By Preeti Wadhwa

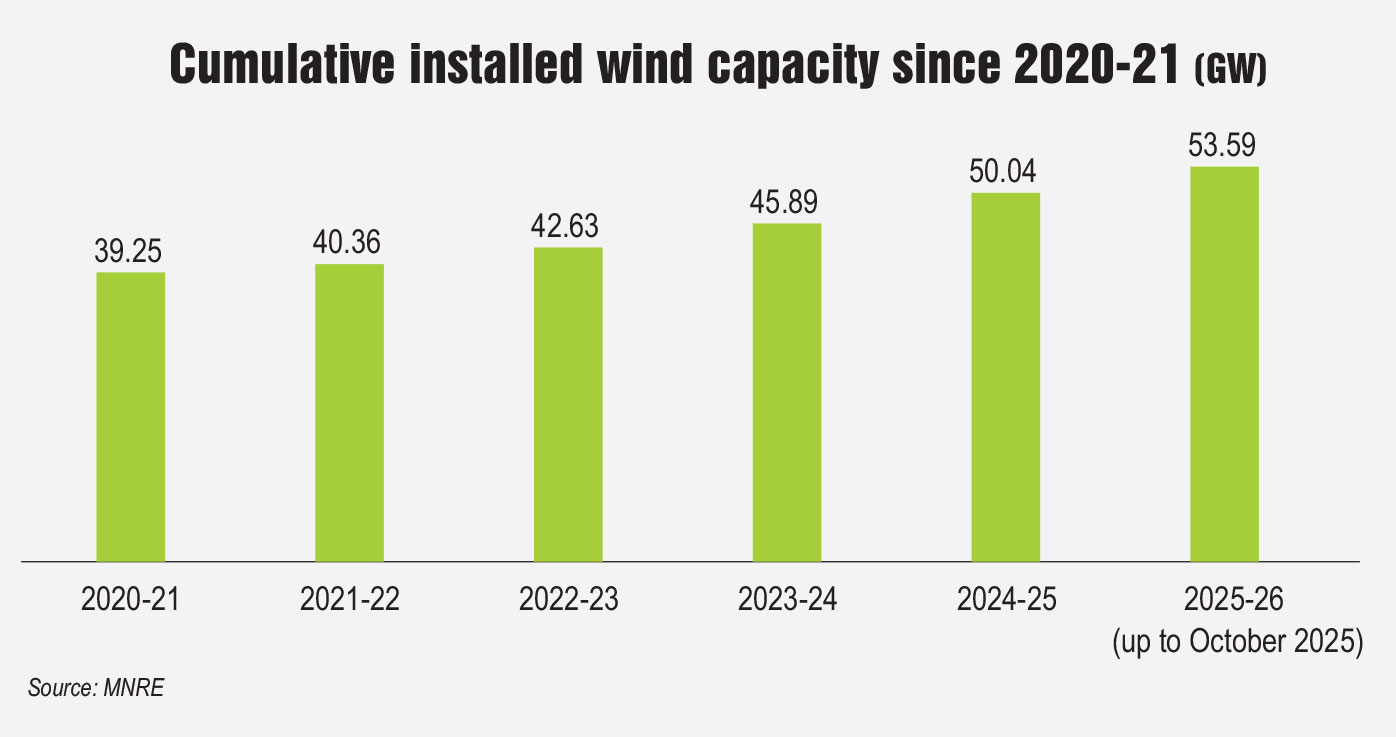

As per the National Institute of Wind Energy estimates, India has immense wind energy potential – about 695.5 GW at 120 metres above the ground level. As of October 31, 2025, the country’s installed wind power capacity stands at 53.59 GW. The wind sector is witnessing renewed momentum, driven by wind-solar hybrids, round-the-clock (RTC) supply, peak power and firm renewable energy tenders. Over the past year, several key developments have taken place in the sector, expected to shape the next phase of growth and determine whether the wind is indeed blowing in the right direction for India’s clean energy transition.

Renewable Watch provides a round-up of the key sector developments in the past year, including tariff and capacity addition trends, sector challenges and the future outlook…

Sector updates

The onshore wind segment has gained significant traction in recent years, driven by a series of policy and regulatory measures aimed at reviving the market. These include the government’s target of 10 GW of annual onshore wind bids from 2023 to 2027, the introduction of tariff-based competitive bidding guidelines to standardise procurement, the notification of sector-specific renewable purchase obligations up to 2030 and the waiver of interstate transmission system (ISTS) charges until June 2025.

