Over the past two years, the solar market has witnessed unprecedented growth globally, with record capacity additions in many countries and solar power tariffs falling to the floor. This has significantly increased the share of solar energy in the global electricity mix. According to Fraunhofer ISE, the photovoltaic (PV) market grew at a compound annual growth rate of 40 per cent during 2010-16. With the increase in demand and an even higher increase in supply, the solar cell and module prices have declined rapidly. This has intensified competition between PV technologies such as crystalline silicon (c-Si) and thin film in terms of efficiency and cost effectiveness. Further, the market’s focus has shifted to research and development (R&D) activities in solar PV technologies, particularly in China and Germany, which have been the pioneers and front runners in the segment.

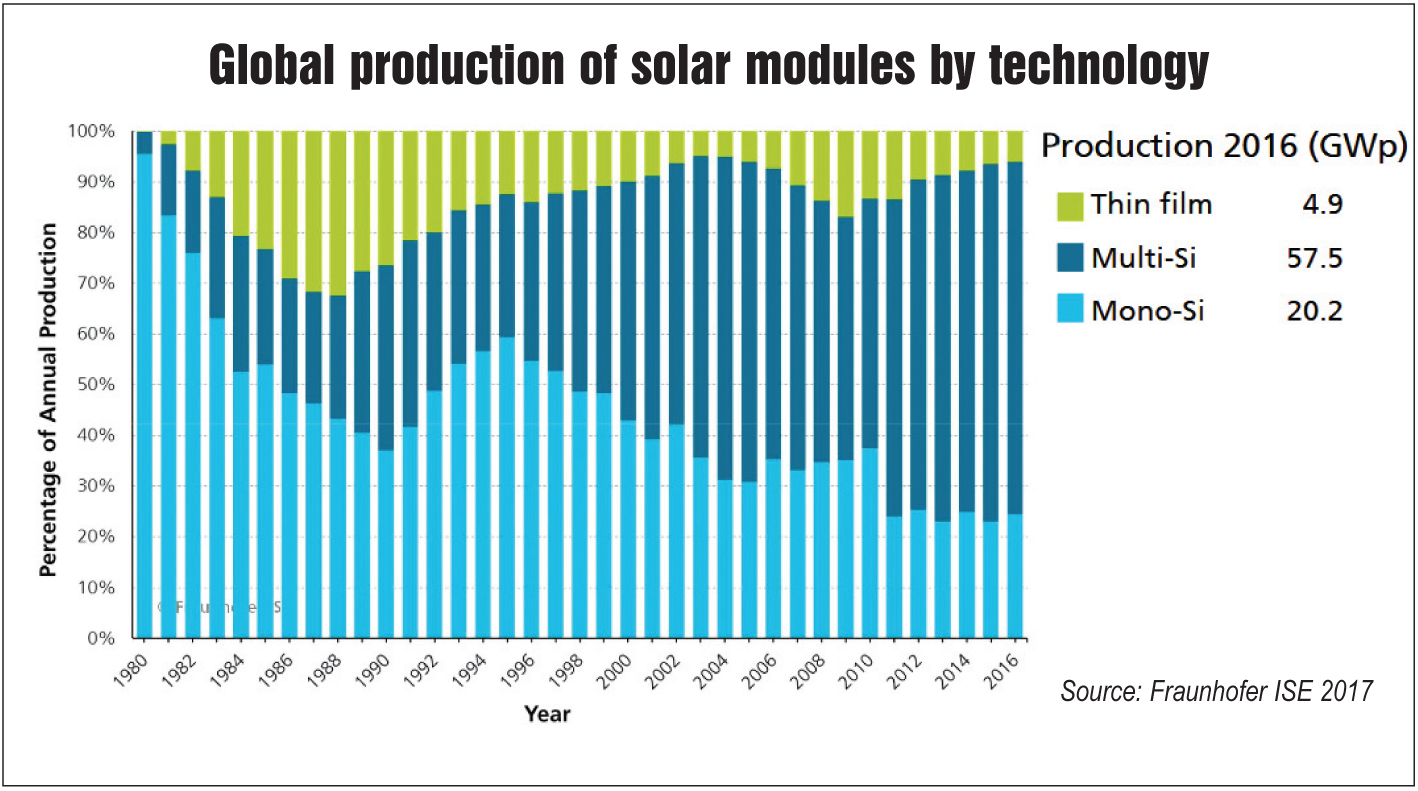

Crystalline silicon (c-Si) has become the preferred choice of PV technology, accounting for 94 per cent of all PV production in 2016 as compared to thin film, which accounted for 6 per cent. This can be attributed to the low cost of the technology and its mass production by Chinese companies. Within c-Si, polycrystalline technology is more popular than monocrystalline for similar reasons. However, monocrystalline is by far a superior solar PV technology.

