By GL Aditya, AGM- Business Development, AMPIN Energy Transition

By GL Aditya, AGM- Business Development, AMPIN Energy Transition

Renewable energy capacity in India is currently being added via 2 routes: One being the utility scale competitive bidding, where in the distribution companies/ or central/state nodal agencies come up with tenders for entering into a power purchase agreement (PPA) with the successfully qualified bidders (renewable energy generators). Secondly, the renewable energy generators under open access framework of respective state/centre, directly get into a PPA with the commercial and industrial (C&I) consumers. The C&I consumers on receiving the renewable power from the renewable energy generators would use such energy to suffice for its obligations under the renewable purchase obligations (RPO) or achieve the voluntary commitments under the internationally recognised net zero standards / science-based target initiatives (SBTi) / RE100.

Currently, the open access (OA) from the renewables segment in India has an installed capacity of approximately 35 GW. Of this, 32 per cent is from Solar OA, 34 per cent from Wind OA and 34 per cent from onsite rooftop solar respectively as per Ministry of Power (MoP).

Types of OA access transactions

The C&I consumers have 2 options to source renewable energy from OA, one being the captive/group mode, where the C&I consumer(s) will be required to put individually/collectively at least 26 per cent of the equity shareholding and consume minimum 51 per cent of the generation in proportion of their equity shareholding to qualify as captive consumer(s).

Secondly, there is an option for third-party mode, where the renewable project will entirely be owned by the renewable energy generators and the consumer only source the renewable energy from the renewable energy generators by entering into a PPA.

In India, the C&I consumers are being charged with higher tariff to account for the subsidies given to the agricultural consumers via cross subsidy surcharge (CSS). The CSS accounts for ~30-40 per cent of the total landed tariff for the C&I consumers. In most of the renewable energy rich states, the CSS had either stayed the same or has increased in the past 5 years. The increase in CSS and additional surcharge have become one of the road blockers for the third-party transactions, thereby making them unviable in most of the states.

While under the captive mode, the captive consumer(s) are eligible for waivers on CSS and additional surcharge under the provisions of Electricity Act 2003, hence, being the preferred option for renewable OA.

Options for green procurement

The corporate consumers have the following options to go for RE 100.

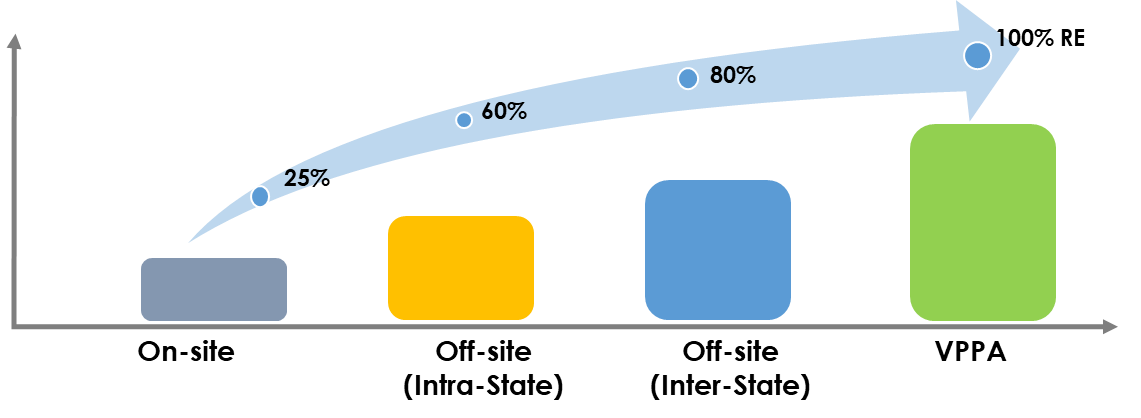

- Onsite: Installing a rooftop in the consumer premises replaces ~25 per cent of energy consumption from the grid.

- Offsite intrastate: Procuring renewable energy via intrastate OA (both renewable energy generators and C&I consumer are in the same state). Replacement from renewable energy to an extent of ~60-70 per cent of the energy consumption from the grid.

