By Sarthak Takyar

By Sarthak Takyar

One of the key trends highlighted in the cover story of Renewable Watch’s January 2024 issue was the rise of round-the-clock (RTC) renewable energy as a key energy source, on par with thermal, hydro and nuclear power, for meeting baseload requirements. It highlighted the country’s ongoing plans for significant capacity additions in non-renewable sources till 2032, including 80,000 MW of coal/lignite-based capacity, 18,033.5 MW of hydro capacity and 8,000 MW of nuclear capacity, alongside the promotion of renewables (78,935 MW under construction). A key reason for simultaneously promoting both renewable and non-renewable energy sources is the former’s inability to provide consistent power. Further, storage technology costs have not decreased as anticipated, resulting in continued reliance on non-renewable sources for meeting baseload requirements. This trend becomes important in light of the ambitious climate targets set by the government – to set up 500 GW of non-fossil fuel capacity and fulfil 50 per cent of the country’s electricity needs from non-fossil fuel sources by 2030.

Success depends not only on achieving these targets, but also on doing so in a manner that does not unduly burden stakeholders in the power sector, including grid operators, distribution companies (discoms), renewable energy developers, conventional power plant operators, commercial and industrial (C&I) consumers and taxpayers. The pressure largely stems from the intermittent nature and variability of standalone renewable energy supply and the high costs associated with storage technologies, which may lead to inefficiencies and increased costs.

Conundrum for grid operators: Must-run status of renewables

Grid operators are responsible for adhering to the must-run status of renewables, a key policy initiative aimed at increasing their uptake. This involves procuring intermittent renewable energy and not curtailing it, except in cases where it jeopardises grid safety (though this exemption is often misused to curtail renewables). Earlier, this issue placed even greater pressure on the grid as the generation cost of standalone renewable energy significantly exceeded that of conventional generation sources. While the cost of standalone renewable energy has decreased vis-à-vis conventional sources, the issue of variability still exists. Therefore, properly forecasting and scheduling power generation is crucial.

Balancing act: Renewable developers navigate strict forecasting and scheduling regulations while catering to growing customer expectations

In addition to grid operators, renewable energy developers must ensure accurate forecasting and scheduling in order to avoid penalties. Failure to do so may result in power curtailment, leading to revenue losses. The lack of storage technologies also increases the risk of curtailment, but integrating them is costly. The failure to transition to RTC projects also impacts developers’ business prospects as C&I customers increasingly demand RTC renewables to meet corporate climate goals and reduce reliance on expensive grid power.

Feeling the pressure: Increasing responsibilities and costs for conventional power plant operators

The growing uptake of variable renewables, which have a must-run status, places pressure on conventional power plant operators to enhance their system flexibility in order to significantly ramp up and down during non-solar peak demand hours. This challenge is often illustrated using the duck curve. The significant ramp up and ramp down leads to high operational costs, especially when thermal power plants (TPPs) are not flexible enough and operate on a much higher technical minimum load requirement vis-à-vis global trends and domestic targets.

Multi-pronged challenges: Discoms struggle to meet peak power demand and stringent RPO targets while taxpayers bear an indirect burden

With only standalone solar and wind projects, discoms struggle to meet the peak power demand, thus relying heavily on thermal power and often purchasing power from the exchanges at high prices, further straining their already stressed finances. This also results in low compliance with renewable purchase obligation (RPO) targets. Failure to meet RPO targets leads to penalties, exacerbating the financial woes of the already struggling discoms.

These penalties on discoms may also impact the common man due to the increase in electricity prices. If state regulators incorporate this expense in the discoms’ annual revenue requirements, the price of electricity will be increased, impacting the taxpayer. If regulators do not consider these expenses, discoms will have to bear the costs. Given that most discoms are state owned, ultimately the government will pay using the taxpayer’s money. While standalone renewables, especially rooftop solar, offer some savings on electricity bills for consumers, taxpayers indirectly bear the burden of increased standalone renewables integration into the grid.

Transitioning to RTC renewables

Transitioning to RTC renewables

Given the various challenges faced by power sector stakeholders due to the increased adoption of standalone renewable energy projects, there has been a shift in focus towards renewable energy and storage hybrids to deliver RTC renewable power.

In the policy space, a key recent development has been the notification of guidelines for the tariff-based competitive bidding process for the procurement of firm and despatchable power from grid-connected renewable energy projects with energy storage systems. Introduced by the Ministry of Power in June 2023, these guidelines aim to enable discoms to procure firm and despatchable renewables, coupled with energy storage, through tariff-based competitive bidding. Another major policy initiative allows discoms and other designated consumers to meet their RPOs not only through the procurement of standalone renewables, but also through a combination of sources, including hybrid or RTC renewables.

