")

The solar space in India has been losing growth momentum in recent times. The capacity addition of utility-scale solar projects, which were increasing between 2015 and 2018, has been slowing down since then. The slowdown has been due to execution challenges involving large land and transmission requirements. Moreover, falling solar tariffs have incentivised the high electricity paying customers of the distribution companies (discoms) to take the open access route, which is increasing the discoms’ woes.

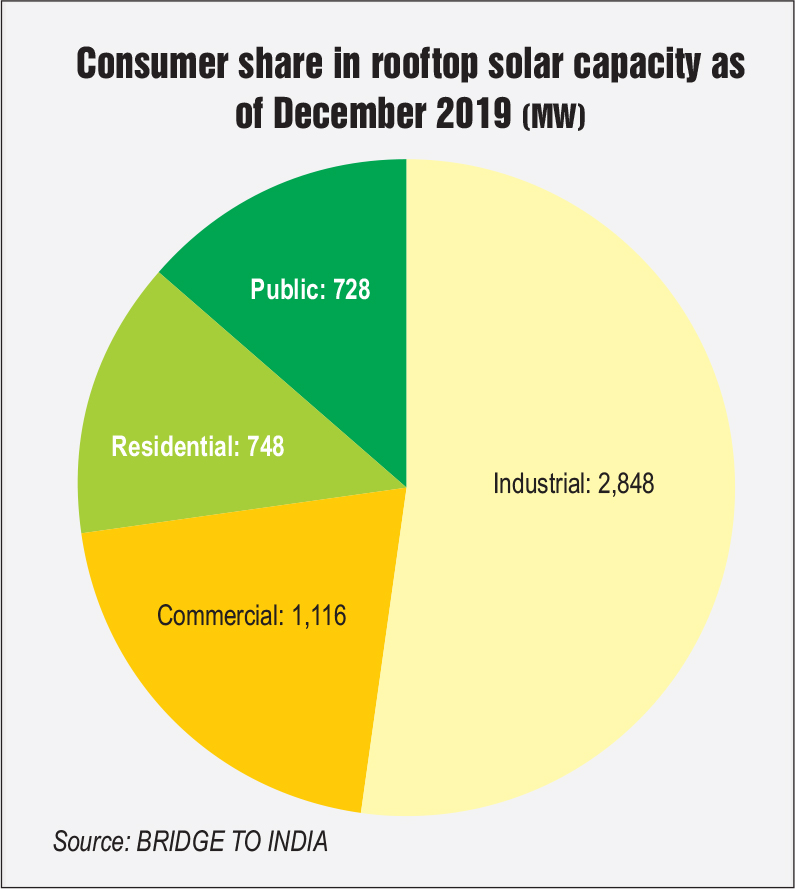

Contrary to this, the trends for the commercial and industrial (C&I) rooftop solar and open access solar segments have been quite different. These segments are primarily driven by the end-consumers’ need to reduce their electricity bills. Currently, the landed cost of rooftop solar systems is around Rs 3-Rs 4 per kWh and is continuously falling due to the rapid decline in the equipment cost. This landed cost is much lower than the C&I grid tariffs in the country and, therefore, is a huge incentive for C&I consumers to shift to renewable energy. Same is the case with the open access segment. The landed cost of open access solar projects is much lower than the grid tariffs for C&I users. The uptake of open access solar projects makes even more commercial sense when various open access charges are exempted. In the past few years, both these segments have grown because of renewable purchase obligations for some large customers and additional voluntary renewable energy targets taken up by a few customers. These projects are concentrated in a few states, dominated by Maharashtra, Rajasthan, Tamil Nadu and Karnataka. While Maharashtra has the largest share of rooftop solar systems, Karnataka has the largest share of open access market.

Despite the obvious economic case for these segments, the industry is not growing at its full potential because of some financial and operational reasons. The major reasons for this dismal growth of these segments are the restrictions posed by discoms that do not wish to lose their high electricity tariff paying C&I consumers. This has been a common trend in the past few years. However, resistance from discoms is slowly increasing momentum due to their mounting financial losses. Discoms stall the growth of these segments through removal of net metering policies, delay or denial of open access approvals and levy of high open access charges. Another issue faced by developers is the volatility of open access charges. These charges keep varying in different states across the country, making it difficult for developers of C&I rooftop and open access projects to keep up with these unpredictable and arbitrary changes.

