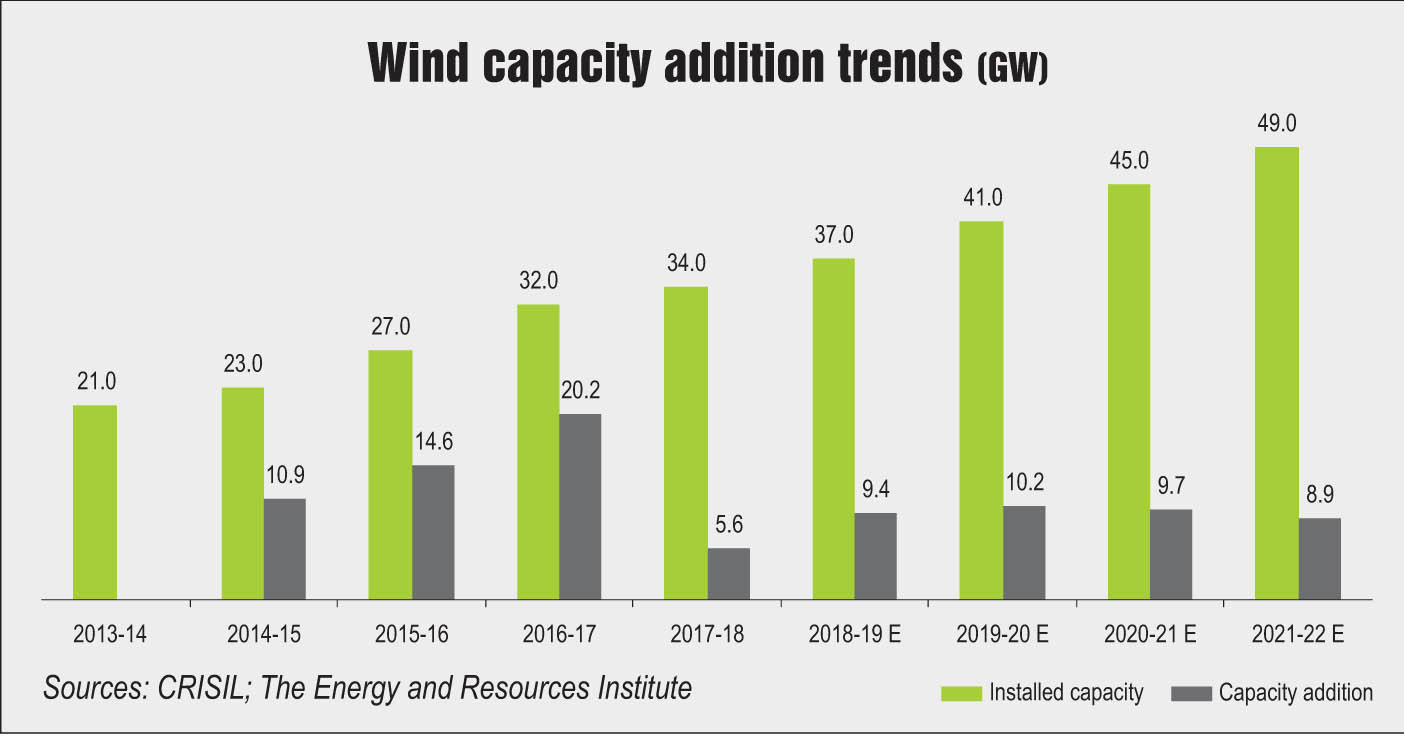

In terms of capacity addition, the impact of the transition to competitive bidding is yet to be seen. Against a potential to add 8,000 MW to 10,000 MW annually, India managed to add only about 1,750 MW last year, trailing a target of 4,000 MW set by the government. In 2018-19 too, the industry may be able to touch only 2-2.5 GW, increasing the woes of wind turbine manufacturers, which are trying to fill their order books in order to sustain themselves. At this pace, India’s ambitious plans to almost double its wind energy capacity from 34 GW at present to 60 GW by 2022 may be hampered.

