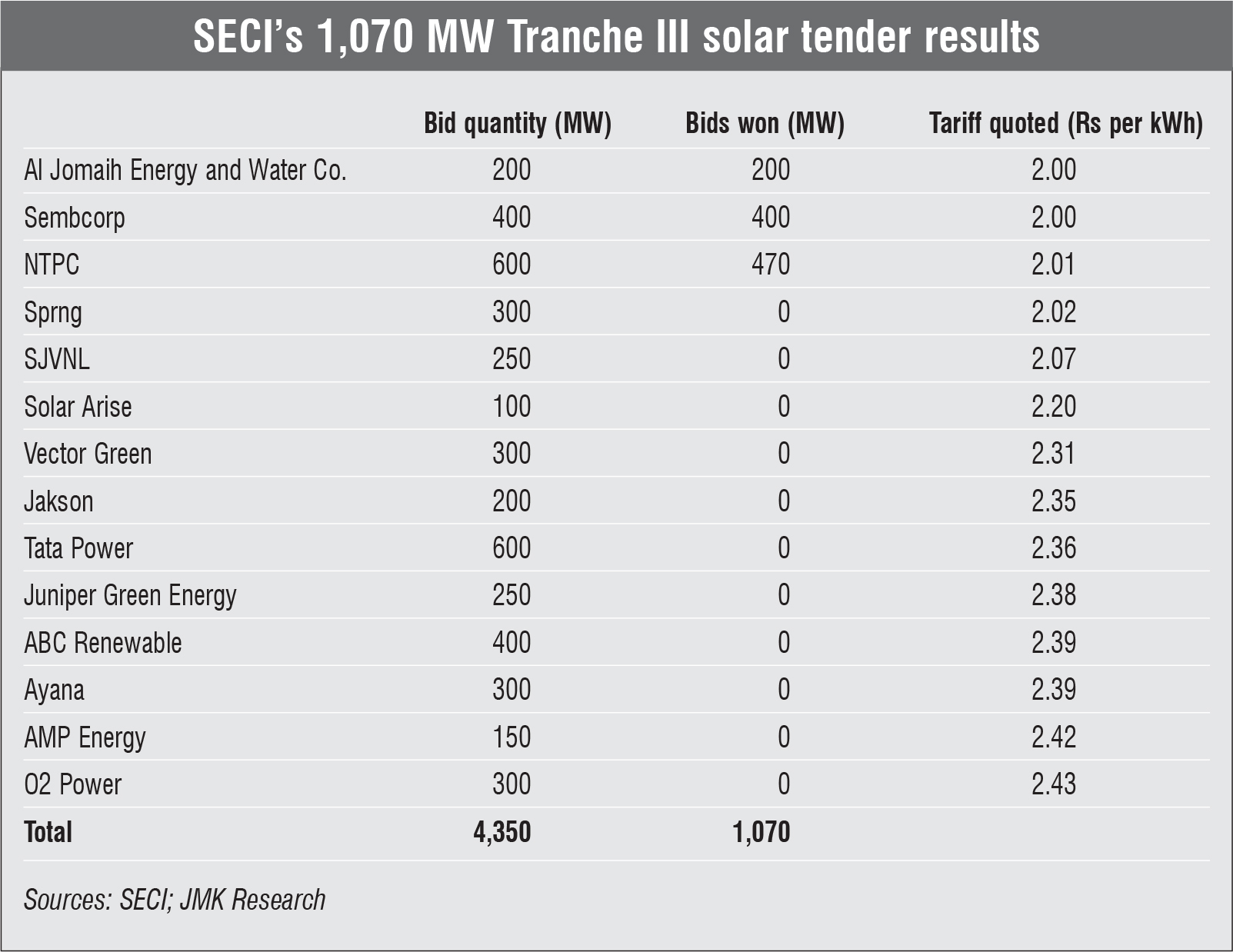

Solar tariffs in India have hit yet another low in the year 2020. In November 2020, a record low tariff of Rs 2 per kWh was discovered in an auction conducted by the Solar Energy Corporation of India (SECI). The auction was conducted for developing 1,070 MW of grid-connected solar power in Rajasthan (Tranche III). The previous lowest winning tariff of Rs 2.36 per kWh was set by SECI’s 2 GW interstate transmission system (ISTS)-connected solar tender, Tranche IX, in July 2020.

SECI’s Tranche III solar tender in Rajasthan received an overwhelming response. There were 14 bidders with the total bids adding up to 4,350 MW. The lowest tariff was quoted by Green Infra Wind Energy Limited (a subsidiary of Sembcorp) and Al Jomaih Energy and Water Company for capacities of 400 MW and 200 MW respectively. The second lowest tariff of Rs 2.01 per kWh was quoted by NTPC limited for 600 MW of capacity, but it was allotted only 470 MW through the bucket filling method. SECI had floated the tender in July 2020 for projects to be set up on a build-own-operate basis. The commissioning timeline for these projects is 18 months from the date of signing of power purchase agreements.

