This is an extract from a recent report “India Insights Briefing: Unlocking India’s Clean Industrialisation Opportunity,” published by Industrial Transition Accelerator (ITA) and BCG.

India is rapidly emerging as a global industrial hub, with surging production and consumption in core heavy industries such as steel, cement, aluminium, chemicals, aviation, and shipping that is powering economic growth and employment. Current carbon-intensive means of production are driving a steep rise in GHG emissions, with heavy industry already contributing nearly 20- 25% of India’s total emissions, while increasing reliance on fossil fuel imports, exposure to volatility in global energy prices, and the risk of losing competitiveness in clean commodity markets. Clean industrial transition offers an opportunity to navigate the dual challenge of sustained industrial growth while pursuing long-term economic resilience, sustainability, and export competitiveness.

Sector Deep Dives

Sector Deep Dives

Chemicals

India’s distinct strength lies in low–cost renewable energy generation. Declining electrolyser capex costs, export–oriented hubs, and supportive government policies position it strongly to become a global leader in producing clean chemicals for domestic use and export. It is emerging as a global hub for clean chemicals production, with a growing pipeline of projects that can reduce import dependence and enhance economic resilience. India ranks as the third-largest ammonia producer with an output of 17.4 MT in 2022–23, representing over 8 per cent of global production capacity. However, despite its large-scale domestic production, around 86 per cent of domestic ammonia consumption is met through imports of ammonia, natural gas, or ammonia embedded in fertiliser end-products. Green ammonia offers India a strategic opportunity to reduce reliance on imports, strengthen food security, and build global competitiveness. As a critical fertiliser feedstock, ammonia currently exposes India to natural gas price volatility and supply chain disruptions.

Substituting imports with domestic green ammonia production can help secure supply chains while supporting decarbonisation. India has one of the largest green ammonia and methanol project pipelines globally, and the largest amongst EMDEs, with 51 projects. This pipeline could unlock ~$130 billion in investment, create thousands of green jobs, and expand India’s green hydrogen capacity beyond 6 MTPA by 2030, surpassing the NGHM target of 5 MTPA. Green ammonia dominates the pipeline with 46 projects and ~30 MTPA capacity. While ammonia dominates the pipeline, green methanol projects are taking shape. At least five commercial-scale projects are underway, including the V. O. Chidambaranar Port bunkering pilot, which will provide 750 m³ of storage and anchor India’s role in coastal green shipping corridors. This reflects growing confidence in methanol as a bridge between hydrogen production and carbon utilisation pathways.

Five states dominate the pipeline, positioning themselves as regional hubs with a large share of projects led by established RE players. Odisha, Andhra Pradesh, Tamil Nadu, Gujarat, and Karnataka are emerging as green industrial hubs, owing to access to natural resources, trade infrastructure, and enabling policy environments. Odisha leads in planned capacity, supported by proximity to major ports (Paradip, Kakinada, Kandla, Tuticorin) that provide crucial infrastructure for exports. However, just six major developers: AM Green, ACME, NTPC, ReNew, Ocior, and Avaada account for approximately half of the announced pipeline capacity, with the rest distributed amongst over 20 players. Most major RE players have announced at least one project driven by the strategic decision to diversify from green electrons into green molecules. These players are well-positioned to leverage their strong balance sheets and project execution experience to take on the high capex of hydrogen-based production.

Steel

While India’s growing steel demand is currently set to be met through carbon-intensive production assets, producers can leverage low-cost renewables, a rapidly developing green hydrogen ecosystem, and policy momentum to pivot towards low-emissions steel production, avoiding future lock-ins and unlocking global competitiveness. The iron and steel industry is India’s largest industrial source of GHG, contributing an estimated 10–12 per cent of the national total. It is also among the most energy and emissions-intensive globally: in FY23–24 its average intensity was ~2.54 tCO₂/tcs1 versus a global average of ~1.91 tCO₂/tcs2. This gap stems largely from the technology mix as 90 per cent of primary iron in India is produced via coal-based BF and rotary-kiln DRI, with a greater share of capacity in BF. Indian steel plants with BF units on average emit 2.4–2.5 tCO₂/tcs, typically 30–40 per cent higher than similar units in European countries like Germany and Sweden. Adoption of best available technologies (BATs) is gradually closing this gap, but their penetration, particularly in the smaller-scale steel plants, remains limited.