In addition, strong tender activity in hybrid, firm and despatchable renewable energy (FDRE) and RTC projects, along with improved transmission planning, changes in tariff determination regimes and strong domestic manufacturing base, have contributed to the growing momentum of India’s wind sector.

The offshore wind segment also witnessed renewed activity in 2024, driven by policy support and fresh tender announcements. The momentum strengthened in June 2025 when the union minister for new and renewable energy announced plans for a new offshore wind tender of up to 4 GW. This was followed by another shot in the arm in July 2025, when the Ministry of Power approved the development of transmission infrastructure for a proposed 500 MW offshore wind project in Gujarat, targeted for commissioning by March 2029.

However, the optimism was short-lived. In August 2025, the Solar Energy Corporation of India (SECI) cancelled two major offshore wind projects, including a 500 MW project in Gujarat and a 4,000 MW seabed lease rights allocation, more than a year after their tenders had been issued. The move, though disappointing, was not entirely unexpected given the limited developer participation and weak market response.

Auction activity

Since November 2024, four wind auctions have been conducted. In January 2025, SJVN Limited announced the results of its auction for 170 MW of ISTS-connected wind projects, part of a larger 600 MW tender issued in March 2024. Adyant Enersol (Datta Infra) won 70 MW at a tariff of Rs 3.98 per kWh, while UPC Renewables secured 100 MW at Rs 3.99 per kWh. The results of the tender, issued in March 2024, were declared nearly 10 months later, and relatively higher tariffs were a key reason SJVN did not award the full 600 MW capacity in this round.

In March 2025, NLC India Limited and Adyant Enersol emerged as key winners in SJVN’s 600 MW wind auction. NLC India secured 200 MW at a tariff of Rs 3.74 per kWh, while Adyant Enersol was awarded 112 MW at Rs 3.81 per kWh. The results reflected a slight downward trend in discovered tariffs compared to earlier bids.

Activity continued in April 2025, with the announcement of Gujarat Urja Vikas Nigam Limited’s (GUVNL) Phase IX wind auction results for 250 MW of grid-connected capacity and an additional greenshoe option of 250 MW. In the auction, KPI Green Energy secured 100 MW at Rs 3.64 per kWh, while Juniper Green Energy and JGRJ Four Renewable (Jakson Green) won 50 MW each at Rs 3.65 kWh and Rs 3.66 per kWh, respectively. Inox Neo Energies (Inox Clean Energy) also secured 50 MW at Rs 3.66 per kWh under the bucket-filling method.

Continuing the momentum, in June 2025, SECI awarded 300 MW of wind capacity to Torrent Green Energy Private Limited under Tranche XVIII. The company received a letter of award for the project at a tariff of Rs 3.97 per unit.

Continuing the momentum, in June 2025, SECI awarded 300 MW of wind capacity to Torrent Green Energy Private Limited under Tranche XVIII. The company received a letter of award for the project at a tariff of Rs 3.97 per unit.

The tariffs discovered across these four auctions held since November 2024 have ranged between Rs 3.64 per kWh and Rs 3.99 per kWh, indicating a period of relative stability and mild downward correction after earlier volatility. The lowest tariff was recorded in GUVNL’s Phase IX auction in April 2025, at Rs 3.64 per kWh, followed closely by bids in the Rs 3.65-Rs 3.66 per kWh range. In comparison, SJVN’s January 2025 auctions saw higher winning bids of Rs 3.98-Rs 3.99 per kWh, while subsequent projects awarded in March 2025 reflected a moderate decline, with tariffs between Rs 3.74 and Rs 3.81 per kWh. The SECI Tranche XVIII auction in June 2025 once again saw bids near Rs 3.97 per kWh. Overall, tariffs continued to hover in the range of Rs 3.8-Rs 4 per kWh.

Capacity addition trends

Wind capacity additions have shown steady improvement in recent years following a period of subdued growth. Between FY 2021 and FY 2025, the country added around 12.3 GW of new wind capacity, with annual installations rising from just 1.5 GW to over 4.1 GW during this period. The trend indicates a consistent revival, supported by improved policy clarity, hybrid project structures and enhanced offtake mechanisms. By the end of FY 2025, India’s total installed wind power capacity stood at 50.04 GW, up from 39.25 GW in FY 2021, representing a compound annual growth rate of about 5.8 per cent over the five-year period. FY 2026 has already seen the addition of 3.56 GW within the first seven months, signalling another strong year for capacity expansion if this pace continues.