- Offsite interstate: Procuring renewable energy via intrastate OA (the renewable energy generators and C&I consumer are in the different states). Replacement from renewable energy to an extent of ~80-85 per cent of the energy consumption from the grid.

- Virtual PPA Model: Procuring green certificates (IREC’s) directly from the project and brown power from the project to be sold on the day ahead market/ real time market of the power exchanges.

Green energy open access and its implementation

MoP published promoting renewable energy through green energy open access (GEOA) rules, 2022 on 6 June 2022. The policy was well received by OA industry which aims to standardise the guidelines thereby creating lucrative opportunities for C&I segment to procure renewable energy and achieve respective environment, social, governance (ESG) targets. Some of the key provisions of GEOA is as follows-

- Consumer having contract demand/sanctioned load ≥ 100 kilowatts (kW), can apply for GEOA. Earlier in the OA regime, the contract demand limitation was set to > 1 MW.

- Allows provision for banking of energy for a period of one month. The permitted quantum of banked energy by the GEOA consumers shall be at least thirty percent of the total monthly consumption of electricity from the distribution licensee by the consumers.

- Additional surcharge shall not be applicable for GEOA consumers, if fixed charges are being paid by such a consumer.

- Consumers will be rated based on the percentage of renewable energy consumed.

- Single window clearances for all approvals related to GEOA. All GEOA applications after getting renewable energy generators registered with central nodal agency will get routed to the respective nodal agencies.

- Concerned nodal agencies

- Short term OA – State Load Dispatch Centre

- Medium term OA- State Transmission Utility

- Long term OA- Central Transmission Utility

- Concerned nodal agencies

MoP rules on GEOA, sets up a guiding framework for the state bodies to act upon and come up with their respective GEOA regulations. As of now, states including Karnataka, Maharashtra, Gujarat, Madhya Pradesh, Haryana, Punjab, Andhra Pradesh, Telangana, Odisha, Chhattisgarh, West Bengal have already come up with their respective GEOA regulations and implementation procedures. While other key states like Rajasthan, Tamil Nadu, Uttar Pradesh have released the draft regulations and have called for stakeholder consultation. The final regulations will soon be released by these states.

Key challenges

While the OA industry will become standardised with the implementation of GEOA regulations, there are a lot of other challenges which shall become a road blocker for OA capacity addition. Some of the key issues are listed below:

- Cumbersome approval processes involving multiple state/central agencies. Such approval processes should be streamlined by adopting to a single window clearance from project conceptualisation to final implementation. Currently the states of Gujarat and Maharashtra have implemented single window clearances for various project stage approvals.

- Non availability of land banks has become a pressing issue for some of new states adopting to GEOA framework. Respective state nodal agencies should act upon the same and create centralised land banks.

- Asymmetry between central regulations and state regulations causing delay in project implementation timelines. State agencies should adapt to frameworks issued by central agencies for better synchronisation.

- Enforcement of Approved list of models and manufacturers (ALMM) to the OA industry is putting an additional burden on renewable energy generators to procure modules at a higher cost. To drive the C&I industry towards voluntary commitments, ALMM should not be made applicable to C&I projects.

Way forward

Despite with several challenges, the C&I consumers interest on procurement of renewable energy had only increased over the past few years. With the addition of renewable energy to the portfolio, the C&I players have not only been able to save significant costs on procurement of energy, but also have been able to fulfil their RPO targets, ESG commitments under net-zero/SBTi/RE 100 initiatives.

Also, the key policy level initiatives from central/state regulatory bodies have created a cohesive environment for C&I players to carry this momentum forward in sustainable energy transition. It is expected that this market will have additional 47 GW of new corporate capacity addition till 2027 and about 120 GW of additional corporate capacity additions by 2030 as per Bridge to India.

Further, on addressing the above challenges, the C&I consumers can not only speed up their own energy transition, but also significantly contribute to achieving the India’s ambitious non-fossil fuel target of 500GW by 2030.