Planned investments in cost-effective but carbon-intensive assets risk locking the industry into high-emissions pathways and out of emerging low-emissions steel markets. BF accounts for ~80 per cent of additional ironmaking capacity and basic oxygen furnaces (BOF) for ~55 per cent of additional steelmaking capacity. The reliance on fossil-based routes reflects the need to meet domestic demand cost-effectively in the absence of viable low- or near-zero-emission alternatives such as green hydrogen and carbon capture. Constraints in access to high-grade iron ore, natural gas, and bioresources further restrict the shift to cleaner pathways. At the same time, overcapacity in the global markets (creating downward pressure on prices) and rising competition from Asian producers have weakened Indian steel exports in recent years. These exogenous pressures erode profit margins and constrain the industry’s ability to invest in transitional and near-zero emissions technologies. The current trend presents a significant risk of locking in massive carbon emissions over the coming decades. Further, with commitments from global steel consumers for the reduction of carbon footprint from purchased materials, failure to transition to low-carbon steel would result in significant loss of export opportunities for Indian producers.

The Indian steel sector and the Government of India demonstrate a strong intent to overcome the challenges to shift towards low-emissions pathways. With abundant renewable energy potential, a rapidly developing green hydrogen ecosystem, and a supportive policy landscape, India has an opportunity to position itself as a global leader in cost-competitive, low-carbon steel production. In 2025, the government (in consultation with the industry) has set a target to reduce emission intensity to below 2.2 tCO₂/tcs by FY29– 30, aligned with the CCTS. Policy momentum is building further through the NGHM and the upcoming National Green Steel Mission. With the support of initiatives like LeadIT, near-term efforts focus on deploying commercially viable BATs, expanding RE use, and increasing scrap utilisation, while piloting low-carbon alternatives such as green hydrogen, biochar, and CCUS.

Furthermore, the use of green hydrogen is in early stages, with just two commercial-scale projects being announced. The first project is a 4 MTPA green steel project by JSW low-carbon steel (to be carried out in two phases of 2 MTPA each) involving the phased transition of a natural gas-based plant to green hydrogen. In a major development, JSW Steel would soon commission one of the first projects in India to partially use green hydrogen in the DRI unit at its Vijayanagar plant, deploying a 25 MW electrolyser. Other project is a pilot for green hydrogen injection into BF by Steel Authority of India Limited. Beyond these two projects, a handful of small-scale pilots, some supported by the Ministry of Steel, are testing green hydrogen integration across both BF and vertical shaft DRI units. These projects demonstrate early momentum across leading steel producers. Successful scaling of these initiatives hinges on achieving commercial viability through cost decline in green hydrogen production and structuring of de-risked business models, including securing offtake for premium low-carbon steel.

Cement

Building on its strong production base, improving efficiency levels, and ambitious net-zero commitments, India’s cement sector has the opportunity to become a global example in balancing industrial growth with low-carbon transition. The Indian cement industry is the world’s second largest in terms of production capacity (770 MTPA) and is a backbone of the country’s economy. However, it faces a steep decarbonisation challenge but is starting from a relatively strong base. As the second-largest industrial GHG emitter after iron and steel, cement accounts for about 7-8 per cent of India’s total CO₂ emissions. It is also one of the hardest to abate sectors, given the reliance on fossil fuels for combustion in kilns and a large share of process emissions from limestone calcination, which require expensive breakthrough solutions. Despite this inherently carbon-intensive production profile, Indian cement producers have already made notable efficiency gains. The sector’s current average emission intensity stands at 0.60–0.65 tCO₂ per tonne of cement, close to the global average of ~0.6 tCO₂/t6. This progress reflects a decade of sustained investments in best-available efficiency technologies and the early rollout of waste heat recovery systems (WHRS), which have proven to be cost-effective, providing a solid foundation for transitioning to low-carbon cement production.