The tariff reached a record low of Rs 2 per kWh due to a combination of reasons. Renewable Watch presents the key factors responsible for the aggressive tariffs, with inputs from the Institute for Energy Economics and Financial Analysis (IEEFA) and JMK Research’s recent study on the subject…

Foreign players and low-cost finance

A large number of international investors with deep pockets and a huge risk appetite have entered the Indian solar space, which has played a critical role in the recent dip in solar tariffs. In the latest auction, Saudi Arabia-based Al Jomaih Energy and Water Company and Singapore-based Sembcorp Energy’s Indian subsidiary, Green Infra Wind Energy, were the lowest bidders. In the previous auction, Spanish company Solarpack Corporacion Tecnologica quoted the L1 tariff of Rs 2.36 per kWh. Other winners included Italy’s Enel Green Power, Germany’s IB Vogt, New York-based Eden Renewables, Canadian developer AMP Energy, Ayana Renewable Power, backed by the UK’s development finance institution CDC Group, and ReNew Power, backed by Goldman Sachs among other investors.

These international developers have been keen to enter the Indian market, and are bidding aggressively for solar projects. They also have access to low-cost financing, which also leads to lower expectation for return on equity, making lower tariffs viable. Al Jomaih, for instance, has now entered the Indian market after winning the bid for a 55 MW solar project in Bangladesh, where the bid tariff went as low as $0.0748 per kWh. Sembcorp also has a presence in the wind and solar power market in India.

For domestic layers, debt financing for green energy projects is slowing down. This is partly because large Indian banks are declining to fund projects that have committed to sell power at less than Rs 3 per unit due to viability concerns. That said, government entities like NTPC can secure debt at the rate of 7-7.5 per cent. Thus, NTPC has been moving fast in terms of green energy portfolio expansion. It has around 4 GW of renewable capacity, mostly solar, and plans to add at least 5 GW of solar capacity in the next two years.

Advantage for Rajasthan

To create a conducive environment for solar power development, the Rajasthan government has taken key steps, such as the announcement of the Rajasthan Solar Policy, 2019. Due to a provision in this policy, developers will be able to save on overhead costs. As per the clause, developers are expected to pay Rs 200,000 per MW every year for the entire life of the project as a contribution towards the Rajasthan Renewable Energy Development Fund. However, this is only payable if the power generated from the solar projects is sold to discoms outside the state. In the case of the latest 1,070 MW project, the power will be sold to the discoms within the state.

Of late, many Indian distribution companies have been struggling financially and have often been unwilling to sign agreements to procure power from intermediary agencies like SECI. This had also led to wariness among developers. However, in the case of the recent SECI project, there is assurance of power purchase for developers as the power sale agreement between SECI and Rajasthan Urja Vikas Nigam Limited has already been signed, thus alleviating concerns regarding power offtake. Other positive factors for setting up solar projects in Rajasthan include the relatively low land rate as compared to other states and very high solar irradiation. Since large-scale solar projects are very land intensive, this is a major advantage.

Project cost and LCOE

Project cost and LCOE

Since Rajasthan has high irradiation, higher efficiency modules can help greatly in the optimum utilisation of this factor. As the project is developed, it is likely to include bifacial modules and single-axis trackers. These are expected to have increased efficiencies, with a capacity utilisation factor that could go as high as 30 per cent. This will reduce the levellised cost of energy (LCoE) of the solar plant. As per the IEEFA’s report, solar insolation in Rajasthan is in the range of 19-21 per cent, depending on the site.

Module prices, which constitute almost 64 per cent of the project cost, are also expected to fall due to the expansion of production capacities. Many module manufacturers around the world, including leading Chinese players, have announced expansion plans in production over the past year. These companies include Risen energy, Trina Sola, ZnShine, Canadian Solar and Longi. Given the push towards domestic manufacturing, companies such as Adani Solar and Vikram Solar have also announced plans to expand their manufacturing. Lately, there have been some uncertainties regarding the extension of safeguard duty and exemption from basic customs duty. Given the 18-month commissioning timeline for this tender, it is likely that modules will only be procured after July 2021. If the safeguard duty is not extended beyond July 2021, it will not be applicable to modules supplied for these projects. If the basic customs duty exemption is levied, a change in law clause will be introduced for these projects.

Conclusion

Conclusion

The recent fall in renewable tariffs, especially solar tariffs, can be attributed to many factors. Most notable among these is the entry of foreign players with an advantage of access to low-cost financing. Further, there are expectations regarding the decline in module prices and absence of safeguard duty and basic customs duty for the 1,070 MW SECI tender.

Even if the tariffs are viable, there are still uncertainties and risks associated with these projects. For one, there is uncertainty regarding the technology that would be used for the solar projects. While

higher efficiency modules with single-axis trackers are the preferred choice, projects lenders in India are reluctant to fund this technology because of the lack of experience in the country. Further, due to the lag in placing bids and module procurement, module prices could differ from expectation. This new tariff could create similar expectations in other states as well. Although highly unlikely, even if developers agree to supply power from new projects at these tariffs, there would surely be concerns regarding viability and substandard project quality.

Overall, it remains to be seen what this latest round of auctions with record low tariffs means for the Indian solar market.

Note: A new record low tariff of Rs 1.99 per kWh was discovered shortly before the magazine went to press. The tariff was discovered in Gujarat Urja Vikas Nigam Limited’s (Phase XI) auction for 500 MW of solar power capacity.

By Meghaa Gangahar