The growth of the small-hydro power (SHP) segment in India has been sluggish year after year. While the government has been fairly optimistic about the segment, it has failed to translate this into a real fillip to growth. In fact, the segment has been short of target for the past few years and as such, there seems to be little hope on the horizon.

Current scenario

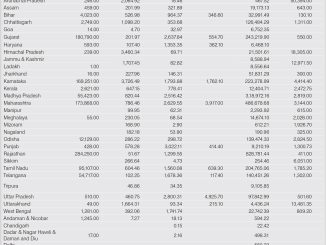

With an estimated potential of 20,000 MW across 6,474 sites, the industry remains largely underdeveloped with an installed base of only 4,384 MW as of June 2017, with a paltry 4 MW being added in the first quarter of 2017-18.

It can also be argued that the segment has lost favour with the government, which has instead turned its attention to the solar and wind energy segments. Notably, capacity addition has slowed down post the government’s announcement of the ambitious renewable energy target of 175 GW of capacity by 2022. As per data from the Ministry of New and Renewable Energy (MNRE), a disappointing 106 MW was added in 2016-17 against the 250 MW target.

Meanwhile, the private sector too is reluctant to invest in the SHP segment due to the large size of investments involved as well as the long delays in obtaining permits, low tariffs and modest returns. Moreover, seasonal variability and unpredictability of rainfall restrict power generation and hence affect revenues. Such issues undermine the viability of SHP projects for private investors.

State-wise scenario

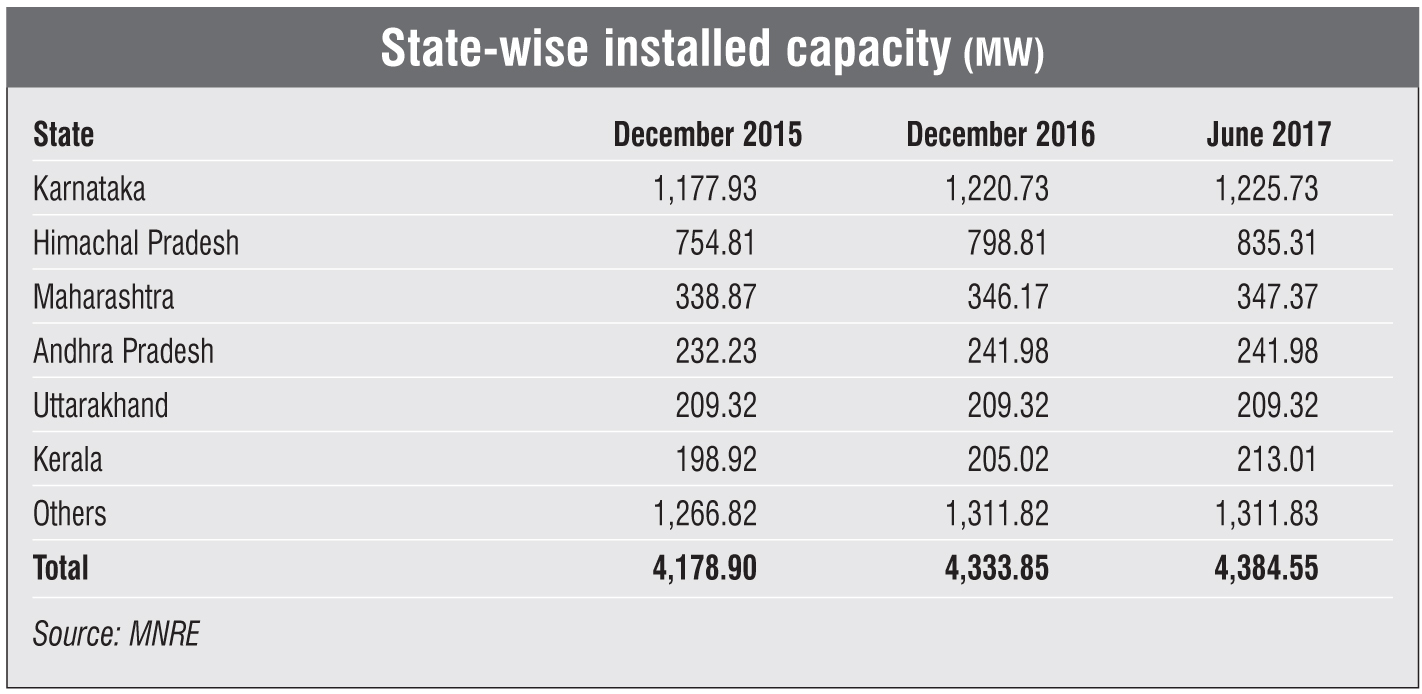

Although Karnataka and Himachal Pradesh have the largest SHP potential and installed capacity, Maharashtra has been able to achieve the largest share of its potential at 43.73 per cent as of June 2017. Uttarakhand has a significantly large potential of 1,707.87 MW. However, capacity addition has stagnated at 209.32 MW over the past three years.

In the other states, capacity addition has been very modest. Among the worst performing states, where the installed capacity is only 10 per cent or below that of the identified capacity, are Arunachal Pradesh, Madhya Pradesh, Jharkhand, Assam, Manipur, Gujarat and Uttar Pradesh. While other sources of renewable energy have witnessed significant uptake in these states, SHP has failed to make a mark.

Issues and challenges

Issues and challenges

There are a series of challenges that are impeding growth in the SHP segment. These issues have remained more or less the same year after year due to the lack of proactive government intervention in tackling these. Protracted delays and difficulties in obtaining permissions from multiple government agencies increase the gestation period of plants, reducing their viability and making SHP projects unattractive for private developers. The state governments and central agencies need to expedite and streamline the process of providing statutory clearances to projects.

Another concern is grid availability. Lack of grid connectivity has often led to losses for developers, who are forced to curtail generation, leading to revenue losses and underutilisation of the plant.

The way forward

Future projections do not look too optimistic for the SHP segment, caught as it is between policy uncertainty and investor reluctance. Dwindling investor interest and lack of government attention indicate bleak times ahead for the SHP segment.

While solar and wind no doubt make greater commercial sense, SHP has its own set of benefits that cannot be ignored. SHP projects offer large social and economic gains, which call for urgent government intervention to promote this segment.