Policy push, early-stage technology development support, and corporate leadership are paving the way for a low-carbon transition. India’s cement sector is beginning to align around both regulatory and voluntary decarbonisation measures. The MoEFCC6 now mandates 186 cement plants to cut their greenhouse gas emission intensity (GEI) by 2–3 per cent between 2025–27, creating an accountability baseline for the industry. While modest, these targets are expected to strengthen over time. In parallel, leading companies such as UltraTech, Dalmia, JK Cement, and JSW Cement have set net-zero timelines for 2040–2050, with interim goals around scaling renewable energy, raising thermal substitution rates (TSR), expanding WHRS, and piloting breakthrough technologies such as CCUS and kiln electrification. Government and industry are also investing in building the CCUS ecosystem — NITI Aayog is developing a national CCUS policy framework to accelerate adoption and enable CO₂ value chains, while the Department of Science and Technology has launched five CCUS testbeds to build technical know-how. At the global level, India’s collaboration with Sweden through LeadIT reinforces this momentum, with cement identified as a priority sector for advancing early-stage, low-carbon projects. The path towards further reductions in emissions abatement is challenging due to several technological, economic, and market barriers. However, India’s cement industry can leverage its existing capabilities to become a global leader in balancing industrial expansion with low-carbon growth.

Aviation

India’s rapidly growing aviation sector is well-positioned to transition to SAF, meeting domestic demand while emerging as a global leader and exporter, supported by strong resource availability. Aviation contributes over ~2.5 per cent of global GHG emissions. To address these emissions, the International Civil Aviation Organisation adopted the CORSIA in 2016. From 2027, airlines will be mandated to offset emissions from international operations above 2019 levels through reductions or carbon credit purchases. For India, where international aviation is expanding faster than in many mature markets, exposure to compliance costs is disproportionately high. Industry estimates suggest that India’s two leading carriers could face $0.5–2.3 billion in costs between 2027- 2035. This makes decarbonisation measures urgent, particularly through the adoption of SAF. Currently approved pathways can produce drop-in SAF with 50–80 per cent lower life-cycle carbon footprint, and these can be blended up to 50 per cent with the conventional jet fuel without significant engineering changes.

India is well placed to emerge as a leading SAF producer, with studies indicating the potential to produce 8–10 MTPA by 2040, equivalent to ~5 per cent of global demand. India’s advantage stems from the availability of feedstock like biomass, agricultural waste, used cooking oil, and green hydrogen. The production capacity could be even higher with early actions from the domestic players and adequate policy support. Domestic demand for SAF is expected to reach ~4.5 MTPA, leaving a significant surplus for exports to premium markets like the EU, UK, and US. However, India needs to act fast as several Southeast Asian states, like Singapore, Malaysia, Thailand, Indonesia, and the Philippines, are exploring SAF production and are expected to compete with India for a share in the global SAF demand. For India, early policy support and decisive industry action would be critical to secure a competitive share of this emerging global market.

At present, India’s SAF pipeline consists of three large-scale projects and one pilot across different technology routes. The state-run petroleum company IOCL is constructing a 0.035 MTPA plant to convert used cooking oil to SAF. Once operational, this plant might be sufficient to meet the 1 per cent SAF blending mandate in India in 2027. There is one commercial scale project announced by NGEL in Andhra Pradesh with an estimated capacity of 0.2 MTPA PtL SAF production. Another project has been announced by a joint venture between IOCL and LanzaJet based on the latter’s AtJ technology with a capacity of 0.085 MTPA in Haryana. Mangalore Refineries and Petroleum Limited has announced a pilot project for HEFA-based SAF production in Karnataka.

Aluminium

By harnessing India’s abundant low-cost renewable energy and declining energy storage costs, the aluminium sector can position itself among the world’s lowest-emission producers at globally competitive prices. Meeting rapidly growing domestic demand while remaining globally competitive creates both urgency and opportunity for India to reposition as a hub for low-emission aluminium production. As the world’s second-largest producer (~6 per cent of global output1,2), India’s aluminium sector underpins infrastructure, automotive, and urbanisation, while being deeply integrated into global trade. Domestic demand is poised to double to ~9 MT by 2033, as the per capita consumption catches up with the global average. At the same time, trade competitiveness has recently come under strain: exports to Europe fell by 34 per cent between 2022–2024 in anticipation of the EU’s CBAM, the US imposed tariffs of up to 50 per cent, Asian demand, especially from Japan, remains weak, and global buyers are tightening procurement standards with over 7000 SBTi companies have set emissions reduction targets in line with climate science.