Efficiency trends

Of all PV technologies, monocrystalline silicon is the most efficient, with polycrystalline being a distant second. The peak lab efficiency of monocrystalline cells has been recorded at 26.7 per cent, with average efficiency of 24.4 per cent, as compared to the peak efficiency of 21.9 per cent for polycrystalline silicon PV cells. For monocrystalline modules, the lab efficiencies have been recorded at 24.4 per cent, much higher than those of polycrystalline modules and CIGS (cadmium indium gallium selenide) thin film modules at 19.9 per cent and 19.2 per cent, respectively. In October 2017, China-based LONGi Solar achieved conversion efficiencies of 22.71 per cent for monocrystalline passivated emitter rear contact (PERC) technology at its 100 MW pilot cell line in mass production. It has been certified by Fraunhofer ISE CalLab, Germany. The company achieved multiple record efficiency levels for monocrystalline PERC cells thrice in a span of only ten days, indicating the strength of innovation and the advanced nature of this technology.

The efficiency of monocrystalline silicon technology grew gradually till 2013, from about 23 per cent in 1993 to just below 25 per cent in 2001 and 25 per cent in 2004-05 and then remained stable for four to five years before increasing by a few percentage points in 2011-13. At present, it stands beyond 26 per cent and is expected to improve further in the short term. Meanwhile, a comparison of commercially available monocrystalline modules produced by leading global manufacturers shows that on-field efficiencies for the technology are mostly in the range of 16-17 per cent. These included modules produced by Kyocera, Hanhwa Q Cells, Canadian Solar and Jinko Solar.

A primary point of difference between mono and polycrystalline technologies is the manufacturing process. Polycrystalline cells are made by assembling multiple pieces (grains) of silicon into wafers, whereas monocrystalline cells are made of a single continuous silicon lattice. The wafer thickness for these cells has improved from about 400 µm in 1990 to about 160 µm in 2016. Similarly, the use of silicon has reduced significantly, from about 16 grams per watt to 5.3 grams per watt.

Cost trends

The cost of PV technology significantly impacts its performance, uptake and popularity in any market. Most of the emerging solar markets are developing countries and are therefore price-sensitive. Monocrystalline technology is more expensive than its counterparts owing to a complex manufacturing process. On the other hand, polycrystalline silicon cells and modules involve a simpler and low-cost production process. Moreover, mass production by Chinese companies such as Talesun and GCL has disrupted established business markets by bringing an abundant supply of polycrystalline cells and modules.

