Given India’s renewable energy targets and Intended Nationally Determined Contributions, the country’s green investments could reach $2.5 trillion by 2030. Traditionally, capital for energy projects has been raised either through equity financing (via private equity) and initial public offerings (IPOs), or debt generated through external or domestic commercial borrowings. Conventional financing is increasingly giving way to new models that factor in the risks associated specifically with renewable energy projects via equity participation, credit guarantee schemes and InVITs (infrastructure investment trusts). To this end, traditional bond and securities instruments have evolved into green bonds, masala bonds and yieldcos. These emerging financing mechanisms are becoming the preferred routes to raise capital for renewable energy projects as they provide debt at low interest rates, diminishing the risk component while ensuring steady returns.

Even though green bonds account for only 1.5 per cent of the global fixed income market, their issuance spiked last year to $93.4 billion, of which Chinese issuers accounted for more than a third of the issuance volume. The global green bond market is expected to more than double in 2017 over the previous year, with India becoming one of the key emerging markets.

Green bonds

Green bonds are debt instruments providing climate-focused investment solutions that aim to reduce the overall cost of capital. These bonds can be particularly useful for institutions and organisations such as the Green Climate Fund, the Green Investment Bank and the Indian Renewable Energy Development Agency that invest in clean energy options. Green bonds have emerged not only as a source of low-interest capital, but also as an instrument to diversify the funder profiles of the issuing entity, which may use the funds raised by these bonds to free their bank credit lines. In addition to funding clean energy projects, green bonds can be used to finance sustainable development goals and green economy projects.

Green bonds usually undergo a third-party certification to ascertain that the proceeds are used for projects that generate environmental benefits. These bonds largely fall under two categories – labelled green bonds (certified for green energy projects) and unlabelled green bonds (uncertified issuances linked to projects that have environmental benefits). In addition, there is another subcategory, called climate bonds, where projects associated with climate change activities are undertaken.

The Climate Bonds Initiative (CBI) has identified four types of green bonds – green use of proceeds bond, green use of proceeds revenue bond, green project bond, and green securitised bond. These are differentiated based on how they are being invested in the projects. For instance, US-based residential solar installer SolarCity Corporation entered the bond market through a green securitised bond backed by the solar lease agreements signed with its customers.

India has become one of the largest green bond markets in the world over the past year, owing to the opening up of a price-sensitive market in need of capital for achieving the ambitious renewable energy target. In the first seven months of 2017, India’s green bond issuance has reached $2.1 billion, enough to fund over 3.5 GW of renewable energy projects. In fact, in the first two weeks of July 2017, Greenko and Azure Power together raised $1.5 billion from the sale of green bonds.