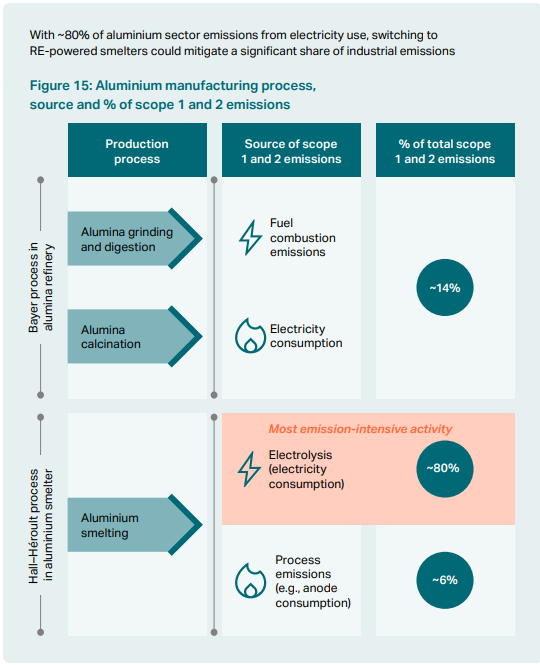

Switching aluminium smelters to renewable power is the fastest, lowest-cost lever to cut industrial emissions and protect export competitiveness. The sector contributes 2–3 per cent of India’s industrial GHG emissions, with a carbon intensity of ~17–18 tCO₂/t4,1 versus a global average of ~15 tCO₂/t1, because ~80 per cent of its footprint comes from captive or grid-backed thermal power (Fig.15). Replacing this electricity with round-the-clock (RTC) renewables can deliver immediate material reductions at a modest Rs 1–2/kWh premium (recent SECI RTC auctions cleared ~Rs 5.06–5.07/kWh), a cost that is likely far lower than expected exposure of the EU-bound exports under CBAM. Abundant low-cost renewable power offers the nearterm pathway to slash aluminium’s share of industrial emissions while safeguarding India’s position in international markets.

Switching aluminium smelters to renewable power is the fastest, lowest-cost lever to cut industrial emissions and protect export competitiveness. The sector contributes 2–3 per cent of India’s industrial GHG emissions, with a carbon intensity of ~17–18 tCO₂/t4,1 versus a global average of ~15 tCO₂/t1, because ~80 per cent of its footprint comes from captive or grid-backed thermal power (Fig.15). Replacing this electricity with round-the-clock (RTC) renewables can deliver immediate material reductions at a modest Rs 1–2/kWh premium (recent SECI RTC auctions cleared ~Rs 5.06–5.07/kWh), a cost that is likely far lower than expected exposure of the EU-bound exports under CBAM. Abundant low-cost renewable power offers the nearterm pathway to slash aluminium’s share of industrial emissions while safeguarding India’s position in international markets.

Policy and industry actions are beginning to set a foundation for transition. The MoEFCC has introduced Greenhouse GEI reduction targets of 2–6 per cent for 13 aluminium smelters and refineries by 2027. All three major producers, Vedanta, Hindalco, and NALCO, have declared net-zero ambitions with interim renewable integration targets. These early steps send positive signals but fall short of what is needed to match international decarbonisation benchmarks and protect India’s aluminium trade position. The pathway forward requires overcoming structural barriers to scale low-emission production. Renewable power is now cost-competitive and provides a clear pathway for transition, but high upfront investment in energy storage systems, bottlenecks in transmission and distribution networks, and reliance on imported battery components raise project execution risks. Addressing these constraints at pace will be critical for embedding aluminium at the centre of India’s clean industrialisation story, helping the sector capture domestic demand, sustain exports, and avoid long-term carbon lock-in.

Access the report here