The renewable energy certificate (REC) market has failed to take off and the unsold inventory continues to pile up beyond 10 million. While there was a relative improvement in REC purchases in 2016-17, the absolute numbers still indicate a sluggish market. And now, in what could spell the end for the REC market, the Supreme Court has imposed a stay on the trading of solar RECs in a dispute pending with the Appellate Tribunal for Electricity (APTEL), between the Central Electricity Regulatory Commission (CERC) and REC generators.

There are several reasons for the flat growth in the REC market. Among these are the unenforced renewable purchase obligations (RPOs), the fact that the country has become power surplus and that renewable energy is readily available, contributing to the growing glut. Increasingly, rooftop solar power and captive renewable power plants are becoming preferred ways to offset carbon emissions by commercial and industrial consumers, further eroding the market for RECs. Meanwhile, the continuing poor health of the discoms is preventing them from investing in the purchase of RECs.

Market dynamics

The low demand-high supply REC scenario continued in 2016-17 as well with a dismal offtake of RECs. In 2016-17, solar buy bids on the Indian Energy Exchange (IEX) accounted for a mere 1.3 per cent, or 404,081 RECs, of the total sale bids of 32.2 million, while non-solar buy bids comprised 4.3 per cent of the 98.1 million sale bids. The trend on Power Exchange India Limited (PXIL) was as disappointing. The percentage of buy bids against sell bids for solar RECs fell from 1.9 per cent in 2015-16 to 1 per cent in 2016-17, while that of non-solar RECs remained constant at 2.9 per cent. In absolute terms, PXIL recorded 152,933 buy bids against 14.7 million sale bids for solar RECs, and 1.7 million buy bids against 59.6 million sale bids for non-solar RECs in 2016-17. The uptake of solar and non-solar RECs on PXIL was, however, higher in 2016-17 than in 2015-16.

With the Supreme Court imposing a stay on the trading of solar RECs in May 2017 and suspending trading of non-solar RECs for May, June and July 2017, the buy bids on the IEX stood at 738,847 against sale bids of 23.9 million, while those on PXIL stood at 471,036 against 11.9 million for non-solar RECs as of September 2017.

The lack of interest in buying RECs is true for both the exchanges. As of October 2017, 1,095 projects with an aggregate capacity of 4.47 GW were registered with the REC Registry of India. This translates into 7 per cent of the country’s total installed renewable energy capacity, down from 10 per cent in 2016-17 and 12.6 per cent in 2015-16.