Several significant tender developments have taken place at the central and state levels in RTC renewables and hybrid projects. The key work carried out by central agencies is discussed here. In May 2020, the Solar Energy Corporation of India’s (SECI) 400 MW RTC-1 tender discovered the lowest tariff of Rs 2.90 per kWh, with a 3 per cent annual escalation for the first 15 years of the 25-year PPA, resulting in an effective tariff of Rs 3.59 per kWh. The entire capacity was won by ReNew Solar Power Private Limited. As per the bid conditions, the developer was mandated to fulfil an annual and monthly minimum capacity utilisation factor (CUF) requirement of 80 per cent and 70 per cent respectively. Failure to achieve these would result in the removal of tariff escalation in the subsequent years, until the requirement is fulfilled (for shortfall below 77.5 per cent availability) and a penalty of 300 per cent of the PPA tariff for shortfall below 80 per cent availability and up to 77.5 per cent.

The RTC-2 auction was conducted in October 2021 for 2,500 MW (reduced from the original 5,000 MW) of renewable plus thermal capacity, with Hindustan Thermal Projects securing 250 MW of capacity by quoting the L1 tariff of Rs 3.01 per kWh. Under this tender, the tariff structure was part fixed and part variable. The annual CUF requirement was 85 per cent with a peak hour duration of four hours. The penalty provision was 400 per cent of the applicable tariff.

Prior to the RTC-1 and RTC-2 auctions, SECI had issued a 1.2 GW tender for renewable-plus-storage projects with an assured peak power supply. The auction was conducted in January 2020, with Greenko and ReNew Power winning 900 MW and 300 MW at a peak tariff of

Rs 6.12 per kWh and Rs 6.85 kWh respectively and an off-peak tariff of Rs 2.88 per kWh. SECI issued another tender in April 2023 with assured peak power supply (1,200 MW solar-wind hybrid with energy storage, Tranche VI). The tariffs ranged between Rs 4.64 per kWh and Rs 4.73 per kWh in this auction. In April 2023, Railway Energy Management Company Limited (REMCL) issued its tender for the delivery of 1 GW of RTC renewables with or without storage, in which an L1 tariff of Rs 3.99 per kWh was discovered. REMCL also auctioned 750 MW of RTC renewable projects, with or without storage, early this year, in which an L1 tariff of Rs 4.25 per kWh was achieved. Meanwhile, in November 2023, SJVN Limited launched its tender for 1.5 GW of power from interstate transmission system-connected renewable energy with energy storage projects, which had a winning tariff of Rs 4.38 per kWh.

Promising solution, but new problems too

While the policy push to facilitate the transition from standalone renewables to RTC power is commendable, it entails several challenges. The high cost of energy storage implies that its use will be minimal, with a primary focus on renewables and thermal power in RTC tenders. As a result, oversized renewable energy plants are being developed to meet RTC demands. As the plants are set up at multiple locations ensuring transmission connectivity becomes a hurdle. Going forward, supply chain disruptions, duties and taxes on solar components, and an increase in input costs may increase the cost of solar and renewable energy projects. This raises questions about the willingness of discoms to buy RTC power to meet their peak power demand, especially as they are obligated to pay fixed costs for thermal power.

The issue of expensive RTC power persists as the cost of storage technologies has not reduced as anticipated. Developers are investing in pumped storage projects, which seem to be the cheapest storage option in the long term. Green hydrogen is also emerging as a viable storage option to avoid curtailment of excess renewables. In addition, there are concerns regarding the complicated nature of rules and provisions for RTC tenders, making the developers’ tasks tedious and subject to stringent penalties, particularly as they already struggle with accurate forecasting and scheduling.