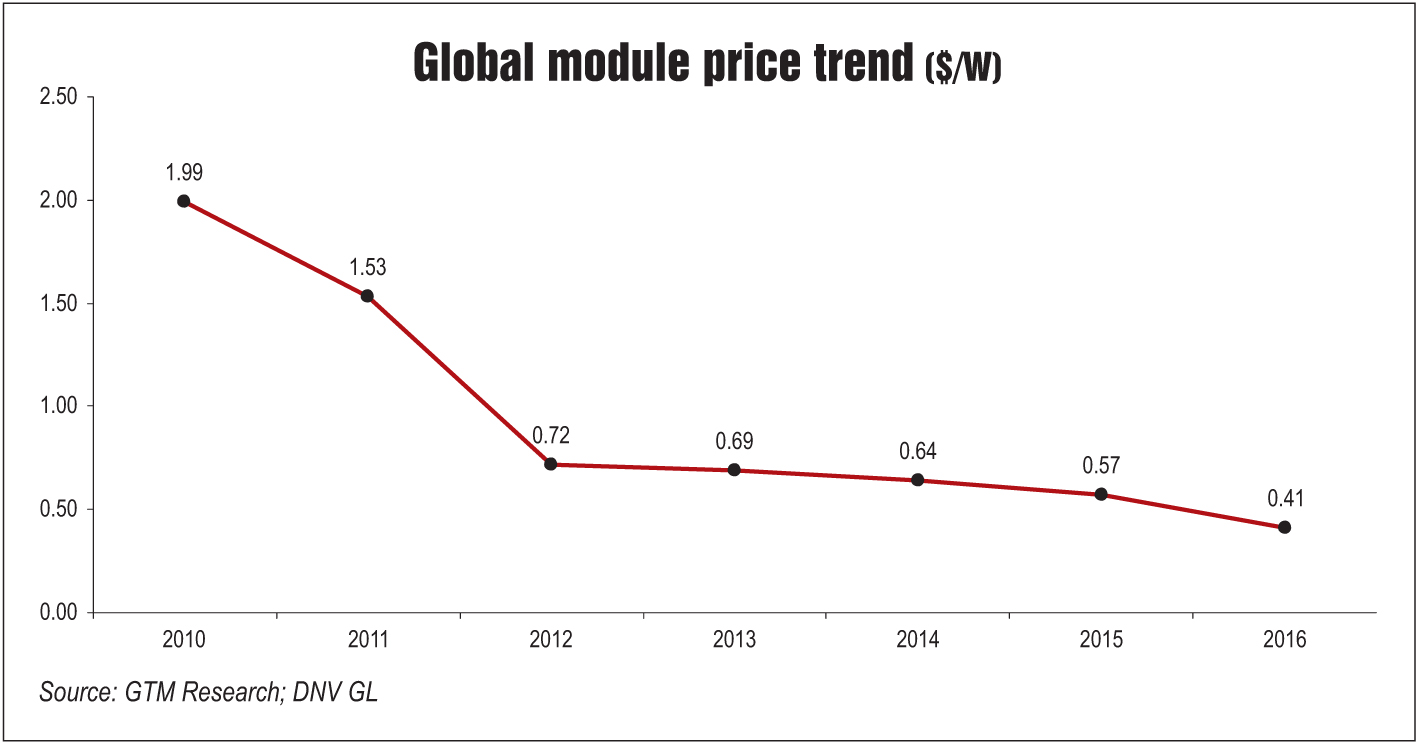

According to the pvXchange module price index, the price of monocrystalline modules has decreased over the past year along with the decline in global average solar module prices. As of July 2017, the price of crystalline modules stands at Euro 0.45 per watt in Germany, Euro 0.52 per watt in Japan and Korea, Euro 0.45 per watt in China and Euro 0.4 per watt in Southeast Asia.

The price gap between polycrystalline and monocrystalline technologies has been a primary reason for the latter’s restricted market share across the globe. According to media reports, extensive R&D is being undertaken by companies such as LONGi to reduce this gap. In 2014, the price difference between the two technologies stood at $0.3-$0.4 per piece. Over the past two years, this has been reduced to $0.1-$0.15 per piece. With the technology becoming more competitive, the cost effectiveness of monocrystalline technology has also increased significantly. The decline in module prices will help improve the overall capital expenses for setting up a solar plant based on monocrystalline technology.

Production trends

The production of PV modules has increased significantly over the past few years. Fraunhofer ISE estimates about 75 GW of PV modules were produced across the globe in 2016. Their distribution as per technology is highly skewed in favour of polycrystalline modules, indicating its popularity in solar-rich countries. While the share of polycrystalline modules has been fluctuating, it has remained the dominant technology globally since 2010. On the other hand, monocrystalline was the preferred choice of technology from the early 1980s to late 1990s. From 2000 to 2010, the share of this technology declined continuously as the market was flooded with inexpensive polycrystalline modules manufactured in China.

In 2016, the trend continued with monocrystalline technology accounting for about 25 per cent or 20.2 GW of global production. Polycrystalline modules, on the other hand, accounted for 70 per cent or 57.5 GW of all modules manufactured during the year. Meanwhile, thin film technology held a 6 per cent share in the global production.

The way forward

With improving efficiencies and the reducing price gap among technologies, the share of monocrystalline modules is expected to increase in the future. Further, to meet the growing demand for solar PV technologies across the world, both polycrystalline and monocrystalline technologies will need to be exploited.

China is currently scaling up the production of monocrystalline silicon cells. In fact, Chinese manufacturers are of the opinion that the polycrystalline market has saturated and it could be the time for monocrystalline technology to grow.