The rebound in installations is largely attributed to the roll-out of hybrid, RTC and FDRE tenders, which have restored investor confidence and enabled better grid utilisation. Developers are increasingly leveraging India’s high-quality wind resources in states such as Gujarat, Tamil Nadu, Karnataka and Maharashtra, where infrastructure readiness and transmission access are improving.

Challenges and the way forward

Despite the renewed momentum in the wind energy sector, several structural and operational challenges continue to impede progress and delay the achievement of ambitious capacity targets. The sector is grappling with significant delays in project implementation and widespread cancellations that are undermining overall growth. A critical bottleneck has emerged in the contracting process – as of September 30, 2025, renewable energy implementing agencies had awarded projects totalling 44 GW, yet power sale agreements with end procurers remain unsigned.

The offshore wind segment has experienced particularly turbulent times, with SECI cancelling two major projects in August 2025. The key challenges facing the offshore segment include the lack of robust risk mitigation frameworks, unclear offtake and tariff mechanisms, and financial viability concerns that have deterred meaningful investor and developer interest.

The offshore wind segment has experienced particularly turbulent times, with SECI cancelling two major projects in August 2025. The key challenges facing the offshore segment include the lack of robust risk mitigation frameworks, unclear offtake and tariff mechanisms, and financial viability concerns that have deterred meaningful investor and developer interest.

Additionally, long-standing challenges related to land acquisition, transmission connectivity and state-level policy alignment continue to create obstacles for timely project execution and grid integration, risking a slowdown in capacity additions even as policy support strengthens.

Repowering, long identified as a key opportunity for accelerating wind capacity additions, has also failed to take off despite multiple policy interventions. In 2016, the Ministry of New and Renewable Energy (MNRE) introduced its first policy for repowering ageing wind projects, followed by the National Repowering and Life Extension Policy in 2023, which superseded the earlier framework. The policy estimates India’s repowering potential at around 25 GW, primarily across sites hosting older turbines of up to 2 MW. However, despite this potential and a clearer policy structure, uptake has been slow.

A major challenge is the highly decentralised ownership structure of legacy wind farms, many of which consist of small, individual turbine owners operating sub-optimal machines in high wind corridors. Consolidating these projects under a single repowering plan requires complex coordination, renegotiation of land arrangements and alignment among multiple stakeholders with varying financial capacities and expectations. The absence of a clear, scalable business model has further constrained momentum. Developers face uncertainty around evacuation upgrades, residual power purchase agreement terms and the treatment of existing incentives, while original owners often lack the capital or appetite to reinvest. As a result, repowering remains a largely unrealised opportunity, even though modern turbines could significantly enhance generation on some of the country’s wind sites.

Addressing these challenges will require sustained policy clarity and faster infrastructure development to translate the existing potential into scalable growth. The government’s target of 10 GW of annual onshore wind bids from 2023 to 2027, combined with improved transmission planning and the establishment of large-scale renewable energy parks, provides a strong foundation, but execution must keep pace through close coordination between central and state agencies.

On a positive note, India has emerged as the world’s third-largest wind manufacturing hub, with capacity increasing from 12 GW in 2022 to 20 GW in 2024, a 74 per cent increase that enables the country to cater to nearly 10 per cent of global wind demand. The MNRE’s rebranded Approved List of Models and Manufacturers (Wind) framework, which mandates local procurement of key components such as towers, blades, gearboxes and generators, will further reinforce domestic innovation and reduce dependence on imported components such as castings and pultrusion carbon fibre. This manufacturing scale-up, combined with the availability of 33 turbine models ranging from 225 kW to 5.2 MW across 14 manufacturers, enhances India’s ability to support accelerated deployment while building self-reliance.

Going forward, achieving 100 GW of wind capacity by 2030 is key to ensuring a cost-efficient, affordable and secure energy mix. Having crossed 50 GW, India must double its installed capacity over the next five years, requiring annual additions of approximately 10 GW. Whether this target will be met remains uncertain, since between FY 2021 and FY 2025, the country added only around 12.3 GW of new wind capacity. According to Crisil Intelligence, 9.5-10.5 GW of stand-alone wind capacity is expected to be commissioned by 2030, along with an additional 14-15 GW within hybrid and mixed resource projects. Even in the best-case scenario, the wind sector is likely to fall short of its 100 GW target.

Net, net, the wind sector is entering a phase of meaningful but measured progress. Momentum is building through hybrids, RTC demand and a strong manufacturing base, yet execution bottlenecks, slow contracting and offshore uncertainties must be resolved for the country to stay on course toward its ambitious 2030 wind capacity target.