Next steps and discussion points

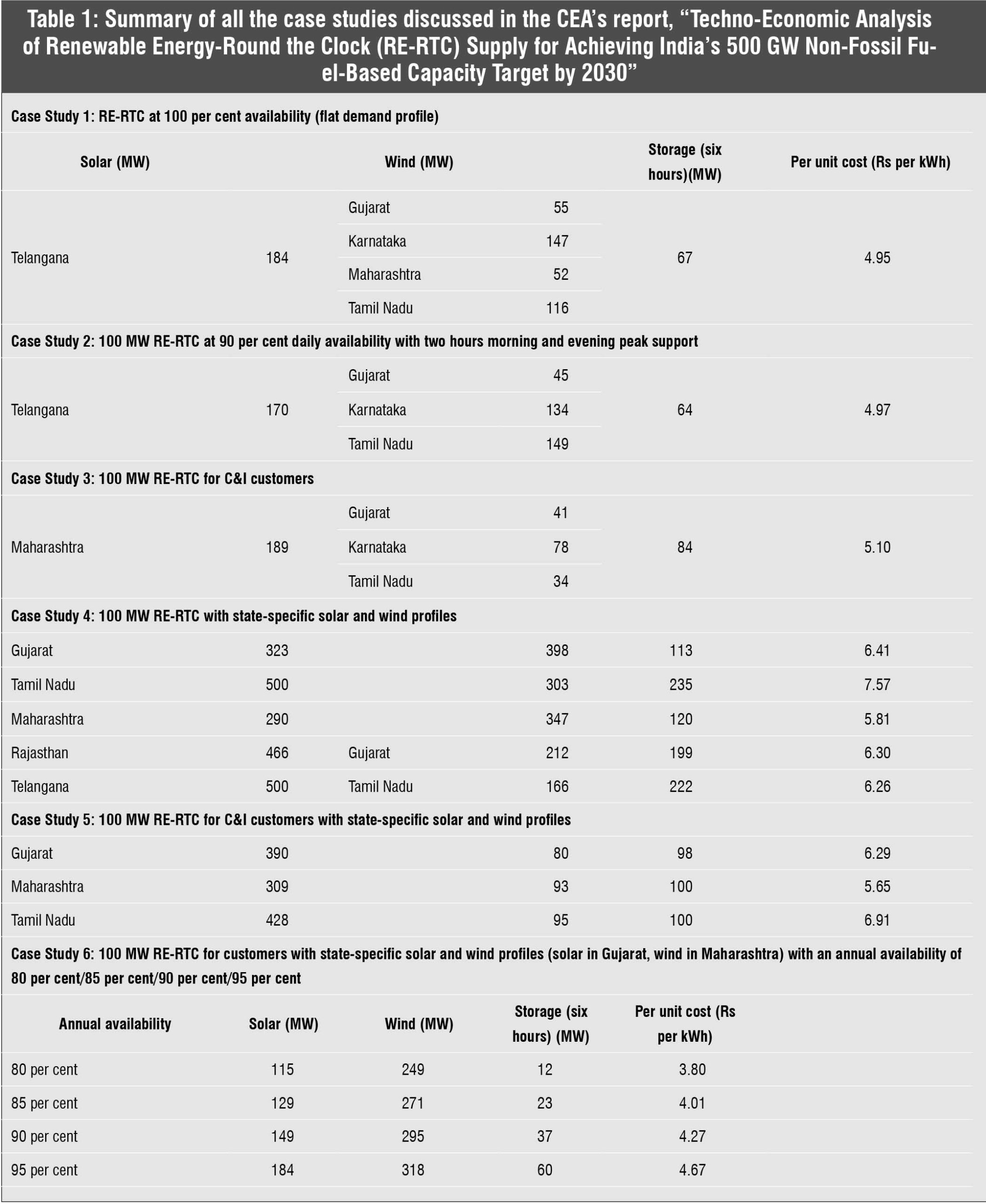

The Central Electricity Authority (CEA) recently released a report titled “Techno-Economic Analysis of Renewable Energy-Round the Clock (RE-RTC) Supply for Achieving India’s 500 GW Non-Fossil Fuel-Based Capacity Target by 2030”. The report assesses various scenarios of renewable energy generation combined with storage capacity across different states to provide RTC power at a certain availability and load profile at optimum costs. The accompanying table provides a summary of all the scenarios.

Going forward, the shift towards RTC renewables has key implications for policymakers, raising several questions. One, if RTC renewables, including storage, are consistently priced lower than RTC conventional power, do stringent RPOs remain relevant? Will they become the default choice for discoms? Moreover, in scenarios where RTC renewables are cheaper than other sources, does the must-run status of renewables need to be re-evaluated? If the uptake of RTC renewables for providing baseload needs proves to be costly and complicated, policymakers may consider promoting nuclear power, an alternative clean baseload option. Another policy implication pertains to banking, as many C&I consumers claim to procure 100 per cent renewables through this route. There is a need to make RTC renewables truly green in order to avoid greenwashing by corporates going forward.

Overall, even though the uptake of RTC renewables seem to be generating more questions than answers, they are clearly here to stay.