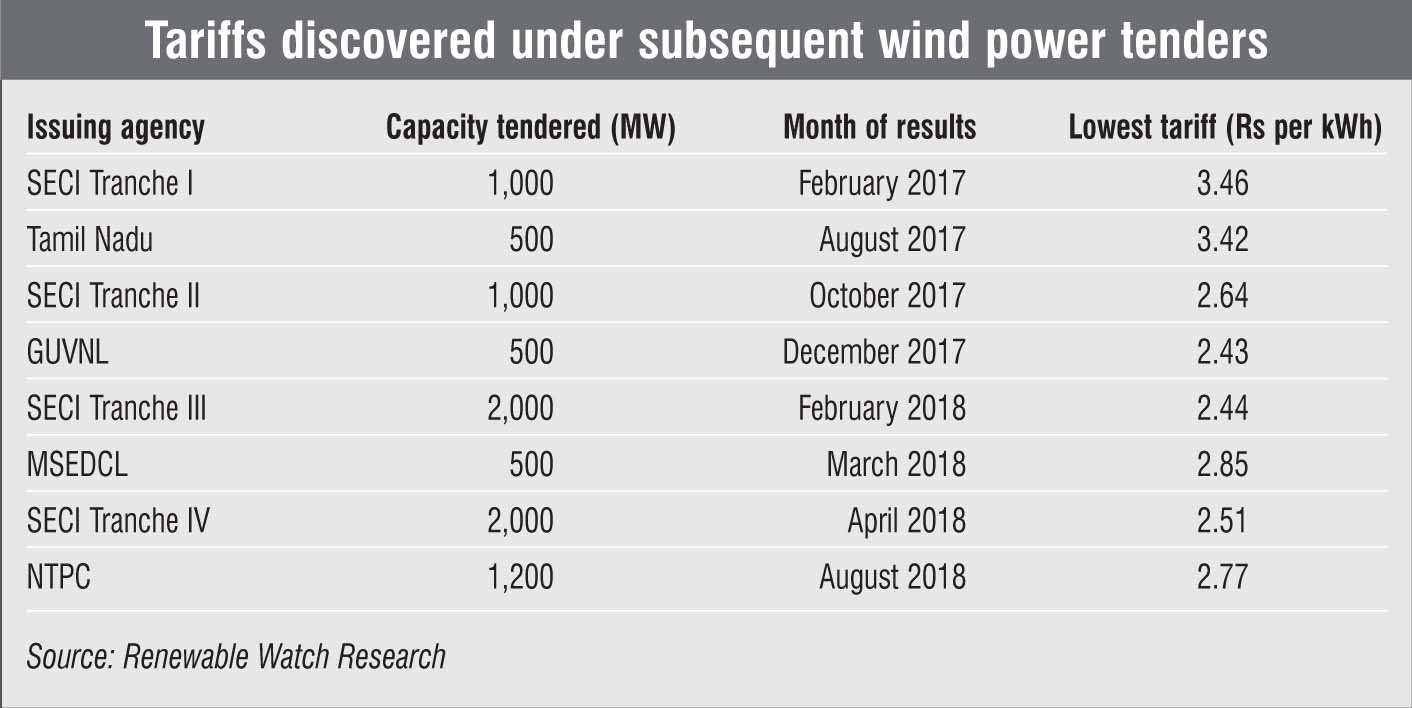

Since the time competitive bidding was first introduced in February 2017, the Solar Energy Corporation of India (SECI), the nodal agency for wind and solar energy auctions, and the state utilities in Tamil Nadu, Maharashtra and Gujarat issued tenders for a total of about 9 GW of wind energy. Another 8-10 GW is proposed to be awarded in 2018-19 and 10 GW in 2019-20. While this is in line with the trajectory of project awards announced by the Ministry of New and Renewable Energy (MNRE) in November 2017 to achieve the cumulative wind capacity target of 60 GW by 2022, the tenders have started facing headwinds.

In July 2018, a 2,000 MW wind power tender issued by SECI had to be cancelled as it failed to muster adequate subscriptions due to transmission-related issues. The SECI Tranche V tender was then re-issued with a lower capacity of 1,200 MW. This time, it has been oversubscribed but the financial bids are yet to take place.

Within a few days of this development, in July 2018, Gujarat Urja Vikas Nigam Limited (GUVNL) annulled its 500 MW wind tender, launched under Phase II of its wind programme. GUVNL had tendered the capacity to cash in on the recent low wind tariffs and to fulfil its renewable purchase obligation (RPO). Wind power tariffs had dropped to Rs 2.43 per kWh in the previous GUVNL wind auction. The scope of work for the GUVNL tender included the development of wind projects along with the requisite transmission infrastructure up to the delivery point. The shortage of transmission could also have played a role in the cancellation of this tender.