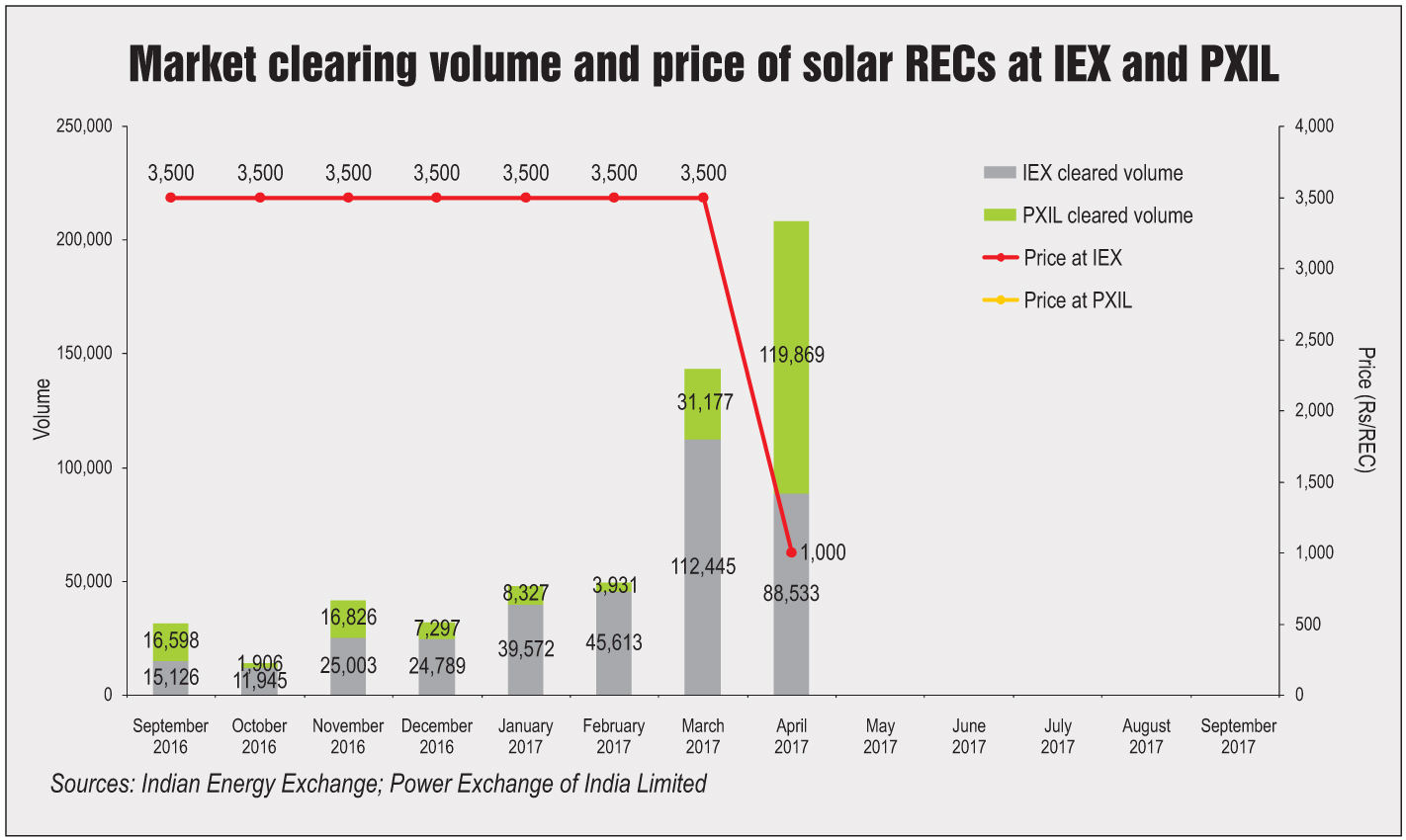

A deep analysis of monthly trading trends reveals a marked shift in pattern. In the non-solar REC category, the peak clearing volume for 2016-17 was recorded in January 2017, while in 2015-16, peak sales were observed in December 2015 and March 2016. In the solar category, the highest sale of RECs was observed in April 2017. This can be attributed to the fact that the CERC had introduced a new pricing regime in March 2017, following which buyers began purchasing heavily at the low prices. Other macroeconomic developments in the country during 2016-17 also affected the general offtake of RECs.

