By Ashay Abbhi

On February 19, 2019, the Cabinet Committee on Economic Affairs (CCEA) approved Phase II of the grid-connected rooftop solar programme, which is aimed at achieving 40,000 MW of rooftop solar capacity by 2022. The focus of solar development in India has primarily been on the ground-mounted segment, mostly to increase the scale of installations for rapidly decreasing the cost of solar power generation. As a result, rooftop solar has experienced limited growth. According to BRIDGE TO INDIA, the total installed rooftop solar capacity in India stood at 3,399 MW, as of September 2018, a growth of 82.6 per cent over September 2017 (1,861 MW). Despite the high growth, the installed capacity of the segment is quite low, leading to scepticism over the achievement of the 2022 target. In light of this, the CCEA approval for Phase II of the grid-connected rooftop solar programme can give a much-needed boost to the segment.

The rooftop solar segment has traditionally suffered from a host of challenges, including the unavailability of competitive financing for project developers and consumers. The risk profile of rooftop solar projects is high and the borrowers’ credit profile is low, making financiers wary of lending capital to these projects. The reluctance of state discoms to let go of their high-paying industrial and commercial customers without adequate compensation is another reason for the low penetration of rooftop solar. Phase II of the rooftop solar programme attempts to address these challenges by providing central financial assistance (CFA) and designating discoms as nodal agencies.

Key features

- Target: Phase II is aimed at achieving 40,000 MW of cumulative installed rooftop solar capacity by 2022.

- Financial support: The programme will be implemented with a total financial support of Rs 118 billion.

- Eligibility: The CFA is available only for the residential segment, including individual houses, group housing societies and resident welfare associations. The CFA will not be extended to any other category, be it institutional, educational, social, government, commercial or industrial.

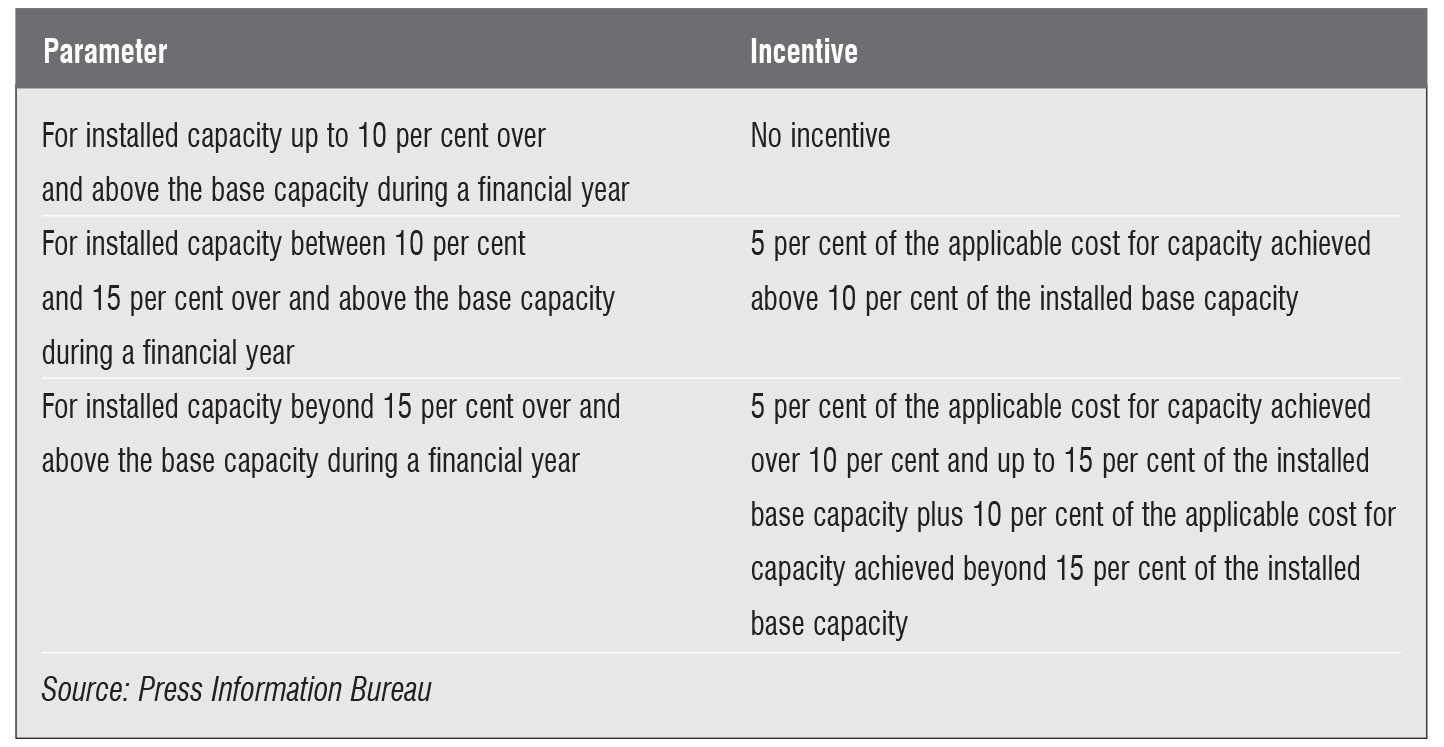

- Involvement of discoms: Under Phase II, the government has decided to increase the role of discoms. The discoms will be provided performance-based incentives based on the rooftop capacity achieved during a financial year (April 1-March 31). This capacity will be in addition to the base capacity at the start of each year.

- Incentives to discoms: Discoms will be incentivised for the addition of only the initial 18,000 MW, according to certain parameters (see box).

- Installed base capacity: The capacity within the jurisdiction of the discom at the end of a financial year will qualify as the installed base capacity for the next year. This includes all the rooftop solar capacity under residential, institutional, social, government, public sector and statutory/autonomous bodies, as well as private, commercial, industrial and any other segments.

- Applicable cost: The applicable benchmark cost set by the Ministry of New and Renewable Energy for states and union territories for mid-range rooftop solar capacity of above 10 kW and up to 100 kW or the lowest cost discovered in the tenders for those states will be the applicable cost for incentives.

- Nodal agency: The discoms and their local offices will be the nodal agencies for the implementation of the programme.

- Emission savings: It is estimated that at the end of Phase II of the programme by 2022, 45.6 tonnes of CO2 emissions per year will be reduced.

Conclusion

Conclusion

Phase II of the rooftop solar programme can address the problem of discom reluctance – the biggest roadblock in the path of rooftop solar development in India. By involving the discoms as nodal agencies and incentivising them, the loss in revenue may no longer be a reason for them to refuse rooftop solar uptake. Meanwhile, capacity addition in the residential segment is expected to improve on the back of the CFA provided as per the programme. The CCEA approval for Phase II is, therefore, likely to give the rooftop solar market a significant boost.