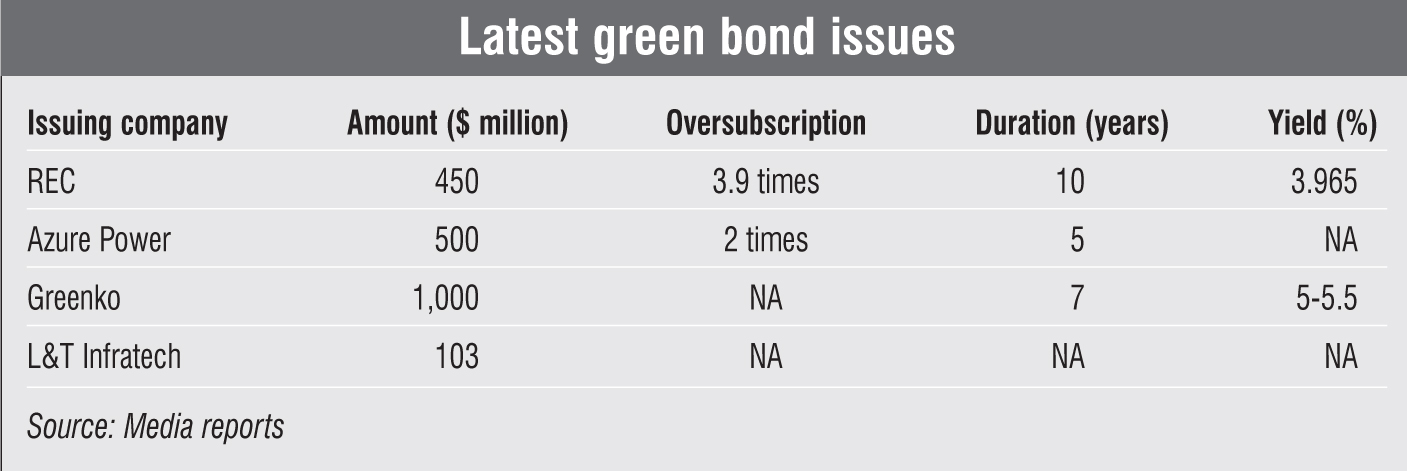

Renewable Watch takes a look at some of the recent bond deals…

REC

The Rural Electrification Corporation (REC) raised $450 million through the sale of green bonds, oversubscribed by 3.9 times, on the London Stock Exchange (LSE). The bond, which is a part of REC’s $1 billion medium-term note programme, is the first of its kind to be traded on LSE’s new international securities market. Investors based in Asia, and Europe, Middle East and Africa (EMEA) made up 68 per cent and 32 per cent of the order book respectively. The bond is expected to mature in 10 years, with an annual yield of 3.97 per cent. The funds raised through the CBI-certified green bonds will be used to finance environment-friendly projects, including solar, wind, biomass, and sustainable water and waste management projects across the country.

Azure Power

Azure Power plans to issue the first-ever solar green bond with a value of $500 million. This is a CBI-certified green bond, set to mature in 2022. Even though the company recently completed its IPO on the New York Stock Exchange, the bond is not registered under the United States Securities Act and will not be offered or sold within the US. The proceeds from the bond will be used for refinancing existing debt and other general corporate expenses of the company. According to a report by the Mercom Capital Group, the bond was oversubscribed by two times.

Greenko

In one of the largest offerings in Asia till date, Greenko Energy Holdings has raised $1 billion through the issue of green bonds. The bond will mature after seven years. It is expected that the capital thus raised will be used to refinance the company’s first dollar bond sale that had fetched $500 million in 2014. Moreover, the company is planning to use the proceeds to refinance the debt it inherited with the acquisition of SunEdison’s 350 MW portfolio last year. According to BRIDGE TO INDIA, the issue has been completed at rates between 5 per cent and 5.5 per cent, resulting in an overall cost of over 9 per cent, including hedging costs.

L&T Infratech

The International Finance Corporation, part of the World Bank Group, has invested Rs 6.6 billion ($103 million) in the first official green bond issue in India by the L&T Infrastructure Finance Company. The company plans to fund solar power projects using the proceeds from the bond. The bonds were issued after the Securities and Exchange Board of India released norms governing green bonds in the country.

Key challenges

With the conventional renewable energy financing mechanisms moving towards new and untested tools such as green bonds, market experts caution against the risks associated with clean energy projects.

Ambiguity surrounding the definition of green bonds is a major challenge as it prevents investors from knowing exactly where their money is being invested. This phenomenon is commonly known as “green washing”. Under this, a project developer may use the funds in clean coal or nuclear power projects. For example, the EDF Group, a nuclear power plant operator in France and the UK, recently issued a Euro 1.4 billion green bond. Although these projects technically reduce carbon emissions, they are not 100 per cent green and, therefore, may not be in line with the expectation of the investor.

Transparency and monitoring remain significant causes of concern in the green bond market. The market still relies on voluntary reporting, which often leads to selective information revelation, preventing an investor from making a well-informed investment decision. However, as the market grows, clear guidelines and processes for monitoring the green bond money trail are expected to emerge.

Another challenge plaguing the green bond market is the lack of liquidity. As the market is small, getting in and out of positions may not be easy for investors as the returns are directly linked with maturity. Therefore, only investors with deep pockets and the patience to wait for bond maturity are likely to invest in green bonds, which reduces the number of players considerably.

Meanwhile, high transaction costs incurred during buying or selling green bonds can diminish returns from projects. Other risks associated with the green bond market include low yields, mispricing of bonds and insufficient information available to make an informed investment decision.

Outlook

“Going green” is currently one of the most popular trends in the economy and is expected to continue in the future, especially in India. With the country promoting innovative financing mechanisms for green energy through favourable regulations, the green bond market is likely to grow. However, the selection of the most appropriate instrument to solve renewable energy financing challenges depends on policy measures and their implementation. To enable a conducive financial ecosystem, the government should engage financial institutions and research organisations on a consultative level for selection, development and implementation of these instruments. Additional steps may be taken to improve the social impact of green bonds. For example, stakeholders could enhance the green bond principles to better address environmental impacts and concerns. Moreover, they can introduce reporting on social outcomes according to international standards for better monitoring.

Macro-level risk reduction in the renewable energy space is required to make the market more attractive for green bond issuers. This will help promote the use of debt-based investments for the development of renewable energy projects in India. At the same time, ensuring offtake of the renewable energy generated and penalising the cancellation of power purchase agreements can become important influencing factors for risk reduction, in turn influencing the future of green bonds in India.