Regulators have taken note of these challenges and are working towards finding innovative solutions. Recently, Maharashtra has come up with an innovative policy for the rooftop solar segment, which tries to solve the fundamental issues faced by all stakeholders. According to the new policy template, the state has allowed net metering for all consumers, levied banking charges for all C&I consumers and allowed discoms to levy grid charges of Re 0.72–Rs 1.16 per kWh, once the rooftop solar capacity crosses 2 GW. With these provisions, consumers get net metering, discoms get an additional revenue stream and investors get a stable policy environment. It is a win-win situation for all stakeholders and can be the future policy template for other states to follow.

While this is a positive move for the segment, challenges for the C&I rooftop and open access solar segments are not limited to the resistance posed by discoms. A large part of this market is untapped because of financing constraints. In India, the annual C&I rooftop solar market is 1.2 GW and the annual open access solar market is between 600 MW-800 MW, making the cumulative C&I market around 1.8 GW-2 GW. Of this market, just around 50 per cent is dominated by bankable large customers with whom developers are comfortable to do business because of their good credit worthiness. For customers in the remaining market, access to finance is a key challenge to develop rooftop and open access projects using their own funds. To this end, a lot needs to be done to incentivise developers to set up projects for these low-rated customers using the operating expenditure model.

Challenges in residential rooftop solar segment

The residential rooftop solar segment has also not been growing at a fast pace. The capacity addition in this segment has stagnated at around 200 MW per annum. While there has been policy impetus, on-ground implementation remains low. In a positive development for this segment, the Ministry of New and Renewable Energy approved Phase II of the grid-connected rooftop solar programme. The second phase has two main components. Under the first component, 4,000 MW of grid-connected residential rooftop solar projects will be installed by 2022, with a capital subsidy of up to 40 per cent. Under the second component, incentives will be provided to discoms based on the achievement towards the initial 18,000 MW of grid-connected rooftop solar plants.

There is still a looming uncertainty in this segment as many tenders have been floated by state agencies and, therefore, power offtake becomes an issue. There is also concern of low prices (Rs 37,000 per kW) that emerged in these tenders, which puts the future trajectory of tenders in a precarious position. Till date, around 952 MW of capacity has been tendered by 10 states. Despite the decline in the market sentiment because of Covid-19, the future outlook of the residential rooftop solar segment remains positive as various institutional investors are willing to tap this market. For this segment, the Green Climate Fund has led a $200 million credit facility, while the World Bank is planning a $245 million concessional lending facility. Moreover, new solar-focused non-banking financing companies are also emerging, which will improve access to finance, going forward.

Impact of Covid-19 and future outlook

Impact of Covid-19 and future outlook

While it is too early to gauge the impact of Covid-19 pandemic on these two segments, there are two broad trends that may emerge in the short term. One, going forward, the projects set up on the capital expenditure model will reduce as consumers have limited funds to spend due to fall in financing. Two, the top-tier customers will continue to accelerate their transition to renewables and developers would be keen to set up projects for such customers. In the long term, resistance of discoms is expected to increase as their financial losses will multiply. A drop in the capital costs due to a fall in price of equipments will further motivate discoms to increase their resistance towards scaling up of open access projects. Still, favourable economics will continue to drive demand for such systems. Therefore, the future outlook is largely positive, despite the current challenges faced during the pandemic.

Net, net, both rooftop solar and open access segments have attractive growth potential, which needs to be supplemented with a conducive policy environment involving policy stability and visibility. Going forward, consumer awareness and quality assurance for small consumers will be key to making growth in these segments more robust. Adopting innovative business models and more financing solutions will also go a long way in scaling up both the rooftop and the open access solar segments.

(Based on a panel discussion among VinayRustagi, Managing Director, BRIDGE TO INDIA Energy; SandipAgarwal, Managing Director and CEO, Ever Stream India/Think Energy Group; Adarsh Das, Co-Founder and CEO, SunSource Energy; DrAnuvrat Joshi, Head, Business Development, Cleantech Solar and P. Vinay Kumar, Founder, Varp Power.)