Addressing transmission woes

It is now established that the biggest issue facing the wind industry is evacuation of power from sites where developers have decided to install wind farms. The problem magnifies especially in the case of large wind farms requiring connectivity to the interstate transmission system. “The issue came to light when, in the last four SECI auctions, a huge bid capacity (about 2.6 GW) came up for Bhuj in Gujarat due to the high wind sites in the region. However, the evacuation infrastructure was insufficient to cater to such high capacities,” says Shailesh Kumar Mishra, director (power system), SECI.

This issue is now being resolved by the concerned parties and augmentation work of approximately Rs 5 billion at Power Grid Corporation of India Limited’s (Powergrid) substation, including the installation of seven transformers, is being carried out. Powergrid has already issued tenders to develop 10 GW of transmission capacity – 5 GW each in Gujarat and Tamil Nadu. However, there is a catch in this as well. Both these projects will be able to support only around 5 GW of capacity, which is expected to be commissioned in a phased manner between October 2018 and April 2020. What will happen post this? Moreover, Powergrid would take 24-36 months to expand the existing transmission infrastructure for carrying additional wind power. Project developers, on the other hand, have a deadline of 18 months.

Mishra acknowledges these issues and says that the future methodology has been worked out bearing this issue in mind. A plan for 67 GW of transmission capacity augmentation has been developed, which is under approval.

Another transmission-related challenge pertains to unmatched transmission and bid capacities. The Central Electricity Regulatory Commission (CERC) has released a draft regulation, which permits the booking of transmission capacity by the nodal agency, and that is later transferred to the successful bidder identified through competitive bidding. In this particular case, the transfer of connectivity has also been allowed. Once the final guidelines are released, the respective nodal agency can ask for bids for the blocked connectivity, and bidders will only quote in the area where a transmission system is planned. This will ensure planned wind or solar capacity development as the areas have been chosen by the developers themselves.

Impact on IPPs

Backing SECI and the state discoms’ move to encourage new wind projects, wind power generators is keen that certain regulatory modifications and policy changes are put into place to accelerate growth.

One of the issues that wind power developers want resolved relates to the honouring of power purchase agreements (PPAs) as any violation has an adverse impact on developers, investors and financial institutions. There have been attempts in the past by discoms to renegotiate PPAs, but their proposals have so far been rejected by the courts. Another issue pertains to declining margins. According to India Ratings’ estimate, the bidders that won in the first auction would be able to earn an equity internal rate of return (IRR) of just about 9 per cent against IRRs of 18-20 per cent achieved with feed-in tariffs (FiTs). However, the returns rise to 12-14 per cent with a slightly higher plant load factor (PLF), which can be achieved through more efficient equipment, and a reduction in the cost of finance. “While the bidding mechanism is likely to lead to pressures on the revenue side, one would expect these to be balanced by the cost benefits accruing from technological improvements, increasing PLFs, execution efficiencies and enforceable payment security mechanisms,” says Vikram Kailas, managing director and chief executive officer (CEO), Mytrah Energy.

Still, industry experts have cautioned that aggressive developers, in a bid to tap greater capacities, may get trapped in a heavy debt cycle, leading to a situation of non-performing assets (NPAs), as in the case of the thermal sector. According to Ateesh Samant, CEO, IL&FS, “Some manufacturers have in the recent past been giving quotes based on the marginal pricing method. Sustainability at such low quotes remains a challenge for both the manufacturer and the developer.”

Notably, the winners under all auctions so far have been large entities, mostly backed by international financiers and global strategic players in the power space. The auctions could have enabling provisions to allow small investors to participate in the bidding process as this would facilitate investments from domestic investors with long-term commitments. Currently, the small companies’ difficulty in raising cash is keeping them away from government-led power project auctions, restricting their growth and crippling their ability to refinance loans.

One of the impacts of these auctions, therefore, is a greater level of consolidation in the segment. The surge in merger and acquisition (M&A) activity can be attributed to the entry of a large number of global participants with deeper pockets, big appetites and the bandwidth to withstand profit margin pressures. In a rapidly growing and changing wind energy market, the quantum of returns takes priority over the quality of returns. Therefore, companies are looking to expand their project portfolios instead of relying on returns from a few operational projects. In fact, a low-profit environment, in which smaller players are unable to reap optimal returns, is seen as an opportunity by the bigger players to achieve rapid inorganic growth.