Category-wise analysis

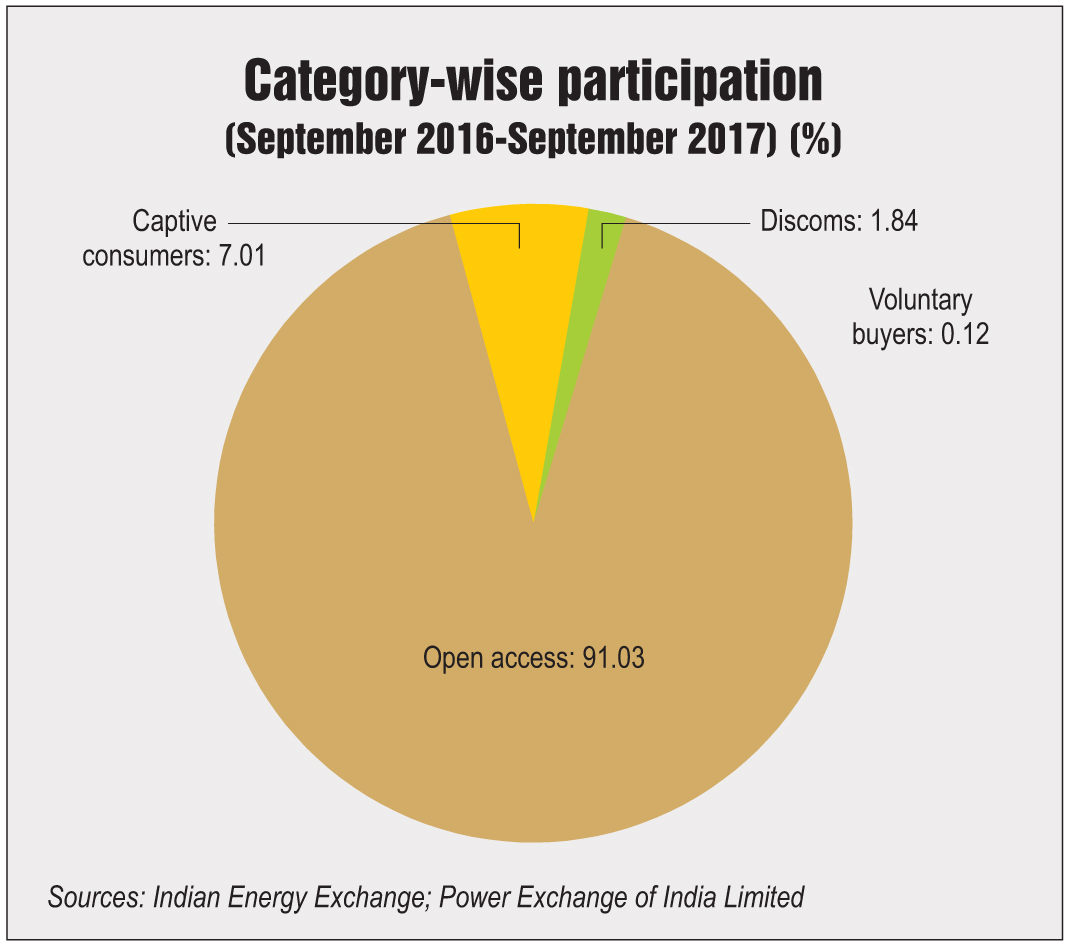

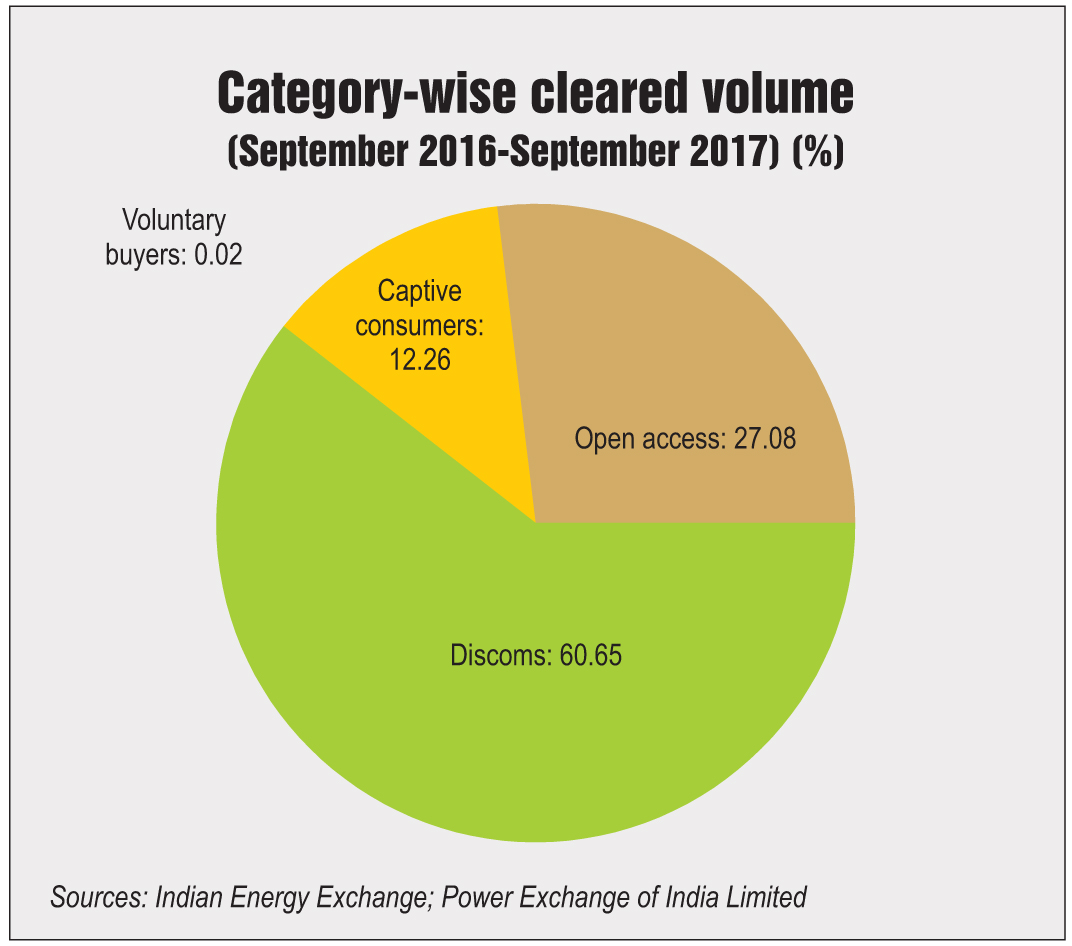

Three out of the four offtaker categories of RECs have continued to follow the dynamic pattern of previous years. The biggest change can be observed in the share pattern of discoms. Their participation in clearing volumes increased to about 61 per cent during September 2016-September 2017 from 39 per cent during the same period of the previous year. The share of open access consumers shrank to 27 per cent from 38 per cent, while that of captive consumers declined from 27 per cent to just over 12 per cent. The share of voluntary buyers remained virtually non-existent.

An analysis of the number of participants reveals a rather skewed share pattern. Open access consumers (3,818) accounting for 91 per cent of the total consumers across the two exchanges, bought 27 per cent of the RECs. Moreover, only 77 discoms, accounting for around 1.8 per cent of the total participants, bought 61 per cent of the RECs. About 7 per cent or 294 captive consumers are responsible for only about 12 per cent of the total volume. This is a strong indicator of a highly consolidated market in favour of discoms, which, despite being small in number, accounted for a far larger quantity of RECs than any other category.

Pricing dispute

Pricing dispute

In March 2017, the CERC decided to introduce a new pricing regime that saw forbearance prices fall from Rs 3,500 per REC to Rs 2,500 per REC, and floor prices drop from Rs 1,500 per REC to Rs 1,000 per REC as per an order released in March 2017.

REC generators, companies that have registered their projects with the REC Registry, objected to the sudden fall in prices that led to severe losses. The matter was referred to APTEL to find a way to clear the unsold stock of around 10 million RECs. APTEL suggested providing a vintage multiplier that allowed a generator to sell more RECs per unit of power. When the parties were unable to reach a consensus on APTEL’s suggestions, the case was referred to the Supreme Court. The court imposed a stay on the entire REC mechanism in May 2017, halting trading and staying the implementation of the CERC’s new pricing regime. While the trading of solar RECs remains suspended, the trading of non-solar RECs was allowed by the court in July 2017, following an appeal by the Indian Wind Power Association. A final decision on the matter is to be taken by APTEL. However, the court ordered that the difference between the old and the new prices is to be deposited in escrow with the regulator while the matter is pending.

Key issues

Key issues

One of the primary reasons for the dismal REC market is the lack of RPO enforcement. Moreover, the poor financial health of discoms has heavily affected their ability to purchase RECs to fulfil their RPOs. Further, for open access, captive and voluntary buyers there are absolutely no incentives to meet their specified obligations. The lack of RPO compliance prevents them from investing in RECs. In fact, in states/union territories such as West Bengal, Uttar Pradesh, Kerala, Arunachal Pradesh, Odisha, Haryana, Assam, Chandigarh and Bihar, the compliance level is less than 60 per cent of the obligation. Another key reason is the falling capital costs and tariffs of renewable energy generation, which has increasingly allowed users and discoms to fulfil their RPOs by investing in more profitable renewable energy projects.

Outlook

Outlook

With the CERC versus generators case still pending with APTEL and the Supreme Court, the trading of solar RECs remains suspended. Meanwhile, the trading of non-solar RECs is slowly limping back to normalcy at the behest of the wind power industry post a three-month suspension. The new pricing regime has also been stayed by the court and it is, therefore, expected that the low pricing methodology will be either scrapped or revised in favour of the generators.

Overall, the future of the REC market appears bleak. With an already fragile ecosystem, the court case could spell the beginning of the end of the REC market.