Meanwhile, project execution will only become tougher. The size of wind turbines is increasing. This will put pressure on transportation and erection infrastructure. Moreover, right-of-way issues are becoming complex. The capability to execute projects has increased, but broader infrastructure development will remain a major hindrance in large project development.

OEMs face the brunt

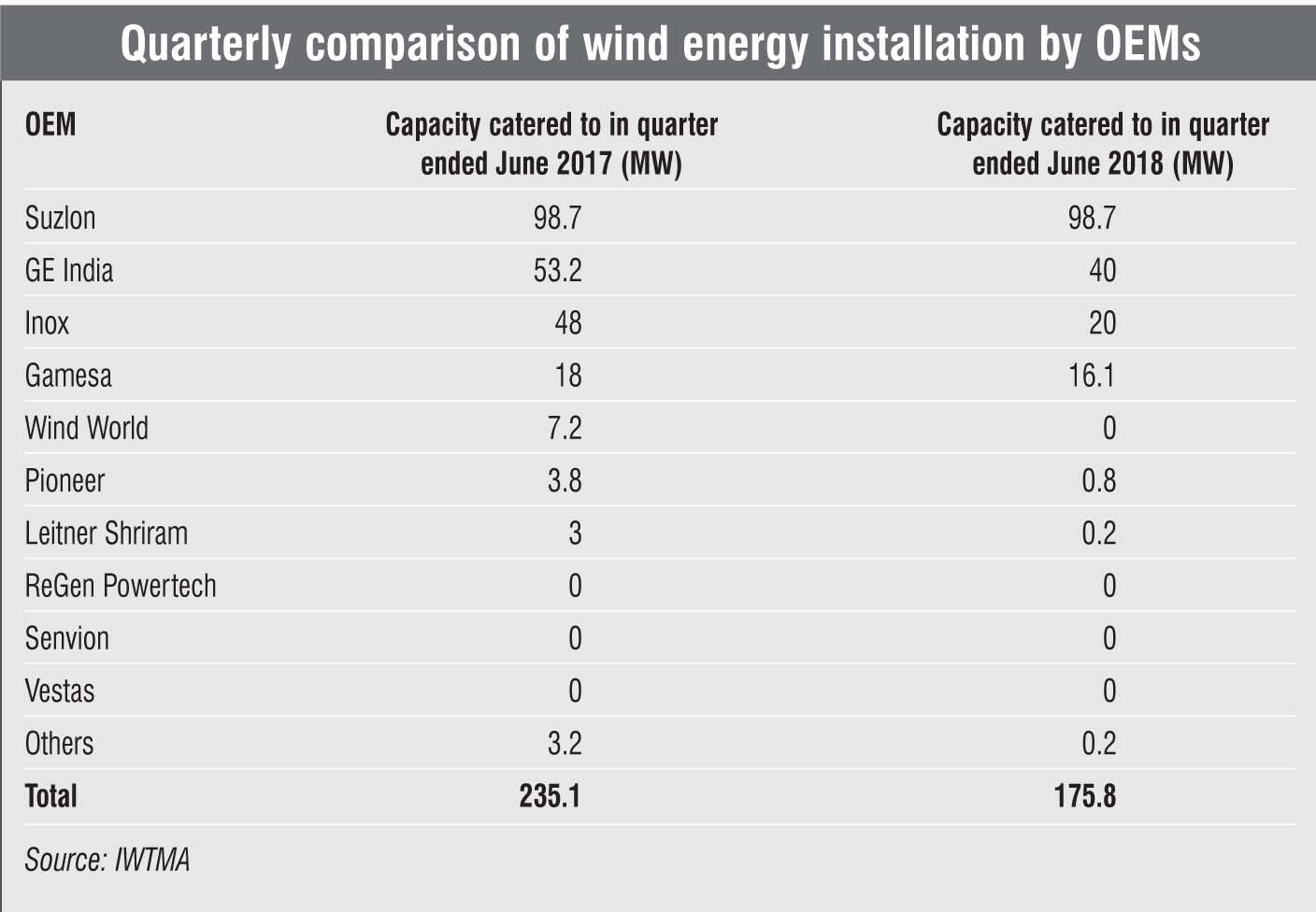

Capacity addition peaked in 2016-17 under the FiT rules, where developers signed individual PPAs with buyers. In 2016-17, 5.5 GW of new capacity was installed, ensuring a healthy balance sheet for OEMs. Tariffs, however, crashed after the government put in place a competitive bidding structure for fresh capacity. This squeezed margins and also led to the cancellation of large turbine orders.

Suzlon Energy, one of the key wind turbine makers globally and in India, plunged from a net profit of Rs 480 million in the quarter ended June 2017 to a loss of Rs 5.75 billion in the quarter ended June 2018. The company withdrew its revenue guidance for 2018-19, citing “near-term market uncertainties”.

In May 2018, Suzlon predicted 45-56 per cent revenue growth for 2017-18 on the basis of its order book and execution capabilities. However, it eventually withdrew the growth guidance, citing approval delays, prolonged execution cycles and bid deferrals. The management further stated that clarity would emerge only by December 2018 as it expects the industry to adjust to the new execution timelines and return to growth in 2019-20.

Inox Wind, another listed domestic equipment-maker, posted a net profit of Rs 103.7 million in the quarter ended June 2018, an improvement over the loss of Rs 390 million it reported in the quarter ended June 2017 but lower than the Rs 118.1 million profit reported in the quarter ended June 2016.

New opportunities

The country saw its first commercial wind-solar hybrid plant getting commissioned in early 2018 by Hero Future Energies in Karnataka’s Raichur district. The greenfield project comprises 28.8 MW of wind turbines and 50 MW of solar modules, and was set up by Siemens Gamesa. Siemens has also developed a 3.375 MW pilot project for NTPC in Kudgi, Karnataka. Such projects lead to a higher return on investment for developers as the plant utilisation factor increases considerably. Further, the intermittent nature of renewable energy has also been addressed to some extent, leading to greater efficiency of transmission infrastructure and better grid stability. According to industry estimates, the capacity utilisation factor of such projects is over 40 per cent. However, regulatory and land management issues continue to pose a threat to the growth of hybrid projects in the country. Currently, there is a lack of clarity regarding metering arrangements, tariff determination and transmission charges for solar and wind components. This is especially the case with brownfield projects. Land prices are higher near existing wind or solar farms, which makes it costlier to hybridise the project. Also, designing a brownfield project is tedious due to the shadow effect of the existing wind turbine on solar panels.

Another emerging area of opportunity in the wind power space in India is the offshore segment. India has a coastline of 7,517 km, which can be harnessed for generating wind power. The full offshore wind potential is yet to be assessed but according to initial studies, Gujarat and Tamil Nadu offer good potential.

Earlier attempts to set up an offshore pilot project in the country have not been successful. However, the scenario is now changing. The National Institute of Wind Energy (NIWE) has proposed extensive studies to assess the offshore wind potential. It has also invited expressions of interest (EoIs) for the development of the country’s first offshore wind energy project in the Gulf of Khambat. As many as 35 national and international developers have expressed interest in the project and the request for proposal is likely to be issued soon. A start has been made but it’s not going to be an easy journey, given the complexities associated with offshore project development. There needs to be a clear demarcation of responsibilities between the central and the state governments with respect to approvals for faster project development. Railway infrastructure, vessels and specialised ports are necessary to transport and assemble wind turbines.

Long-term gains

To conclude, the wind power segment is surely undergoing a transition. Competitive bidding has definitely brought along issues, especially pertaining to transmission and uneven state-wise growth, but it may prove beneficial in the long run. It has brought the power utilities, nodal agencies and developers on a common platform to resolve offtake challenges, and once this issue is sorted, the segment will move to better utilisation of evacuation capacity. It will also address the issue of skewed growth across states. The introduction of solar-wind hybrids and battery storage will further add up to higher utilisation. Low tariffs, meanwhile, will ensure better efficiencies and optimum utilisation of resources by developers. New sub-segments such as solar-wind hybrids and offshore will also create greater opportunities for developers and OEMs. As far as the 60 GW target is concerned, 2022 seems too early to achieve it as there are several short- and medium-term issues that need to be resolved. Till these are addressed, it will not be feasible to achieve the target on time.